Quickly after the US President introduced – Liberation Day tariffs – I wrote this weblog publish – US authorities is pinning its tariff hopes on some unlikely to be realised assumptions (April 7, 2025) – to assist readers perceive what logic there was, if any, within the determination by the American authorities to impose wide-ranging and seemingly random tariffs on the remainder of the world. The one obvious logic was that his advisors thought that whereas the tariffs would variously improve the US greenback worth on last items and providers out there to US customers by way of imports, the flood of world funding funds into US treasury bonds, because of the heightened international uncertainty would push the US greenback up and offset the tariff impacts on import costs, as a result of all international items would now be cheaper. We now have just a few weeks of information out there to see whether or not issues are turning out as Trump and his advisors thought. The definitive reply up to now is that the alternative traits are rising which can see the burden of the tariffs borne by the US customers and producers reasonably than the presumption of the Administration that the burden could be pushed onto the remainder of the world, which might precipitate fast change within the favour of the US. It appears at current that an ‘personal aim’ is being kicked – and – most likely a variety of them.

The substantive doc that outlines the US authorities’s hopes post-tariff imposition was written Chair of Trump’s Council of Financial Advisors, Stephen Miran in November 2024 – A Consumer’s Information to Restructuring the World Buying and selling System.

He wrote:

Tariffs present income, and if offset by foreign money changes, current minimal inflationary or in any other case adversarial unintended effects, in step with the expertise in 2018-2019. Whereas foreign money offset can inhibit changes to commerce flows, it means that tariffs are in the end financed by the tariffed nation, whose actual buying energy and wealth decline, and that the income raised improves burden sharing for reserve asset provision.

Drawing on the expertise in 2018-2019, throughout Trump’s first time period, Miran wrote:

Throughout his marketing campaign, President Trump proposed to boost tariffs to 60% on China and 10% or greater on the remainder of the world, and intertwined nationwide safety with worldwide commerce. Many argue that tariffs are extremely inflationary and might trigger important financial and market volatility, however that needn’t be the case. Certainly, the 2018-2019 tariffs, a cloth improve in efficient charges, handed with little discernible macroeconomic consequence. The greenback rose by virtually the identical quantity because the efficient tariff charge, nullifying a lot of the macroeconomic influence however leading to important income. As a result of Chinese language customers’ buying energy declined with their weakening foreign money, China successfully paid for the tariff income.

Why would possibly the offset mechanism happen?

A number of components are talked about – none convincing.

He claims that the tariffs will enhance US federal income and financial “deficit issues are more likely to be allayed”, which make US Treasury bonds extra engaging.

He thinks Trump’s choices to “aggressively decontrol parts of the economic system” will enhance financial progress and make US property extra engaging.

World uncertainty additionally helps given the historic behaviour of world traders to maneuver funds to US Treasury bonds in such occasions.

You might ask how a strengthening US greenback helps US producers who’re attempting to promote right into a aggressive world market.

Miran acknowledged that ought to the change charge offset happen then “U.S. exporters now face a competitiveness problem insofar because the greenback has turn out to be extra pricey for international importers”.

His resolution?

An “aggressive deregulatory agenda, which helps make U.S. manufacturing extra aggressive”.

What does that imply?

It must embrace an assault on staff’ wages and circumstances given the proportion of these gadgets in complete manufacturing prices.

He cited this text (April 29, 2024) – A Trillion-dollar 12 months – which was printed by one of many by no means ending Proper-wing propaganda ‘suppose’ tanks within the US which promotes, in their very own phrases, “free-market options”.

The cited article was attacking the US Environmental Safety Company (EPA) determination to guard individuals from PFAS in main water provides eand regulatory guidelines within the US, generally.

The writer thought the prices to enterprise of such safety had been outrageous.

He additionally attacked the EPA for regulating to cut back “tailpipe emissions” in automobiles and to encourage EV use.

Nevertheless, lowering “paperwork” gained’t make the distinction between US manufacturing being internationally aggressive once more versus not being so.

They must severely lower wages.

Estimates previously discovered that “China’s unit labour prices” (which mix wage prices with productiveness estimates) had been round 25 to 40 per cent of the US unit labour prices.

Additional, whereas wages progress is accelerating in China because the emergence of the center class substantiates, labour productiveness progress is extra fast (by some) than it’s within the US.

There was after all contradictions within the stance taken by Miran.

He additionally famous that the US President has “mentioned adopting substantial modifications to greenback coverage. Sweeping tariffs and a shift away from sturdy greenback coverage” as a result of from “a commerce perspective, the greenback is persistently overvalued, largely as a result of greenback property operate because the world’s reserve foreign money.”

If the US greenback, the truth is, weakens on the identical time the tariff is imposed then the aforementioned ‘offsets’ of the tariff influence on US costs by means of the exhange charge don’t happen.

In reality, the change charge influence would heighten the tariff influence and worsen the scenario confronted by US customers.

What has occurred?

Issues should not panning out as Miran prompt.

First, as a part of the newest World Financial Indicators launch, the IMF prompt (April 22, 2025) that – The World Financial system Enters a New Period.

They pointed to the tariff choices as resetting the “international financial system below which most nations have operated for the final 80 years” which is creating “epistemic uncertainty and coverage unpredictability” and the “attendant uncertainty will considerably gradual international progress”.

For as soon as I agree with the IMF.

The IMF has decreased its estimate of US progress from 2.8 per cent (printed in January 2025) to 1.8 per cent in April.

In line with their calculations, “tariffs account for 0.4 proportion level of that discount.”

Additionally they elevated the “US inflation forecast by about 1 proportion level, up from 2 %.”

The next graph exhibits the newest progress forecasts from the IMF.

It’s clear that they suppose the tariffs will injury US progress greater than some other nation proven.

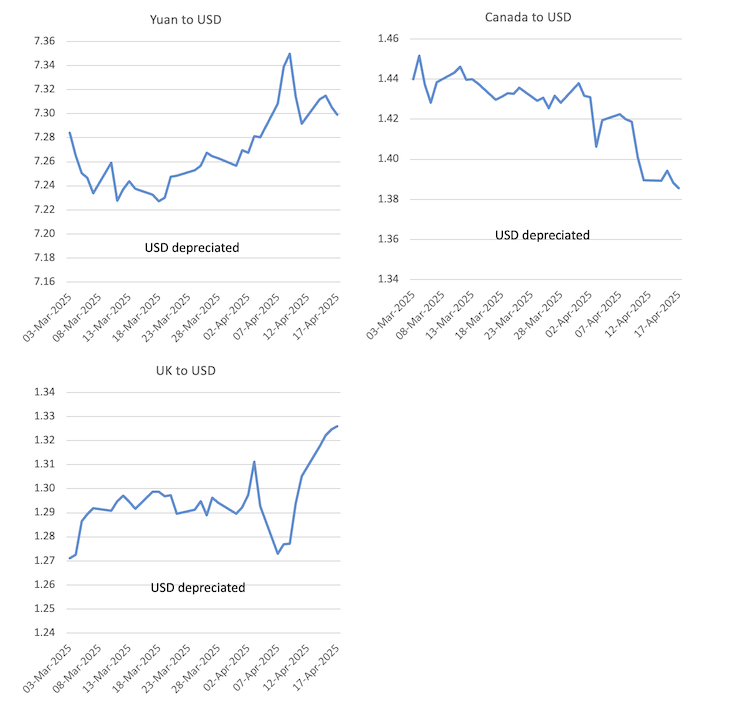

The actions in change charges have additionally been reverse to that required to offset the value impacts of the tariffs.

Listed below are some chosen nations.

Be aware the citation within the charges will not be uniform, that means that when the Australian greenback rises towards the US greenback, it’s an appreciation, whereas, for instance, it’s the reverse for the yen and peso.

Nevertheless, in every of the instances proven, the USD has depreciated.

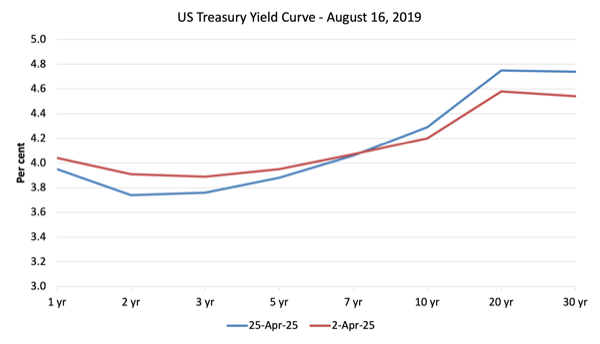

There has additionally been a variety of information these days about the best way the bond markets are defying previous historical past by transferring funding funds out of US Treasury bonds regardless of rising uncertainty that’s normally related to the alternative motion of funds.

Final week, Reuters reported (April 24, 2025) – Japanese traders turned web patrons of abroad bonds final week – that:

U.S. Treasury yields have climbed this month, as bonds bought off, with hedge funds unwinding leveraged foundation trades and abroad traders promoting U.S. debt in obvious retaliation for tariffs and amid rising doubts concerning the safe-haven standing of U.S. property.

Japanese traders are the biggest holders of U.S. Treasuries with roughly $1.13 trillion in holdings.

In the meantime, abroad traders have been buying Japanese property, pushed by safe-haven demand and expectations that the Financial institution of Japan is more likely to delay its rate of interest hike to be able to help the economic system.

The UK Guardian article (April 9, 2025) = Dramatic sell-off of US authorities bonds as tariff conflict panic deepens – additionally reported comparable traits.

It mentioned: “US authorities bonds, historically seen as one of many world’s most secure monetary property, are struggling a dramatic sell-off as Donald Trump’s escalation of his tariff conflict with China sends panic by means of all sectors of the monetary markets.”

Right here is the US yield curve for short- and long-term Treasury bonds on April 2, 2025 and April 25, 2025 (most up-to-date out there knowledge).

Not solely has there been an general sell-off but in addition a change into shorter-term bonds because the uncertainty will increase.

The upper longer-term yields will appeal to funds again into the US, which we now have seen within the final week or so.

However the actuality is kind of totally different to that predicted by the Chairman of Trump’s key financial advisory physique the Council of Financial Advisors.

Conclusion

It’s nonetheless solely a month or so because the US liberated itself and these processes don’t happen in a single day.

So it might nonetheless work out the best way Miran and Co hope.

However I doubt it.

It’s trying very very like an personal aim at this stage.

I clearly maintain my eye on these traits and as they are saying ‘we are going to see’.

That’s sufficient for at the moment!

(c) Copyright 2025 William Mitchell. All Rights Reserved.