In case you’re on Chocolate Finance, you will have seen the newest information that utilizing your Chocolate Visa card can now earn you a candy 2 Max Miles per greenback, and there’s an extra USD possibility on your managed money account with increased curiosity payouts.

I’ll discuss concerning the USD possibility first, since that comes within the aftermath of their SGD charges drop, which shouldn’t come as a shock to anybody by now when you perceive the rates of interest atmosphere and the underlying efficiency of its bond funds.

However how does it work, and is it value signing up for?

Fast Introduction:

Chocolate Finance is a licensed fund administration firm with a CMS license by MAS and a digital adviser serving retail traders specializing in supplying you with higher returns in your money. Based by the Founding father of SingLife (sure, that massive insurer everyone knows who now manages MINDEF insurance coverage), Chocolate Finance was designed to compete with banks as a excessive return money account utilizing a managed account assemble. It isn’t protected by SDIC insurance coverage, identical to how your investments don’t have any such safety.

Not like the banks, which generate returns by investing buyer deposits primarily in mortgages and credit score, Chocolate Finance’s managed account primarily invests in short-duration fixed-income funds and cash market funds, giving them better flexibility to make your cash work arduous for you.

P.S. If that is the primary time you’ve heard of Chocolate Finance, I like to recommend studying these 2 articles first:

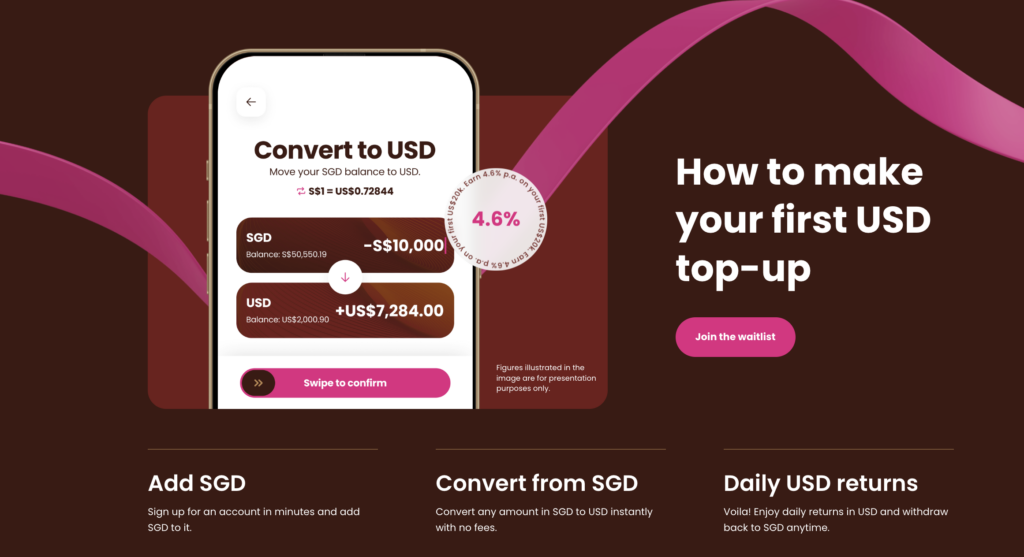

As a buyer, now you can select to both have all your money being managed for you in a SGD account, or so as to add on the USD portfolio as properly.

Right here’s how the charges stack up:

| SGD Account | USD Account | |

| First S$20k | 3.3% p.a. | 4.6% p.a. |

| Subsequent S$30k | 3% p.a. | 4.2% p.a. |

| Above S$50k | Goal 3% p.a. | Goal 4.2% p.a. |

Which means your returns for the primary S$50,000 is assured by Chocolate Finance. In case you choose so as to add on the USD managed account, you’ll then be capable to get double of their assure as much as ~S$135,000* i.e. in your first S$50,000 in SGD and your first US$50,000.

*Be aware that that is based mostly on the prevailing alternate charges, which is at present about 1.36 (USD-SGD).

How does Chocolate Finance earn cash?

As a fund supervisor, they earn when the efficiency is above the charges given out and take a charge of between 0-2%, relying on the extent of outperformance. There is no such thing as a charge in the event that they meet (or fail to satisfy) the acknowledged and goal charges.

In case you’ve already studied their underlying SGD funds earlier than placing your cash in (like I all the time emphasize), then their selection of USD funds mustn’t come as a shock to you. The bulk consists of comparable funds with the identical issuers, besides that it’s denominated in USD.

Even when your cash is being managed by Chocolate Finance, it will be significant that you simply at the very least know what are the underlying funds in every portfolio as it’s the place your cash goes into:

| SGD Portfolio | USD Portfolio |

| Dimensional Quick-Time period Funding Grade SGD Fund (DSF) | Dimensional Quick Time period Funding Grade USD Fund (DSF) |

| Fullerton Quick Time period rate of interest SGD Fund (FST) | Fullerton Quick Time period rate of interest USD Fund (FST) |

| LionGlobal Quick Period Bond SGD Fund (LGF) | LionGlobal Quick Period Bond USD Fund (LGF) |

| Nikko AM Shenton Quick Time period Bond Fund (NST) | abrdn SICAV I Quick Dated Enhanced Revenue USD Fund (ASF) |

| UOBAM United SGD Fund (USF) |

These are fixed-income funds which were fastidiously chosen to optimise risk-adjusted returns based mostly on components like period, yield to maturity, credit score high quality and forex. The funds could change on the sole discretion of the portfolio supervisor; in your app, it is possible for you to to see the data on every fund and the proportion of cash allotted to them.

Is it value getting the USD account?

Whereas the upper charges are engaging, you might want to do not forget that placing your cash in a USD account will inevitably topic you to USD-SGD foreign exchange fluctuations. If the USD weakens in opposition to the SGD, then the upper charges could not find yourself flat in any case. Therefore, whether or not to go for it is going to rely upon you. Listed below are some guiding questions you need to use that can assist you resolve:

- Are you happy with returns in your first S$50,000 in Chocolate Finance?

- In case you favor to place your cash in a financial institution, are the present USD mounted deposits – which vary from 3.09% – 4.25% with a 6 to 12 months lock-up and have minimal quantities of US$5k to US$100k (the best is from UOB) – engaging sufficient for you?

In case you answered no to the above questions, then maybe the USD managed account is value wanting deeper into. Be a part of the waitlist right here or in-app with a purpose to get early entry when it opens!

In case this reminds you of the final Astrea (8) bonds supply that was open to the general public final yr in July 2024, you’re not alone. The distinction? A decrease charge, however with none lock-ups (the Astrea bonds required 5 – 6 years of your cash being locked up in alternate for 4.35% p.a. SGD or 6.35% p.a. USD). The USD supply was oversubscribed by 3.9 instances vs. the SGD supply at 2.9 instances.

Similar to the vast majority of USD funds in Singapore, you can’t deposit USD instantly into your account to begin; as an alternative, you will have to switch SGD first and allow them to do the conversion.

Be aware that the alternate charges within the Chocolate Finance app are based mostly on wholesale market charges with a small margin to cowl forex fluctuations as follows:

• 0.3% adjustment from Monday 5:00 AM SGT to Friday 12:59 PM SGT

• 0.6% adjustment from Friday 1:00 PM SGT to Monday 4:59 AM SGT

Since your USD might be given a 4.6% p.a. in your first US$20k, 4.2% p.a in your subsequent US$30k and a goal 4.2% p.a. on any balances above US$50k, which means with a US$50k stability, clients can anticipate to obtain US$5.80 every day, US$178 month-to-month and US$2,132 yearly of their app.

Upon getting your money working for you in Chocolate Finance, the following query most of you’ll naturally have is whether or not you must click on on that “Apply now” button in your app to get the Chocolate Visa debit card.

Up till final week, my reply had all the time been “no” as a result of there was little cause to get a debit card with zero FX charges when different choices like Belief and Youtrip exist already. Nevertheless, that has now modified as a result of Chocolate Finance has simply introduced their partnership with Heymax to reward clients with Max Miles every time you spend!

In case you have been among the many 3,000 fortunate people who received to attend my free Credit score Playing cards workshop final yr, you’ll be acquainted with HeyMax, which is a miles-hacking device I take advantage of to get additional Max Miles on prime of my bank card miles rewards.

Why you must get the Chocolate Visa Debit Card

Having a card that earns you a candy 2 Max Miles per greenback with zero FX charges, no foolish $5 award blocks and no minimal spend with little or no exclusions on service provider classes is a card that deserves to be a mainstay in any savvy miles collector pockets.

I say this regardless that I’m already an avid bank card consumer who earns wherever between 1.4 – 10 miles per greenback on my spend. Specialised bank cards give the next earn charge of three to 10 mpd, however solely on particular classes of spend. Common bank cards make it simpler to spend wherever else, however the trade-off is lots fewer miles being given (1.2 to 1.4 mpd for most individuals).

So to have a card that provides 2 Max Miles on nearly all the things? That’s a game-changer for certain.

Earn 2 Max Miles on nearly all the things

I foresee this revamped card to turn into a worthy contender within the close to future, as a result of there may be merely no different card that provides you such a excessive earn charge on nearly all the things available in the market proper now.

- There may be no minimal spend required earlier than you begin incomes, and no foolish blocks of S$5 awarded (you get it per S$1).

- Be aware that the two mmpd reward charge is barely given as much as your first S$1,000 spend every month, no matter whether or not you spend this in Singapore or abroad. Watch out to observe for something above S$1,000, which can solely earn you a (unhappy) 0.4 Max Miles per S$1, by which case you’ll be higher off placing your spend on considered one of these bank cards for abroad use as an alternative.

- At zero FX charges, this makes it a greater card to make use of abroad than your Belief or Youtrip card (neither offers you any miles).

- One of the best function concerning the card is that the majority MCCs are included by Chocolate Finance, which incorporates your uncommon Pokemons like insurance coverage premiums, payments, charity donations, schooling faculty charges and even AXS funds (that are usually exempt from card reward programmes). This thus makes it various for these of you who weren’t a fan of routing it by CardUp for a charge to earn 1.2 mpd – 1.8 mpd.

- The Chocolate Visa Card has no minimal revenue requirement and 0 annual charges, making it a nice possibility for college kids to begin incomes miles with.

The one exclusions acknowledged are for money top-ups and monetary establishments, as under:

| MCC | Service provider Class Title |

| 4829 | Cash Transfers |

| 6010 | Monetary Establishments – Guide Money |

| 6011 | Monetary Establishments – Automated Money |

| 6012 | Monetary Establishments – Merchandise, Providers and Debt Reimbursement |

| 6050 | Quasi Money – Monetary Establishments, Merchandise, Providers |

| 6051 | Non-Monetary Establishments – International Foreign money, Cash Orders (Not Wire Switch), Saved Worth Card/Load, Vacationers Cheques, and Debt Reimbursement |

| 6529 | Quasi Money – Distant Saved Worth Load – Monetary |

| 6530 | Quasi Money – Distant Saved Worth Load – Service provider |

| 6540 | Non-Monetary Establishments – Saved Worth Card |

Max Miles by no means expire and could be transformed at a 1:1 ratio to 27 airline and resort companions, with no charges. This makes it arguably extra beneficial than Krisflyer miles, which most of you’ll be extra acquainted with.

To place issues into perspective, when you wished to journey in enterprise class to Tokyo, you solely want 40,000 Max Miles to redeem with Japan Airways, in distinction to 120,000 Krisflyer miles on Singapore Airways!

You’ll be able to apply right here to get your Chocolate Visa Card and add it to your cellular wallets (Google / Samsung / Apple Pay) to begin incomes 2 Max Miles per greenback immediately, even earlier than your bodily card arrives within the mail!

Your funding models might be bought to fund your card spend, whereas your remaining money within the account continues to earn the three% – 4.6% p.a. accordingly.

Essential: Hyperlink to HeyMax to get and monitor your miles earned

In case you don’t have already got a HeyMax account, then you will have to join one right here and pair your Chocolate Visa card with Heymax below the Your Playing cards > Add Card menu tab. A take a look at transaction might be charged and later refunded.

Professional tip: Ensure you click on to affix HeyMax’s public transport marketing campaign right here so that you get 5 Max Miles per greenback once you journey by way of MRT, bus and even bike sharing! (3 Max Miles from HeyMax Visa giveaway + 2 Max Miles from Chocolate Finance’s earn charge.) The marketing campaign runs till 28 February 2025.

TL:DR Conclusion

The Chocolate Visa Debit Card has undergone a revamp and (lastly) offers you rewards on your spend now, at 2 Max Miles per greenback as much as your first S$1,000 anytime, wherever. With most MCCs included, this makes it a lovely possibility for anybody who needs to earn miles on regular excluded spend resembling their payments, insurance coverage premiums, charity donations and even schooling funds.

As on your money in Chocolate Finance, there’ll quickly be a USD managed account possibility launched later this month, which has increased charges of 4% to 4.6% p.a. in your funds. In case you select to go for it, you’ll now take pleasure in charges assured by Chocolate Finance in your first S$50,000 and US$50,000 (vs. simply S$50,000 beforehand).

Would you be signing up for his or her USD account waitlist or activating your Chocolate Visa Debit card in lieu of those provides?

Need to begin incomes every day returns in your cash, or get 2 Max Miles for many excluded MCCs in your Chocolate Visa card?

Disclaimer: This submit was written in response to my readers who've DM-ed me to ask about Chocolate Finance's newest USD supply. Whereas it's NOT sponsored by Chocolate Finance, nevertheless, I've included my very own referral hyperlink as a buyer of Chocolate Finance (which supplies the identical rewards as all your pals').In case you appreciated my work on this text to assist make Chocolate Finance's choices simpler so that you can perceive and decide on, chances are you'll join right here utilizing my referral hyperlink.

With love,

Price range Babe