Union Finance Minister Smt Nirmala Sitharaman on February 1st 2025 introduced her eighth consecutive Union Finances 2025 within the Lok Sabha. Under are the most recent private finance associated proposals which have been made in Finances 2025-26 ;

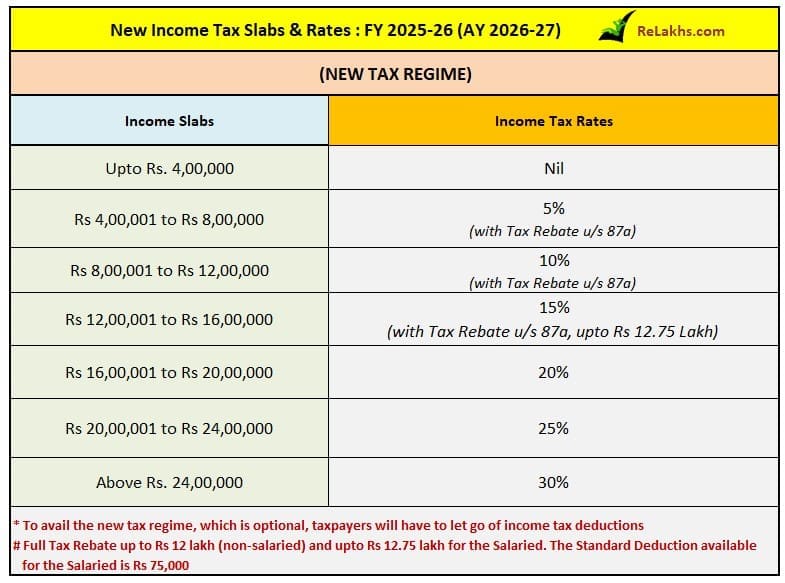

1) Revised Earnings Tax Slab Charges for FY 2025-26

- Beneath the brand new tax regime, the fundamental exemption restrict has been elevated from Rs 3 lakh to Rs 4 lakh.

- As per the Finances 2025, no revenue tax will likely be payable on revenue as much as Rs 12 lakh has been proposed.

- The salaried people eligible for the customary deduction good thing about Rs 75,000 is not going to be required to pay any taxes if their gross taxable revenue doesn’t exceed Rs 12.75 lakh.

- In case your revenue exceeds Rs 12 lakh then you’ll want to pay tax at relevant slab charges.

2) Revised Part 87A Tax Rebate FY 2025-26 / AY 2026-27

- The restrict for claiming the tax rebate is elevated from the present Rs 7 lakh to Rs 12 lakh for revenue beneath Part 115BAC. The utmost rebate will rise from Rs 25,000 to Rs 60,000.

- Kindly observe that this rebate is not going to apply to particular grade incomes similar to capital positive factors.

- In case your regular revenue aside from particular charge revenue (similar to capital positive factors) is as much as Rs 12 lakh, a tax rebate is being supplied along with the profit attributable to slab charge discount in such a fashion that there isn’t any tax payable by you.

- In easier phrases, should you’re a daily salaried particular person or earn different kinds of “regular revenue” as much as Rs 12 lakh, you received’t need to pay any tax, due to each the tax rebate and the decreased revenue tax slabs. Nevertheless, should you earn revenue from sources like capital positive factors, that revenue received’t profit from the rebate, and it is going to be taxed individually beneath totally different guidelines.

Regular Earnings or common revenue refers to your wage, wages, rental revenue or enterprise earnings. The place as Particular Fee revenue refers to capital positive factors, the place relevant tax charges are totally different. So, LTCG & STCG from Fairness or different particular charges property usually are not tax free inside this Rs 12 lakh.

3) Revised TDS restrict for Senior Residents

The restrict for tax deduction at supply on curiosity revenue for senior residents is being doubled from the current Rs 50,000 to Rs 1 lakh.

4) Revised TDS restrict on Lease

The annual restrict of Rs 2.40 lakh for TDS on lease is elevated to Rs 6 lakh.

5) Revised time restrict to replace ITRs

- Finances 2025 has proposed to increase the time restrict for submitting up to date revenue tax returns from the present 24 months to 48 months.

- Whereas Finances 2025 has prolonged the time restrict for submitting up to date ITR, the penal tax payable on the extra revenue declared within the ITR has been pegged at 60% and 70% for up to date ITRs filed within the third and 4th 12 months from the tip of the respective evaluation 12 months.

6) Good thing about two Self-Occupied Properties

Presently revenue tax assessees ca declare the annual worth of self-occupied properties as nil solely on the fulfilment of sure circumstances. Contemplating the difficulties confronted by taxpayers, it’s proposed to permit the advantage of two such self-occupied properties with none situation.

7) TCS modifications for remittances beneath LRS

The edge to gather tax at supply (TCS) on remittances beneath RBI’s Liberalized Remittance Scheme (LRS) is proposed to be elevated from Rs 7 lakh to Rs 10 lakh. The FM additionally proposed to take away TCS on remittances for training functions, the place such remittance is out of a mortgage taken from a specified monetary establishment.

8) Tax free withdrawals from NSS

Withdrawals from outdated NSS accounts (Nationwide Financial savings Scheme) will likely be completely tax-free if the funds are withdrawn on or after August 29, 2024. There will likely be no tax legal responsibility on withdrawals from these accounts.

9) NPS Vatsalya Account

It’s proposed to increase the tax advantages accessible to the Nationwide Pension Scheme (NPS) beneath Part 80CCD of the Act to the contributions made to the NPS Vatsalya accounts as nicely. No extra profit is relevant for deposits in NPS vatsalya account.

10) Taxation on ULIPs

- The taxation of ULIPs (Unit Linked Insurance coverage Plans) has been rationalised to supply that every one ULIPs which aren’t exempt beneath part 10(10D) will likely be taxable as capital positive factors just like fairness oriented funds. Presently solely these ULIPs that are bought after 01 Feb 2021 with premium/ aggregage premiums greater than INR 2.5 lakhs p.a. are taxable as capital positive factors.

- Put up the modification, a ULIP bought say in 2005 for which the premium payable in any 12 months exceeds 10% of the particular sum assured, may also be taxable as capital acquire as a substitute of being taxed as revenue from different sources. The ULIPs which had been exempt beforehand will proceed to stay so.

Kindly observe that this text will likely be up to date/edited as and when extra info is accessible.

(Put up first revealed on : 01-February-2025)