It’s no secret sure of us don’t like Fed Chair Powell. You might have heard of one in every of them, President Donald Trump, who refers to him as a “Too Late Powell.”

He additionally calls him different names that I gained’t repeat right here.

Now he’s obtained one other sturdy critic in FHFA Director Invoice Pulte, whose company oversees Fannie Mae and Freddie Mac.

These two corporations are accountable for many of the mortgages in existence, with conforming loans far and away the most typical mortgage sort on the market.

Because of this, Pulte has referred to as on Powell to decrease charges or resign, the strongest phrases he’s uttered since taking the helm on the FHFA.

Lower Charges or Resign Powell

Pulte went off in a sequence of posts on X, saying very instantly, “I’m calling for Federal Reserve Chairman, Jay Powell, to resign.”

He adopted that tweet with extra one-liners, together with, “There isn’t any reliable factual foundation to maintain charges excessive. None.”

And this one: “Individuals are sick and uninterested in Jerome Powell. Let’s transfer on!”

However he was simply getting began. He went on to put in writing, “…he’s hurting Individuals and hurting the mortgage market, which I’m accountable for regulating.”

Then defined how Powell is “the primary cause” now we have a so-called housing provide disaster in our nation.

That “by improperly protecting rates of interest excessive,” Powell has trapped householders in low-rate mortgages whereas choking off for-sale provide.

He ended that tweet by repeating that “He should decrease charges.”

So it’s fairly clear Pulte, like Trump, isn’t a fan of Powell. That’s tremendous. Everybody has a proper to their very own opinion.

And maybe rates of interest must be decrease in the present day. But it surely must be famous that the Fed doesn’t management mortgage charges.

They management their very own coverage price, the short-term fed funds price, which doesn’t have a transparent relationship with the 30-year mounted over time.

Which means if Powell have been to chop the Fed price tomorrow, or a pair days in the past at their assembly, the 30-year mounted wouldn’t essentially reply in any anticipated method.

The truth is, the 30-year mounted may very well be larger in consequence. When you recall again in September when the Fed minimize charges, mortgage charges elevated.

I wrote about that already, and the takeaway is that it’s an advanced relationship.

We Can’t Bully Our Option to Decrease Mortgage Charges

On the finish of the day, we will’t pressure mortgage charges decrease by yelling at Powell and the opposite Fed members to decrease charges.

They don’t management long-term charges just like the 30-year mounted. Undecided what number of occasions that must be stated, nevertheless it’s getting tiresome.

The one method they will truly, instantly decrease mortgage charges is through one other spherical of Quantitative Easing (QE), the place the Fed buys Treasuries and residential mortgage-backed securities (MBS).

This was how mortgage charges hit report lows in 2021 within the first place, and in addition why we’re on this mess in the present day.

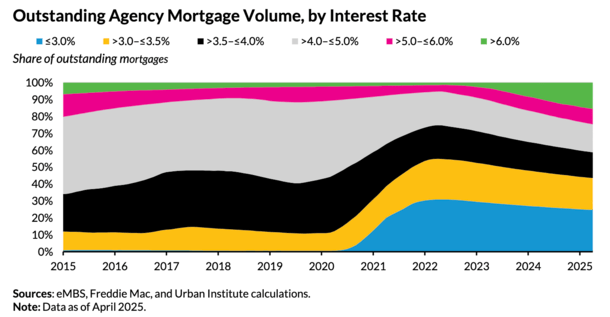

To Pulte’s level about householders being trapped in low-rate mortgages, that’s a phenomenon often called the mortgage price lock-in impact.

It’s the results of householders taking out 2-4% fixed-rate mortgages and now dealing with charges nearer to 7%.

The massive hole in charges (see chart above from the City Institute) makes it much less compelling to maneuver, and thus householders keep put, which additional exacerbates the present housing provide scarcity.

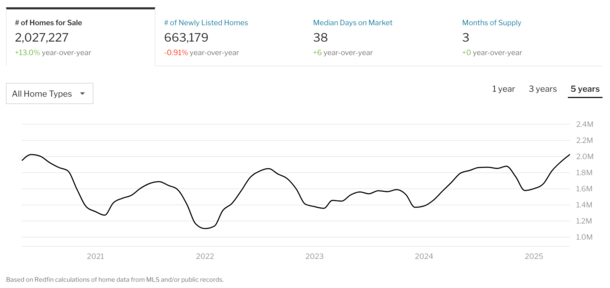

Housing Provide Is Lastly Rising and Up 13% From a 12 months In the past

Nonetheless, provide is rising quickly and ultimately look, is up 13% from a yr in the past, per Redfin.

And it’s lastly getting again to pre-pandemic ranges, when house patrons scrambled to benefit from the bottom mortgage price in historical past, depleting provide within the course of.

So we’re transferring in the best path partially due to larger mortgage charges, which have cooled demand and led to raised equilibrium between purchaser and vendor.

Slicing charges simply to spice up affordability may not enable that course of to proceed. And as famous, that’s not the way it works anyway.

The underlying financial information must assist price cuts, which might additionally drive bond yields decrease (and by extension mortgage charges too) earlier than a Fed price minimize.

It’s a course of that takes time and it’s taking part in out. We simply should be affected person and we’ll get there, whereas additionally making a sustainable path to affordability.

The housing market doesn’t want rock-bottom mortgage charges once more. It wants normalcy. And if we’re affected person, that’ll come.

If we manipulate the market (how we obtained on this mess to start with), but once more, as we did with a number of rounds of QE, we’ll simply create larger issues and proceed to kick the can.

(picture: iandesign)

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house patrons higher navigate the house mortgage course of. Comply with me on X for decent takes.