I preserve listening to that decrease mortgage charges are the silver lining of a worldwide commerce warfare.

That regardless of the inventory market fallout and probably a lot greater costs on account of tariffs, mortgage charges are not less than decrease.

However how a lot decrease are they actually? And at what value? And is anybody really biting, aside from current residence consumers trying to refi?

Whereas there’s nothing flawed with in search of one thing optimistic in these difficult instances, it ought to be famous that charges are nonetheless not removed from 7%.

Actually, one way or the other the 30-year mounted is again to round 6.75% in the present day!

Mortgage Charges Head Again Towards 7%

Whereas the final week and alter was nice for mortgage charges, in the present day hasn’t began so effectively.

As I identified a couple of days, large mortgage charge rallies just like the one we noticed not too long ago are sometimes stopped of their tracks with out warning.

Watch out for the mortgage charge bounce I mentioned, and that’s precisely what we bought in the present day.

The 30-year mounted, which had fallen from 7.25% in mid-January to round 6.60% on Friday, is again to six.75%.

It seemed destined to maintain falling, seemingly hitting 6.50% subsequent, however charges jumped again up in the present day, regardless of one other unhealthy day on the inventory market.

Maybe bonds have but to catch as much as the inventory market, which is extremely unstable in the intervening time.

Possibly bonds want a breather whereas they try to find out President Trump’s subsequent transfer.

However the takeaway right here is mortgage charges are nonetheless solely 25 foundation factors (0.25%) away from 7%, not less than in accordance with MND.

So maybe that silver lining isn’t so silvery in spite of everything.

After having fun with a pleasant down development, mortgage charges appear to have gotten nowhere actually.

Do you know they had been really rather a lot decrease as not too long ago as October of final 12 months?

Whereas your reminiscence would possibly fail you, they had been. The 30-year mounted was mainly hovering round 6%.

Certain, charges are decrease than they had been a 12 months in the past, which could increase residence gross sales this spring, however they continue to be nearer to 7% than 6%.

And days like this make you surprise if we might revisit these ranges once more, which might undoubtedly take the wind out of the very fragile housing market’s sails.

Mortgage Lenders Will Use Any Excuse to Increase Mortgage Charges

The lesson in the present day is that mortgage lenders will use any excuse to extend mortgage charges.

Why? As a result of it’s a lot simpler to play protection, particularly in unsure instances. They don’t need to get caught out on the flawed facet of the commerce.

Keep in mind, they’re providing a hard and fast rate of interest for the following 30 years. They get that flawed and it may be a expensive mistake.

As such, lenders will take their time decreasing rates of interest, but when they get even a sniff of one thing that will increase danger, they’ll elevate them instantly.

Per MND, the 30-year mounted jumped from 6.60% on Friday to six.75% in the present day. That’s a fairly sizable one-day transfer for his or her every day charge survey.

Granted, the 30-year fell by 12 bps on Thursday, adopted by a further 3-bp transfer on Friday, collectively 15 bps.

So your complete enchancment of final week was basically erased in a single day.

That’s form of the way it goes. You must carve out a couple of profitable days to make progress, however at some point can fully unravel it.

It’s two small steps ahead, and one large step again.

However Wait, There’s a Probability This Is Only a Bounce

Earlier than I get too pessimistic right here and quit on the current mortgage charge rally, I ought to observe that this might merely be a bounce.

The inventory market does this on a regular basis. After a couple of down days, there’s a rally. It’s mainly a breather.

Shares and mortgage charges don’t transfer in a straight line up or down, particularly after an enormous rally in a single path.

That could possibly be what we’re seeing in the present day. Granted, in the intervening time each shares and bond yields are decrease, which is rare.

Usually, if shares fall, there’s a transfer into bonds, which will increase their value and lowers their yield (rate of interest).

Not so in the intervening time. Every thing is promoting off as Trump threatens much more tariffs.

It’s as if no person is aware of what to assume, and nothing is protected, not even authorities bonds which are sometimes a protected haven for buyers.

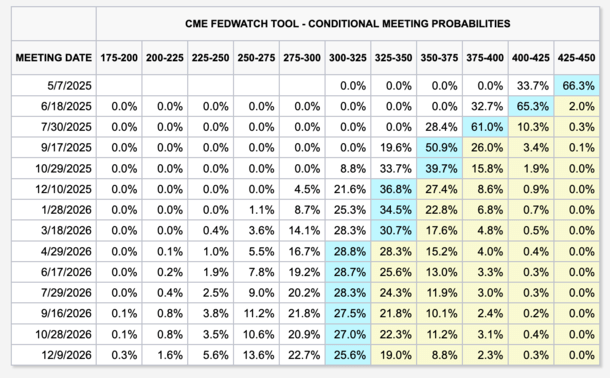

But when we zoom out, right here’s one factor to contemplate. The Fed is now anticipated to chop its personal federal funds charge 4 instances by December, per CME FedWatch.

And whereas the Fed doesn’t set mortgage charges, bonds do take cues from the Fed, and if slicing is anticipated, you would possibly see 10-year bond yields drop.

That tends to translate to greater costs for mortgage-backed securities (MBS), and that results in decrease mortgage charges.

So proper now is likely to be one of the best time to take an extended view as a substitute of getting caught up in day-to-day insanity.

Not straightforward if you must lock or float a mortgage charge within the subsequent few days or even weeks, however reassuring if you wish to refinance your mortgage ultimately. Or maybe purchase a house.

Learn on: Find out how to observe mortgage charges with ease.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Observe me on X for warm takes.