The 2026 conforming mortgage limits have been launched through the vacation week and (shock, shock) they’re greater!

In case you weren’t conscious, these mortgage limits are pushed by the annual change in residence costs, and sure, property values went up.

Whereas there have been pockets of weak spot recently, particularly in locations like Florida and Texas, residence costs nonetheless elevated nationally.

As such, the 2026 conforming mortgage restrict can be $26,250 greater versus 2025, rising from $806,500 to $832,750.

And in high-cost areas, the ceiling mortgage restrict for one-unit properties can be a whopping $1,249,125.

2026 Conforming Mortgage Limits Climb Once more

- 1-unit property: $832,750

- 2-unit property: $1,066,250

- 3-unit property: $1,288,800

- 4-unit property: $1,601,750

The FHFA introduced final week that the conforming mortgage restrict for mortgages backed by Fannie Mae and Freddie Mac rose to $832,750 for 2026.

This marks a rise of $26,250 from the 2025 mortgage limits, pushed by a 3.26% rise in residence costs between the third quarters of 2024 and 2025.

It’s not fairly as giant because the 5.2% enhance seen a yr in the past, however it’s greater nonetheless.

In high-cost areas of the nation like Los Angeles, the brand new ceiling for one-unit properties can be $1,249,125, which is 150 % of the baseline restrict.

Whereas many anticipated residence costs to be flat this yr, and even fall, they nonetheless managed to realize slightly extra regardless of poor affordability.

The FHFA bases the change by itself nominal, seasonally adjusted, expanded-data FHFA residence value index (HPI).

Importantly, the conforming mortgage restrict can’t fall although. So even when residence costs did occur to go down between the third quarter of final yr and this yr, the conforming restrict wouldn’t go down.

As an alternative, it could merely keep put. One thing to consider shifting ahead if the doomsayers are lastly proper and residential costs come down nationally.

Within the meantime, residence consumers and present householders trying to refinance a mortgage can make the most of barely greater mortgage limits.

What’s the Advantage of Staying At/Under the Conforming Mortgage Restrict?

The principle benefit of staying at/beneath the conforming mortgage restrict is that mortgage charges are typically decrease.

Conforming loans are the commonest kind of residence mortgage, supplied by nearly each financial institution and lender as a result of they’re straightforward to unload to traders on the secondary market.

Conversely, jumbo loans whereas extensively accessible, are extra area of interest and don’t have an enormous backer like Fannie and Freddie.

In consequence, rates of interest on jumbo loans are sometimes greater, although this isn’t at all times the case and exceptions do apply.

As well as, it’s usually simpler to get permitted for a conforming mortgage as a result of the underwriting requirements are slightly looser.

For instance, you’ll be able to are available with only a 3% down fee and also you usually don’t want a lot in the way in which of asset reserves.

The most DTI limits and credit score rating necessities additionally are typically much more forgiving.

In the meantime, a jumbo mortgage lender may require a ten% minimal down fee and 6 months of reserves.

So one thing to contemplate when you have been at/near the conforming restrict and are actually underneath it due to the rise.

2026 Excessive-Value Space Mortgage Limits Rise to $1,249,125

- 1-unit property: $1,249,125

- 2-unit property: $1,599,375

- 3-unit property: $1,933,200

- 4-unit property: $2,402,625

As at all times, the mortgage limits are greater in lots of cities nationwide the place property values are higher due to the high-cost space limits.

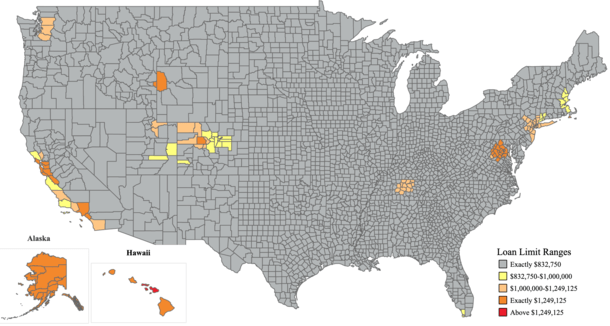

There are greater than 3,000 counties or county-equivalent jurisdictions in the USA, and every year about 100 to 200 of them qualify for high-cost limits that exceed the baseline restrict, as seen within the map above.

This contains locations like Denver, Jackson Gap, Los Angeles, and New York Metropolis, and likewise Alaska, Guam, Hawaii, and the U.S. Virgin Islands.

In these areas, the mortgage limits go as excessive as $1,249,125 for a one-unit property, and to almost $2.5 million for a fourplex.

There are additionally high-cost areas within the state of Hawaii that go even greater. So there may be actually numerous alternative to remain at/beneath the conforming mortgage limits.

The brand new conforming mortgage limits are efficient January 1st, 2026, although some lenders are already accepting the upper limits as we speak.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Observe me on X for decent takes.