RSU or Restricted Inventory Items are shares of the corporate given to workers freed from price however with some restrictions. What are RSUs? Why are RSUs given? What’s the vesting date? When are RSU taxed? Is there a capital achieve on promoting RSU? What’s the capital achieve from promoting RSU? We will reply these questions by speaking in regards to the RSU of an American MNC.

Overview of RSU, Tax, and ITR

RSU or Restricted Inventory Items are shares of the corporate given to worker freed from price however with some restrictions(because the identify suggests)

- On Granting of RSU no tax implication. It’s only a promise by the employer

- On the vesting day, the given share of RSUs are transferred to worker’s buying and selling account.

- Worker has to pay tax primarily based on his earnings slab.

- the worth of shares is taken into account as Perquiste in India and seems in Kind 16. The market worth of the shares vested (variety of shares vested x Honest Market worth X Conversion from Greenback to Indian Rupee) is added to the worker’s taxable earnings as perquisites. The value at which Inventory is given to you is named because the Honest Market Worth

- Tax could be deducted within the different nation.

- US MNCs with workers in India typically submit W-8BEN to US brokers to keep away from any withholding associated to US taxes.

- Indian firms deduct % of shares as tax.

- There’s no double taxation as tax is paid from the sale of shares.

- One must declare shares acquired as RSU as Capital Asset in Schedule FA(Overseas Property) of ITR2, ITR3, ITR4.

- ITR1 does NOT have the schedule for Overseas Property. So for those who RSU, ESPP in MNC you can’t file ITR1.

- It is best to fill in details about all of the RSUs you could have as of the monetary yr of the MNC

- It is best to present earnings you derived from it(Dividend, Capital Positive aspects).

- If tax for RSU has been deducted by promoting of shares, Variety of shares talked about must be after the deduction. So if 100 shares obtained vested and 30 shares had been deducted then it is advisable present solely 70 shares in Overseas Property.

- One can solely promote the RSUs which are vested. On the sale of the vested shares, the revenue earned is a capital achieve and is due to this fact taxable in India.

- For RSUs, the distinction between the vesting worth or the Honest Market Worth and the sale worth is the as capital achieve

- For RSUs, the acquisition date is the vesting date.

- Because the RSUs of the MNCs will not be listed on the Indian inventory change and no STT(Safety Transaction Tax) is paid so the definition of a long run and short-term capital positive factors is totally different from the shares listed on Indian inventory change like BSE and NSE.

- Brief-term capital property – when offered inside 24 months of holding them. Brief-term positive factors are taxed at worker’s earnings tax slab charges

- Lengthy-term capital property – when offered after 24 months of holding them. Lengthy-term positive factors are taxed at 12.5% (earlier than Lengthy-term positive factors are taxed at 20% with indexation earlier than Price range 2024)

- This capital achieve should be declared in Schedule CG of ITR2 ITR3, ITR4 for tax functions.

- Advance Tax must be paid for revenue/capital achieve of greater than 10,000 Rs.

The reporting could be as beneath for overseas shares on

- Schedule CG for Capital achieve on Sale of Shares

- Schedule OS for Dividend earnings

- Schedule FSI and Schedule TR for claiming the overseas tax credit score in case of double taxation aid

- Schedule FA: Particulars of holding of overseas shares/securities

RSU or Restricted Inventory Items

RSU or Restricted Inventory Items are shares of the corporate given to worker freed from price however with some restrictions(because the identify suggests). The restriction is that although an worker is granted RSUs on a selected day (comparable to when he joins an organization or will get a promotion) he will get possession of the shares over a time frame. It’s an incentive to the worker to remain within the firm and to revenue from the expansion of the corporate. When the shares are awarded to the worker in line with the schedule, it’s thought-about as perquisite earnings and added to common earnings. When one sells the RSUs one capital achieve comes into play and one could should pay tax relying on the interval of holding of RSU. Phrases related to RSU.

- Grant date: The date on which the shares are allotted

- Vesting date: the date on which the shares get transferred to the worker.

Say if one is granted 100 RSUs to be vested over 3 years within the ratio 34%/33%/33% on 23 Nov 2023. Then 34 RSUs (34%) will vest on 23 Nov 2024 and 33 every (33%) on 23 Nov 2025 and 23 Nov 2026 respectively. When you depart the corporate on 1 December 2025, then it is possible for you to to promote solely 34 shares and the remaining 66 shares will return to the corporate. When you stick round for one more month, then it is possible for you to to promote 67 shares (34 + 33) as one other 33 shares will vest on 23 Nov 2025.

So if one is granted 100 RSUs to be vested over 4 years within the ratio 25%/25%/25%/25% on 16 Dec 2023. Then 25% of RSUs i.e 25 shares of the corporate will vest on 16 Dec 2024, on 16 Dec 2025, 16 Dec 2026 and 16 Dec 2027 respectively. (If the vesting day is vacation then the shares vest on subsequent working day)

The opposite form of incentives provided by the businesses are ESPP and ESOP.

Our article What are Worker Inventory Choices (ESOP) explains ESOP intimately.

Our article Worker Inventory Buy Plan or ESPP explains ESPP intimately.

Tax when RSUs are Granted

On Granting of RSU no tax implication. It’s only a promise by the employer.

Tax when RSUs are Vested

Vesting date is the date on which the predefined share of shares get transferred to the worker in line with the predefined schedule. Say one is granted 100 RSUs to be vested over 4 years within the ratio 25%/25%/25%/25% on 16 Dec 2023. Then 25% of RSUs i.e 25 shares of the corporate will vest on 16 Dec 2024. On the vesting day, the given share of RSUs are transferred to worker’s buying and selling account, for instance, eTrade or Charles Schwab account for an American MNC. On Vesting, one has to maintain following issues

- one has to pay tax primarily based on earnings slab.

- the worth of shares is taken into account as earnings in India.

Tax on RSU

Firms are obligated to deduct taxes for RSUs vested. The commonest methodology of deducting tax is share withholding, the place the corporate withholds sufficient shares to cowl the tax legal responsibility and deposits internet shares to your brokerage account. This feature is named as Promote to cowl. Some firms allow different strategies, comparable to money or sell-to-cover transactions, that are defined beneath. Totally different strategies could also be supported by buying and selling firms like Schwab or eTrade, however solely the strategies approved by your organization shall be out there to you.

The assorted choices to deduct tax on broking web site the place the RSUs are held are as follows:

- A sell-to-cover That is the default choice the place TDS (as per your earnings slab) share of the vested shares are offered instantly and the quantity is paid to the federal government as tax. The remaining 70% of the vested shares stay in your account and you may promote them later everytime you need. Actully tax deducted is as per the earnings slab however as in many of the firms, the RSUs are provided above a sure degree the place earnings is available in 30% earnings slab.

- A same-day sale: All of the vested RSUs are offered instantly. Proportion of the sale proceeds are deducted and paid as tax to the federal government and the remainder of cash will get wired to your account. You don’t any shares after this.

- A money train permits you to pay the tax and no shares are offered. The cash to pay should be out there in your brokerage account.

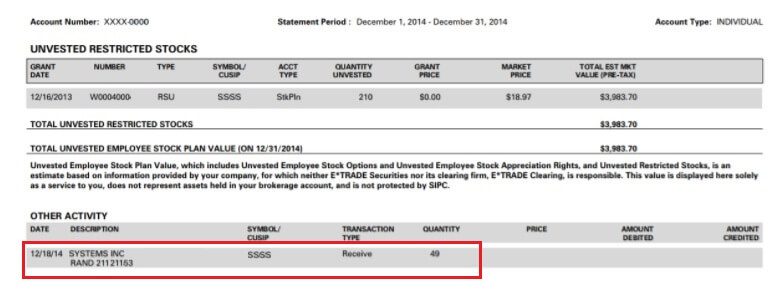

The default choice is Promote to Cowl therefore If 70 RSUs are vested you then would get solely 49 shares in your account resulting from taxation. 30% of 70 = 21 which is taken as tax. So no of shares within the account turns into 70-21=49.

RSU Awarded after promoting of shares for Tax

RSUs as Perquisite Revenue in India

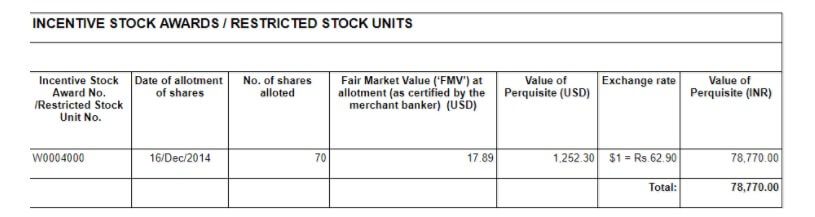

For RSUs, the acquisition worth or buy worth is zero and so the whole market worth of vested shares is handled as earnings in India as a perquisite. The market worth of the shares vested (variety of shares vested x Honest Market worth X Conversion from Greenback to Indian Rupee) is added to the worker’s taxable earnings as perquisites. The value at which Inventory is given to you is named because the Honest Market Worth. All of the shares which are vested are used to calculate the Perquiste Revenue which incorporates the shares which had been offered for tax. if 70 RSUs are vested you then would get solely 49 shares in your account resulting from taxation however all of the 70 shares shall be used to calculate the perquiste earnings.

Calculating Perquiste earnings for RSU

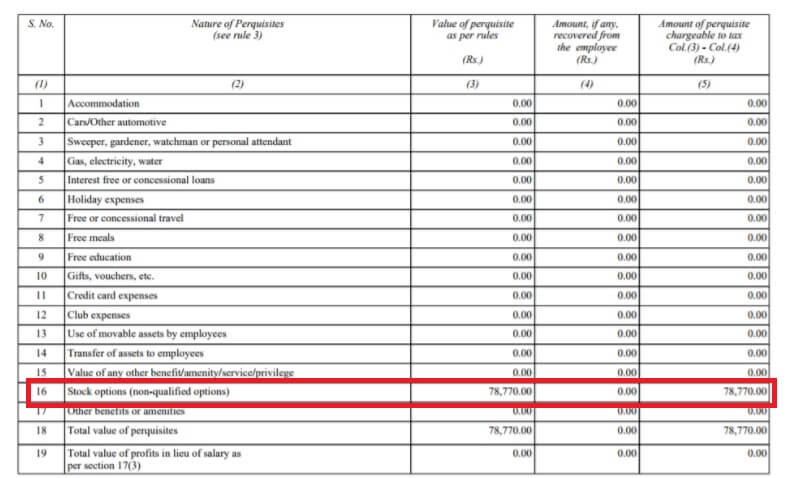

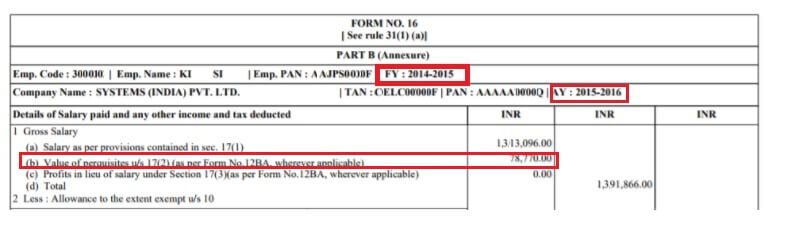

It’s declared in his Kind 12BA for the yr and is on the market in your Kind 16, as proven within the photographs beneath. The Indian firm provides it to worker’s Revenue and costs Tax accordingly.

Perquisite Revenue in Kind 12BA

Our article Understanding Kind 12BA give particulars of Perquisites given to an worker intimately.

Kind 16 displaying Perquisite Revenue

Our article Understanding Kind 16: Tax on earnings explains the Kind 16. Revenue Tax Kind 16 is a certificates from the employer which certifies that TDS has been deducted from worker’s wage by the employe

Are RSU’s Taxed Twice?

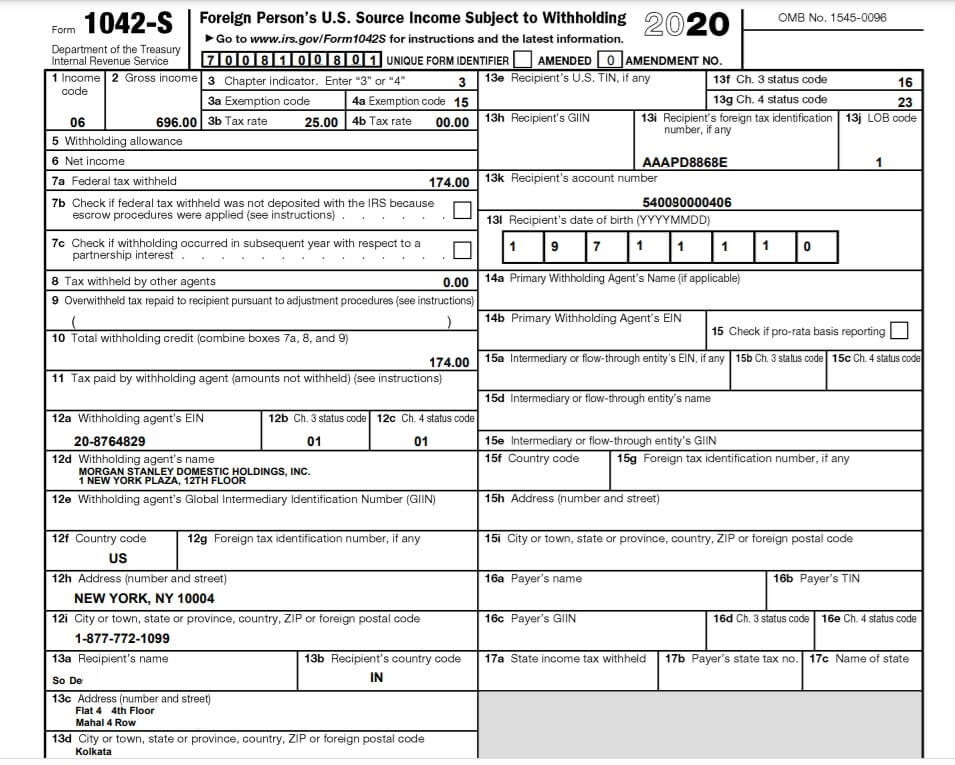

Brief Reply is RSU’s will not be taxed twice. If they might have been taxed twice you’d have Govt doc of the nation deducting tax saying that tax has been deducted. Like Kind 16/Kind 16A offered by Indian Govt or Kind 1042-S offered by US when the tax is deducted on the dividend of US compnaies.

An worker (Resident Indian) working in India in a subsidiary of a US Firm is given RSU or Restricted Inventory Items of the dad or mum firm.

When the shares are vested, some shares are withheld (Promote to cowl) to fulfill tax legal responsibility in US and after decreasing these shares, the stability is given to the worker.

Indian firm additionally calculates prerequisite primarily based on FMV on the full variety of shares together with withheld shares and TDS is deducted. That is mirrored in Kind 16 Half B.

So are RSUs are taxed twice. About 65.22% worth is consumed in tax.

Is double taxation performed by the corporate is appropriate?

Can DTAA advantages be availed for a refund?

No, RSUs will not be taxed twice is what my firm says. Simply since you are seeing that in your Kind 16 and your brokers statements, it doesn’t imply that its been deducted twice.

Within the instance above, Reader Smriti defined fantastically.

100* FMV was added to your prerequisite to indicate it as part of earnings. it simply means you had been paid a 100*FMV quantity by the corporate( in type of shares).

66 shares are deposited to your brokerage account.

The remaining shares (100-66 = 34) are thought-about to be offered by the dealer in your behalf and the quantity obtained from that is paid as tax.

All these calculations are a part of your wage prerequisite and therefore, will present in your wage slip because the tax you’re paying to Govt of India.

The employer will not be deducting tax twice. it’s simply including all the main points within the payslip.

We’ve heard that Proof is within the pudding or present me the proof. If the tax had been deducted by the overseas firm then they should present paperwork like Kind 16/Kind 16A in India and Kind 1042-S within the US. The Pattern Kind 1042-S from our article How are Dividends of Worldwide or Overseas Shares taxed? The best way to present in ITR is proven beneath.

1042-S which exhibits Tax on Dividend deducted

Dividend earnings from overseas shares

Dividend earnings earned from overseas shares is taxed as per Revenue Tax slabs beneath the pinnacle Revenue from Different Sources.

In Schedule TR, it is advisable present a abstract of tax aid that’s being claimed in India for taxes paid exterior India in respect of every nation. This schedule captures a abstract of detailed data furnished in Schedule FSI.

Within the case of sure ESOPs, a person may obtain dividend-equivalent earnings on unvested shares. These are typically taxed as a part of wage earnings.To find out one’s taxation it’s advisable to have a chat together with your Employer or colleagues.

The Double Taxation Avoidance Settlement or DTAA is a tax treaty signed between India and one other nation in order that taxpayers can keep away from paying double taxes on their earnings earned from the supply nation in addition to the residence nation. At current, India has double tax avoidance treaties with greater than 80 international locations around the globe.

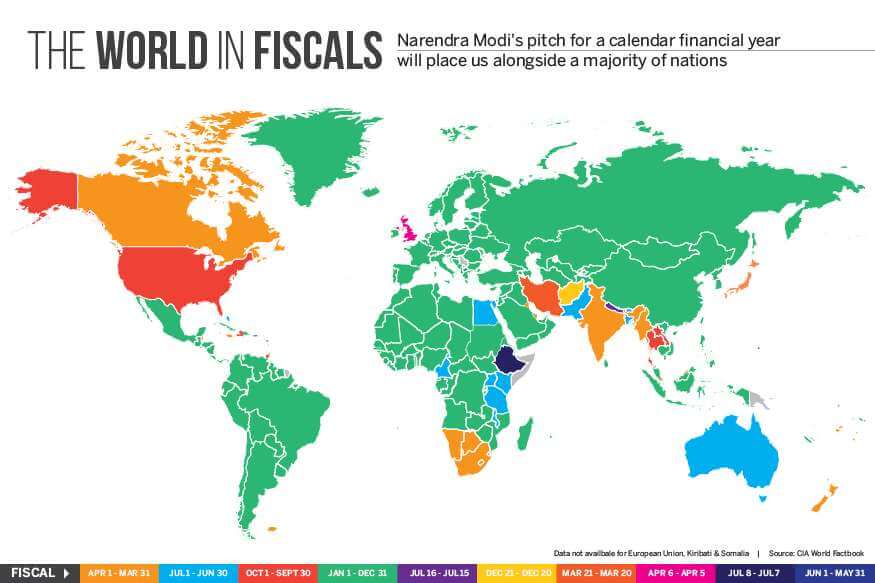

Monetary years of various international locations

“It’s hereby clarified {that a} taxpayer shall be required to reply the related query (whether or not overseas property are held or not) within the affirmative, provided that he has held the overseas property and so forth. at any time in the course of the “earlier yr”(in India) as additionally at any time in the course of the “related accounting interval”(within the overseas tax jurisdiction), and replenish Schedule FA accordingly.”

Lets take an instance of RSUs of a MNC headquartered in USA which has monetary yr from 1 Jan to 31 Dec. So solely RSUs(ESPPs) acquired between 1 Jan 2022 to 31 Dec 2023 must be reported.

Monetary years for widespread international locations are given beneath

1. United States: Monetary yr is from January 1st to December thirty first.

2. United Kingdom: Monetary yr is from April sixth to April fifth.

3. Canada: Monetary yr is from January 1st to December thirty first.

4. Australia: Monetary yr is from July 1st to June thirtieth.

5. United Arab Emirates: Monetary yr is from January 1st to December thirty first.

For particulars checkout our article Distinction between Evaluation 12 months and Monetary 12 months, Earlier 12 months,Fiscal 12 months in World

Monetary Years in several international locations of the world

The best way to present RSU, ESPP, and Overseas Property in ITR

One wants to indicate shares acquired as RSU(ESPP/ESOP) as Capital Asset in Schedule FA(Overseas Property) of ITR apart from ITR1 comparable to ITR2, ITR3, ITR4 as proven within the picture beneath. ITR1 does NOT have the schedule for Overseas Property.

The picture beneath exhibits the case of solely when shares of an organization within the US had been allotted to the worker and the worker has not offered them until submitting of the earnings tax return. To fill this please undergo Perquisite on Inventory Choices report and the break up offered by your employer on shares allotted to you.

If tax for RSU has been deducted by promoting of shares, the Variety of shares talked about must be after the deduction. So if 100 shares obtained vested and 30 shares had been deducted then it is advisable present solely 70 shares in Overseas Property. Whole Funding values is the Variety of shares in your account X Honest Market Worth X US greenback inventory worth.

When you’ve got obtained RSU at totally different instances and also you haven’t offered them then particulars about every allotment you had until 31 Mar of the monetary yr for which you’re submitting ITR needs to be put within the Overseas Property desk.

For instance, your 70 RSUs obtained vested in 2020 and 70 in 2021, the details about each the allotments must be in Overseas Property.

Schedule for Overseas Revenue in ITR

Distinction between Schedule Overseas Supply Revenue (FSI) and Overseas Property (FA)

Is Schedule FSI required to be stuffed in ITR2?

I’m resident in India. I’ve been allotted inventory choices (of my dad or mum US firm), which have been proven in my Kind 16. Do I additionally want to indicate this earnings in Schedule FSI or Schedule FA (Overseas Property)? No Tax has been deducted within the US and I’m not claiming any refund.

- In Schedule Overseas Supply Revenue (FSI), it is advisable report the main points of earnings, which is accruing or arising from any supply exterior India. FSI schedule is obligatory for residents who earned earnings from exterior India and tax paid exterior India and to say the advantage of DTAA on such earnings.

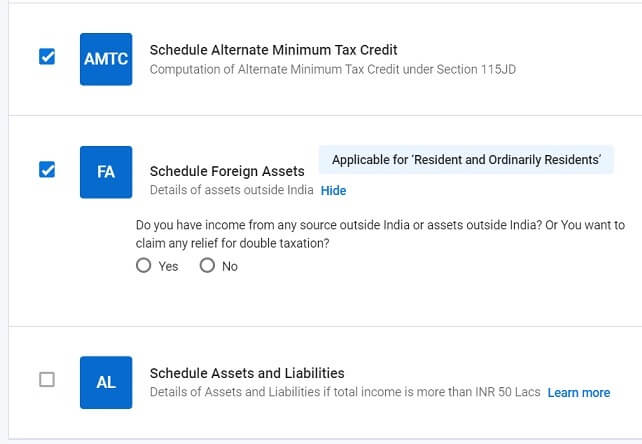

The best way to choose the Schedules?

Go to Schedule Choice

- Click on Revenue to see the Revenue from Capital Positive aspects Schedule. Choose the Schedule

- Click on Revenue to see the Overseas Supply Revenue schedule. Choose the Schedule

- Click on Others to see the Overseas Property Revenue schedule. Choose the Schedule

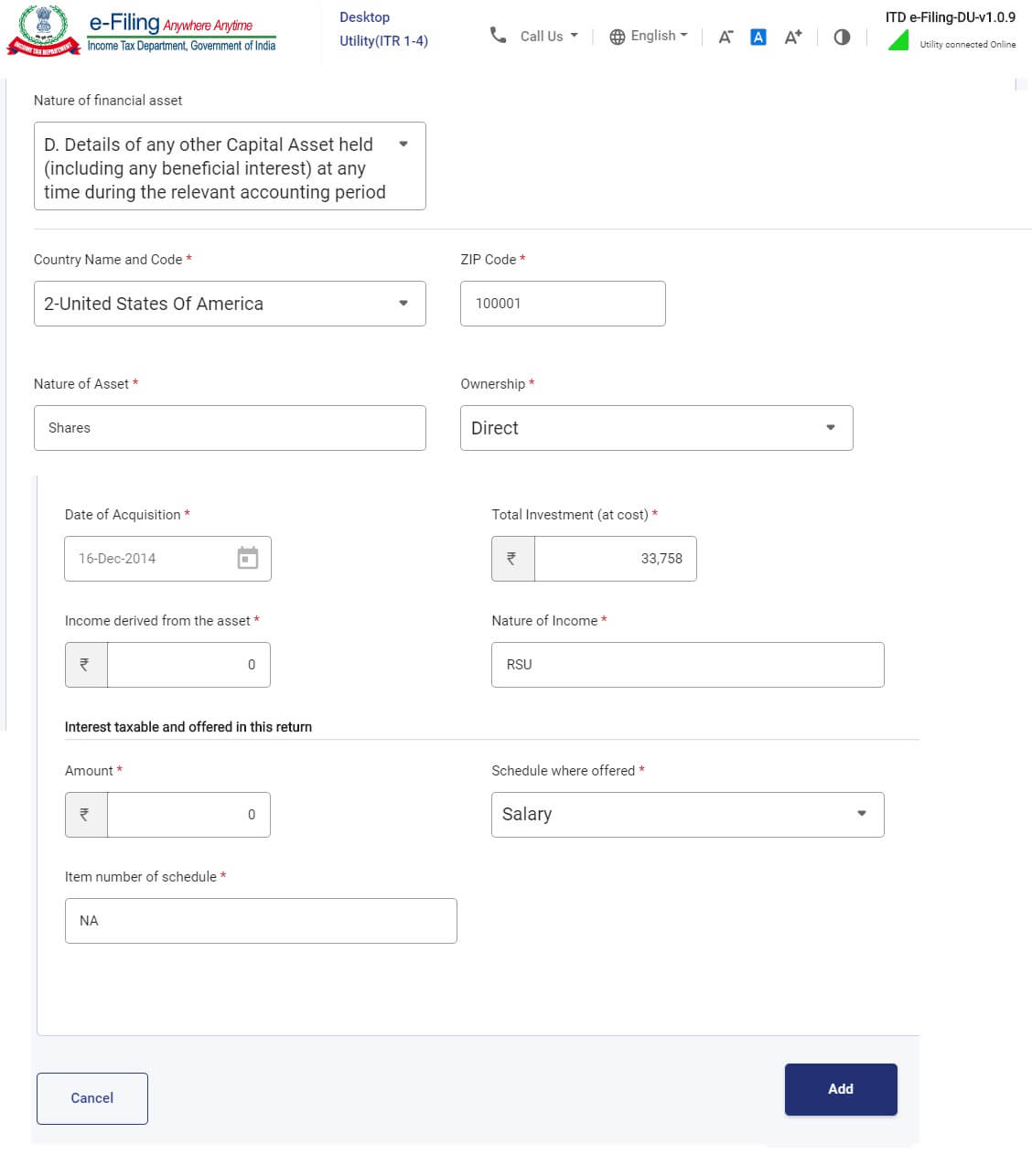

Choose schedule for Revenue from Overseas Property

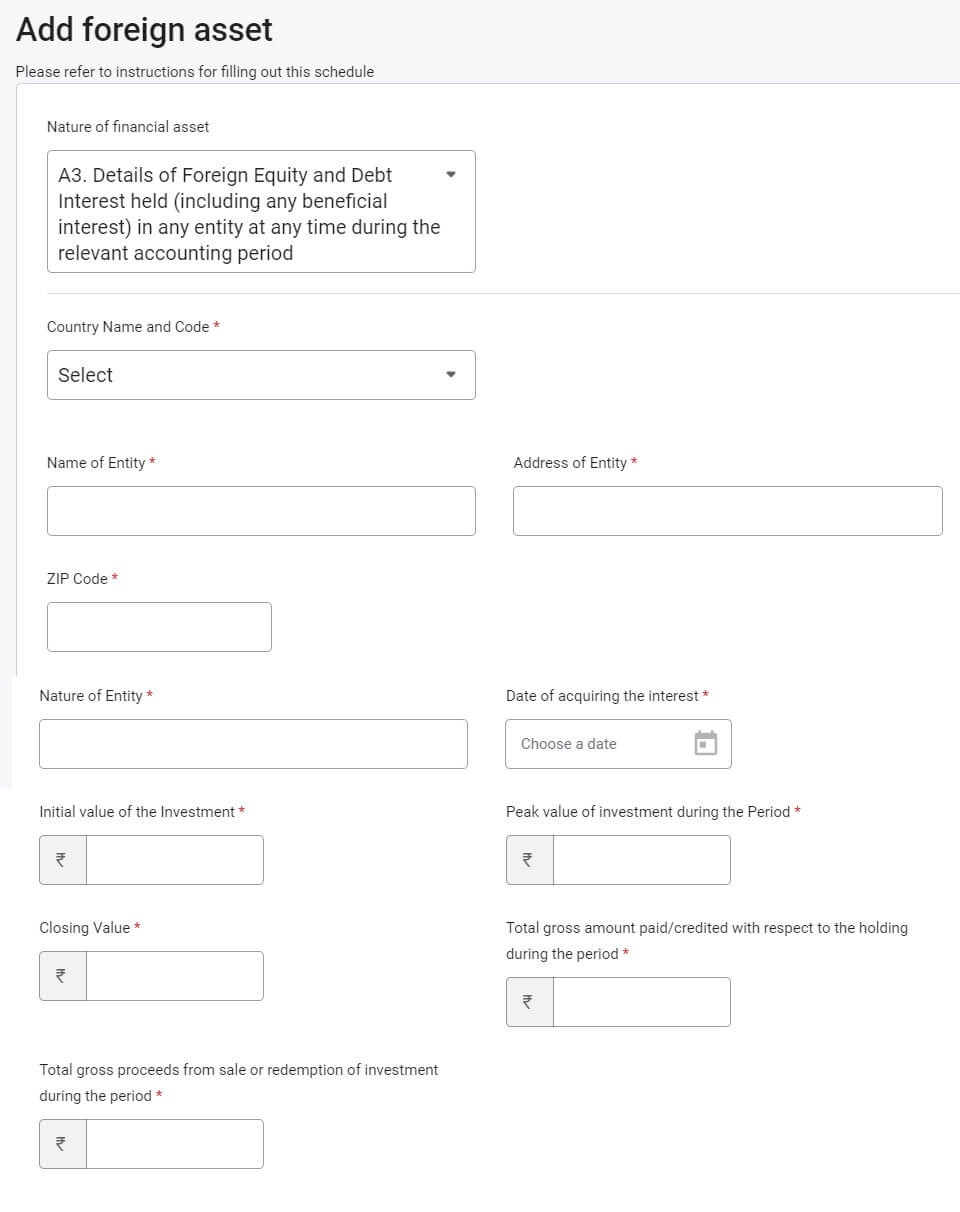

Particulars to be stuffed in Overseas Asset schedule in ITR2

Particulars to be stuffed are:

- Nation Title and code: The Nation the place the change on which shares are listed is traded. Ex for somebody working in Amazon or Microsoft, it will be the USA. Code is on the market within the dropdown in ITR.

- Nature of asset: Shares

- Nature of Curiosity-Direct/Useful/proprietor/Beneficiary: Direct

- Date of acquisition: Date on which shares had been allotted

- Whole Funding (at price) (in rupees): Worth at which RSU/ESPP was allotted. (Please deduct the variety of shares that had been credited to your account after-tax deduction. Say you had been allotted 70 shares however due to tax solely 49 shares had been credited into your broking account). In instance 49*17.89(FMV)*62.90(USD Alternate charge)

- Revenue accrued from such :

- 0, for those who haven’t offered the shares.

- When you’ve got earned a dividend then declare the dividend acquired.

- When you’ve got offered the shares then you need to present the revenue/loss acquired from the sale of the shares.

- Nature of Revenue: What sort of Revenue it’s. For Overseas shares not offered it’s Revenue from Wage. For Overseas shares offered it’s earnings from Capital Positive aspects.

Desk A3 or Desk D

You’ll be able to declare it in Desk A3 or Desk D of Overseas Property as proven within the photographs beneath

Technically it must be declared in Desk A3. Additional particulars required in Desk A3 are the Peak Worth of funding in the course of the interval, Closing Worth. Closing Worth must be as of 31 Mar. These particulars you’ll find out of your dealer.

In desk A3, the preliminary worth of the funding, the height worth of the funding in the course of the accounting interval, the closing worth of the funding as on the finish of the accounting interval, gross curiosity paid, the full gross quantity paid or credited to the account in the course of the accounting interval,and whole gross proceeds from sale or redemption of funding in the course of the accounting interval is required to be disclosed after changing the identical into Indian forex

ITR new overseas property Desk A3

However because it requires extra particulars, many individuals do it in Desk D, the rationale being we’re declaring the earnings and account for it.

Desk A3 and Desk D within the previous ITR

Desk A3 and Desk D within the previous ITR

Declare RSU/ESPP in Overseas Property in ITR

RSU as Overseas Property in ITR

Our article Are ESPP, ESOP in MNC to be filed in ITR as Overseas Property? discusses What are overseas property? The Overseas Asset schedule in ITR2.

Tax On Sale of RSU

One can solely promote the RSUs which are vested. On the sale of the vested shares, the revenue earned is a capital achieve and is due to this fact taxable in India.

For RSUs, the distinction between the vesting worth or the Honest Market Worth and the sale worth is the capital positive factors.

Because the RSUs of the MNCs will not be listed on the Indian inventory change and no STT(Safety Transaction Tax) is paid so the definition of a long run and short-term capital positive factors is totally different from the shares listed on Indian inventory change like BSE and NSE.

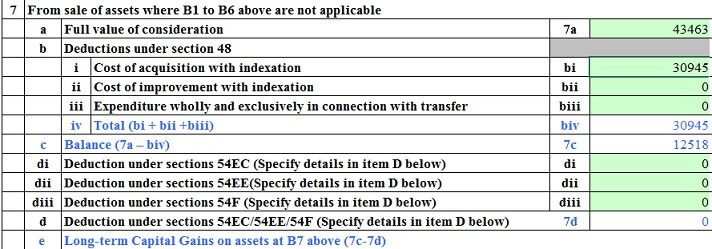

From FY 2016-17 i,e for the sale of unlisted shares on or after 1st April 2016 UNLISTED fairness shares is given beneath. This capital achieve should be declared in Schedule CG of ITR in order that tax could also be suitably charged

- short-term capital property – when offered inside 24 months of holding them. Brief-term positive factors are taxed at worker’s earnings tax slab charges

- long-term capital property – when offered after 24 months of holding them. Lengthy-term positive factors are taxed at 20% with indexation (so part 48 which makes use of Indexation applies)

The earnings tax Act in India act differentiates between the tax on capital positive factors of listed and unlisted shares.

- Listed shares are these which are listed on Indian inventory exchanges, comparable to TCS, HDFC Financial institution, and so forth.

- Unlisted shares are these that aren’t listed on Indian exchanges, no matter whether or not they’re of Indian firms or overseas firms listed on overseas exchanges comparable to Google, Microsoft, Apple, and so forth.

The tax therapy on capital positive factors which are unlisted in India or listed out of India is similar. So for those who personal shares of an American firm, this firm will not be listed in India, therefore it’s thought-about unlisted for the aim of taxes in India.

The interval of holding begins from the vesting date as much as the date of sale

The desk beneath exhibits the instance of Brief Time period Capital Acquire and Lengthy-term Capital Acquire

| On the time of | Items | Date | FMV of share(USD) | Tax to be paid | In earnings tax return |

| Grant | 240 | 12-Dec-13 | Not Relevant | nil | Not Relevant |

| Vesting | 70 Vested

49 transferred |

12-Dec-14 | 17.89

1 USD = 62.90 Rs CII of yr 240 |

Tax of 30% taken by promoting 21 shares

Revenue Tax = 70 * 17.89* 62.90=78770 |

Perquiste Revenue as Revenue from Wage.

Taxed as per worker’s Revenue Tax Slab Fee |

| Sale of shares if unlisted | 20 | 31-Jul-15 | 20.96

1 USD = 63.60 Rs |

Brief Time period Capital Acquire= 20* ((63.60*20.96)-(62.90* 17.89))= Rs 4,155.5 | Underneath Capital Positive aspects (brief time period capital positive factors)

Taxed as per Revenue Tax slab of worker |

| Sale of shares if unlisted | 25 | 31-Jan-17 | 25.89

1USD = 67.15 CII of the yr 264 |

Listed bought price = 62.90 * 264/240 = 69.19

Lengthy-Time period Capital Acquire with indexation= 25*((67.15 * 25.890)-(69.19* 17.89)) = =25* (1738.5135 -1237.8091) = 25*500.7044=12517.61 Lengthy-Time period Capital Acquire tax(with indexation) = 20% of 12517.61=2503.522 |

Underneath Capital Positive aspects (long run capital positive factors)

Lengthy-Time period Capital Acquire with out indexation= 25*((67.15 * 25.890)-(62.90* 17.89)) = 15330.8125 Lengthy-Time period Capital Acquire tax(with out indexation) = 20% of 15,330.8125=3066.1625 |

Capital Loss

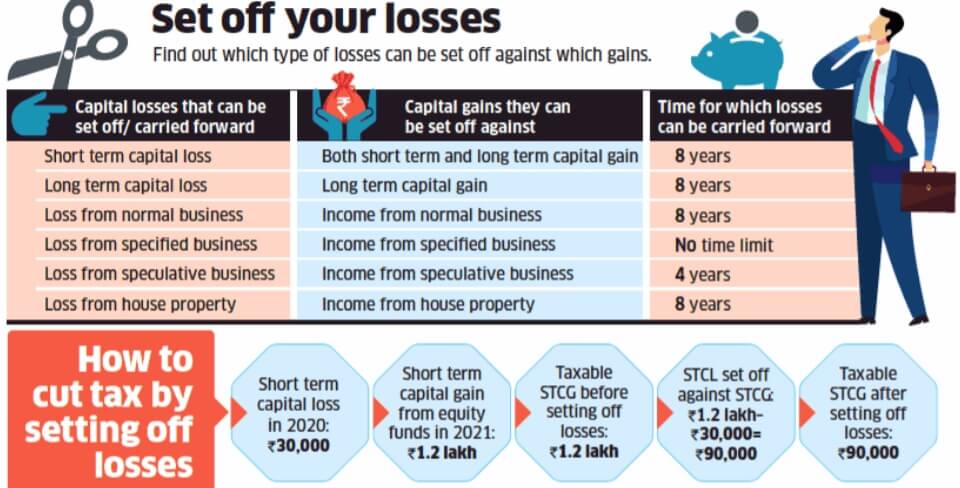

What if there may be loss on promoting shares? Fortunately Revenue Tax Division provides advantage of Setting of Capital Loss.

Set-Off Losses means adjusting the loss in opposition to the taxable earnings earned; after that, remaining the loss may be carried ahead to future years.

The taxpayer can’t carry ahead losses to future years if the earnings tax return for the yr wherein loss is incurred will not be filed on the Revenue Tax Web site inside the due date as per Sec 139(1).

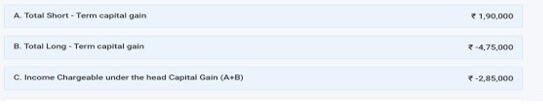

If one has Brief time period capital loss, then it may be set off in opposition to short-term or long-term capital achieve from any capital asset(actual property, gold, debt mutual funds).

If the loss will not be set off totally, then it may be carried ahead for a interval of 8 years and adjusted in opposition to any short-term or long-term capital positive factors made throughout these 8 years. However provided that he has filed his earnings tax return inside the due date.

The best way to set off capital loss

Displaying Capital Positive aspects in ITR

Half A of the Capital Positive aspects Schedule gives for computation of brief‐time period capital positive factors (STCG) from the sale of several types of capital property. Out of this, merchandise No. A3 and A4 are relevant just for non‐residents.

Half B of this Capital Positive aspects Schedule gives for the computation of lengthy‐time period capital positive factors (LTCG) from the sale of several types of capital property. Out of this, merchandise No. B5, B6, B7, and B8 are relevant just for non‐residents

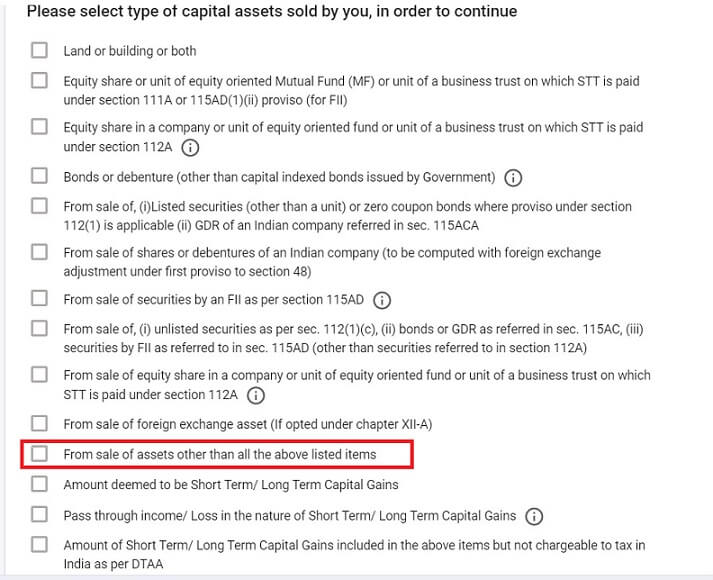

Select the Schedule Capital Positive aspects

In Capital Acquire Schedule on the market of shares of MNC not listed on Indian Inventory Alternate select Sale of Property apart from listed. (along with some other capital achieve you’d have)

Selecting the part in Capital Positive aspects for Overseas Shares

Then Select Brief Time period Acquire/Lengthy Time period Acquire

- Brief Time period Acquire for those who held shares for lower than 24 months

- Lengthy Time period Acquire for those who held shares for greater than 24 months

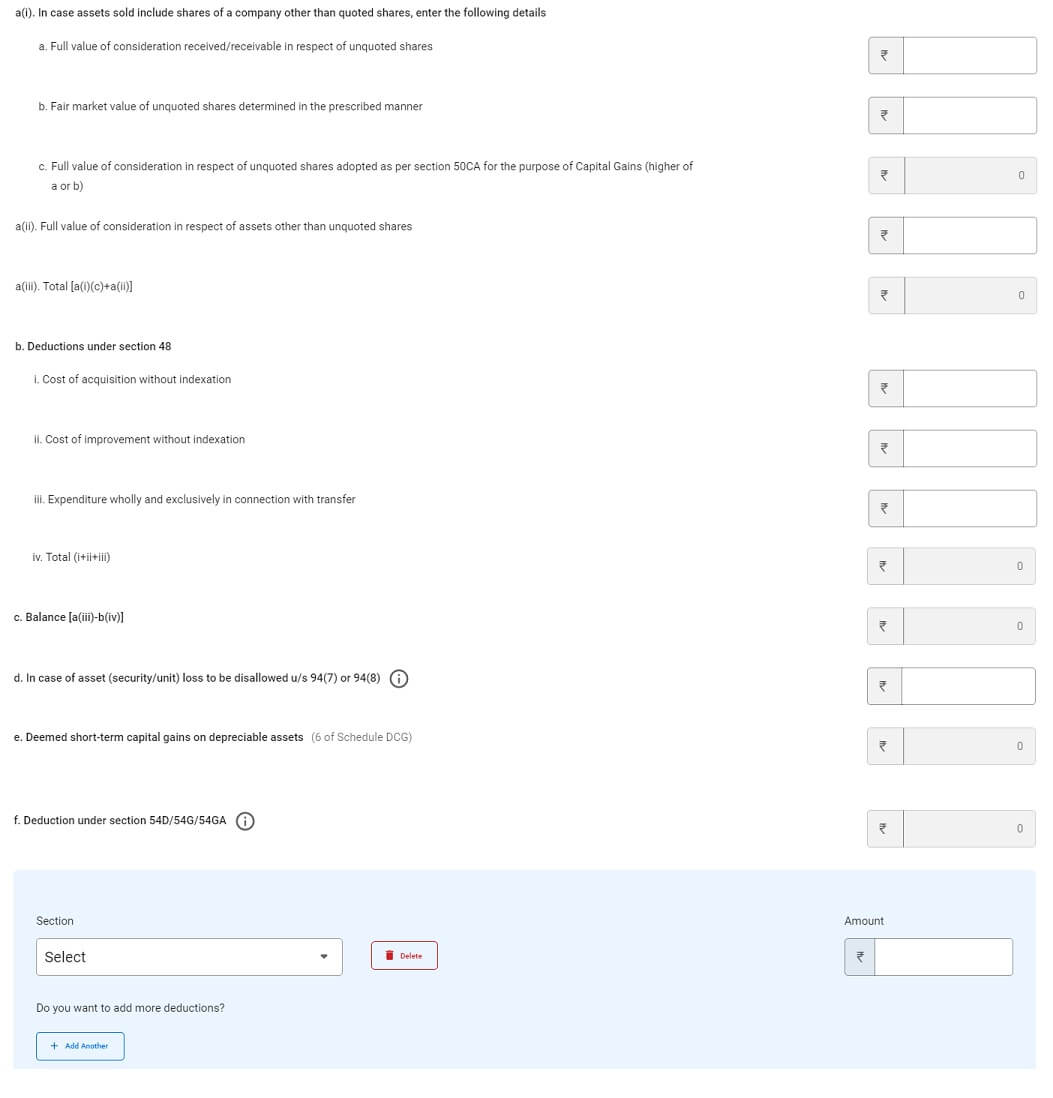

The brand new ITR Utility exhibits the main points that have to be stuffed for Capital Positive aspects

Present capital achieve on sale of Overseas shares in New ITR

Capital Positive aspects in Outdated ITR

Long run capital Acquire in ITR for RSU with indexation

Setting of the Capital Loss

When you’ve got a capital loss then in abstract you’d see the loss an instance of which is proven within the picture beneath. If there’s a Capital Loss, it will be mirrored as a detrimental worth

Capital Loss in ITR

Click on on Schedule CYLA (Present 12 months Losses Changes). The small print entered in Capital Acquire Schedules will replicate in Set-Off/ Carry Ahead Schedules.

Observe: Set off & carry Ahead Schedules will fetch knowledge from Capital achieve Schedule. The taxpayer needn’t enter the main points once more in these schedules.

Click on on Schedule CFL (Carry Ahead Losses)

The unadjusted losses of that monetary yr shall be carried ahead.

Within the following years ITR you possibly can alter your capital positive factors in opposition to this loss and cut back your tax legal responsibility.

DTAA and RSU

Double taxation refers back to the scenario when a person is taxed greater than as soon as on the identical earnings, asset or monetary transaction.The Double Tax Avoidance Agreements (DTAA) is bilateral agreements entered into between two international locations, in our case, between India and one other overseas state. The fundamental goal is to keep away from, taxation of earnings in each the international locations (i.e. Double taxation of identical earnings) and to advertise and foster financial commerce and funding between the 2 international locations.

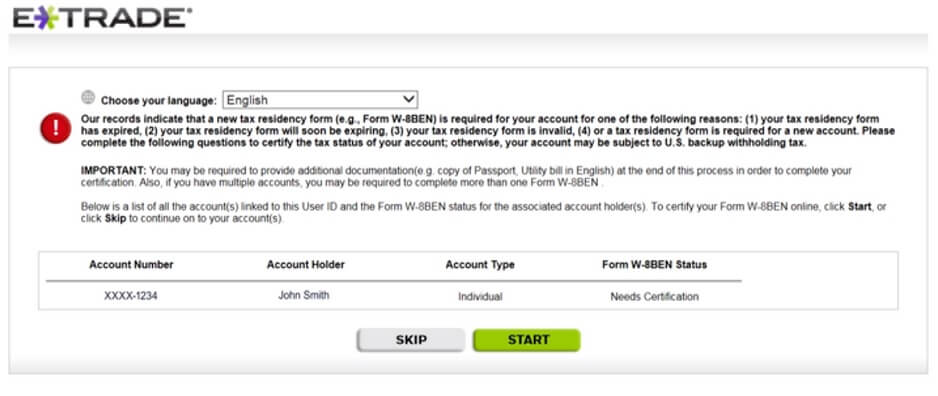

US MNCs with workers in India typically submit W-8BEN to US brokers to keep away from any withholding associated to US taxes. Nonetheless, the taxes and so forth are deducted for the workers in India. These are reported in perquisites kind. (as defined above). The picture beneath exhibits how one has to certify W-8BEN kind on ETrade for US. Extra particulars within the video right here.

If any tax is deducted in US then US IRS division will ship Kind much like Kind 16 to your handle.

ETrade W8Ben Certification

Advance Tax on Capital Acquire of RSU

Advance Tax guidelines require that one’s tax dues (estimated for the entire yr) should be paid prematurely. Advance tax is paid in installments. Whereas the employer deducts TDS when your RSUs get vested, one could should deposit advance tax if one earns capital positive factors.

Non-payment or delayed cost of advance tax ends in penal curiosity beneath sections 234B and 234C.

That you must pay Advance Tax on RSUs solely while you promote the RSUs and the revenue is greater than 10,000 Rs. That you must pay an acceptable share of it earlier than the closest due date. So for those who offered between 16 June and 15 Sep it is advisable pay 45% earlier than 15 Sep.

| Due Date | Advance Tax Payable |

|---|---|

| On or earlier than fifteenth June | 15% of advance tax much less advance tax already paid |

| On or earlier than fifteenth September | 45% of advance tax much less advance tax already paid |

| On or earlier than fifteenth December | 75% of advance tax much less advance tax already paid |

| On or earlier than fifteenth March | 100% of advance tax much less advance tax already paid |

Nonetheless, it could be onerous to estimate tax on capital positive factors and deposit advance tax within the first few installments if a sale occurred later within the yr. Subsequently when advance tax installments are being paid, no penal curiosity is charged the place installment is brief resulting from capital positive factors. Remaining installment (after the sale of shares) of advance tax at any time when due should embody the tax on capital positive factors.

Relying on the time period between the vesting date and the sale date, the revenue can both qualify for short-term or long-term capital positive factors tax. For RSUs, the acquisition date is the vesting date.

Our article Advance Tax:Particulars-What, How, Why is about Advance Tax for people.

Disclaimer: This data is for academic functions solely. We’ve tried to supply the knowledge to the very best of our means. However please seek the advice of your CA, tax guide. Bemoneyaware.com will not be liable for any legal responsibility on data offered on the location.

Associated Articles:

- Wage, Internet Wage, Gross Wage, Value to Firm: What’s the distinction

- Wage, Allowances, Dearness Allowance, Authorities Wage, Pay Fee

- Understanding Variable Pay

- Understanding Kind 16: Half I

- How To Fill Wage Particulars in ITR2, ITR1

- HRA Exemption, Calculation, Tax, and Revenue Tax Return

- How are Dividends of Worldwide or Overseas Shares taxed? The best way to present in ITR

Hope this text helped in understanding What are RSUs? Why are RSUs given? What’s the vesting date? When are RSU taxed? Is there a capital achieve on promoting RSU? What’s the capital achieve from promoting RSU? The best way to present these in ITR