As I anticipated (and doubtless many others too), mortgage charges moved larger after the Fed price reduce this afternoon.

Everybody knew the Fed was going to chop its personal federal funds price by 25 foundation factors (bps), so it wasn’t a shock in anyway.

And given how a lot mortgage charges had fallen going into this extensively anticipated information, a bit of bounce larger appeared like it might most likely make sense.

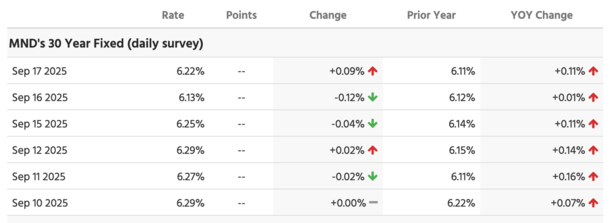

For the report, mortgage charges didn’t surge larger immediately, however they principally erased a lot of the massive good points seen a day earlier.

So all issues thought of, mortgage charges stay in actually fine condition.

It Occurred Once more. The Fed Minimize and Mortgage Charges Went Up

This isn’t the primary time this has occurred and positively gained’t be the final.

The #1 purpose why is as a result of (and sure I’m bored with repeating this) the Fed doesn’t set mortgage charges!

They set financial coverage through short-term charges to advertise most employment and steady costs. That’s it.

Nothing of their twin mandate has something to do with long-term rates of interest, not to mention shopper mortgage charges.

So no matter occurs to mortgage charges on the day of a Fed price reduce (or hike) is likely to be unrelated to the precise coverage choice.

Other than the choice, which everybody principally knew, there was the dot plot immediately (launched quarterly) that outlines the place the 19 Fed members see the FFR going by year-end and past.

That principally strengthened the thought of extra cuts to return in 2025, which even earlier than immediately regarded like two extra (one every in November and December).

That left the press convention, the place Jerome Powell fielded questions after ready remarks.

Lengthy story quick, Powell was Powell, that means he was very even-keeled and mentioned challenges stay.

“Within the close to time period, dangers to inflation are tilted to the upside and dangers to employment to the draw back—a difficult scenario,” he mentioned.

“With draw back dangers to employment having elevated, the stability of dangers has shifted. Accordingly, we judged it applicable at this assembly to take one other step towards a extra impartial coverage stance.”

Bond yields initially went down a bit on the dot plot however then jumped larger as Powell spoke.

Why? As a result of Powell is a staunch Federal Reserve Chair who isn’t going to present in to calls for to chop charges unnecessarily. Nor make any sudden or reckless strikes to suit anybody else’s agenda.

That’s why he added, “As is all the time the case, these particular person forecasts are topic to uncertainty, and they don’t seem to be a Committee plan or choice. Coverage is just not on a preset course.”

In different phrases, yeah, we would maintain reducing, however provided that the underlying knowledge helps it.

That’s maybe what despatched 10-year bond yields larger immediately. Or possibly they simply wanted a breather. And as I alluded yesterday, a bit of promote the information motion.

Mortgage Charges Already Fell a Ton Main As much as the Minimize

Now every part Powell mentioned immediately was principally a given. He didn’t waver and the financial knowledge the Fed depends upon was beforehand identified to all of us.

We already knew labor had worsened significantly over the previous few months, and that inflation continues to be a giant query mark.

However that labor is taking priority once more as a result of it’s starting to look actually ugly.

That’s precisely WHY mortgage charges fell a lot over the previous month. Keep in mind, the 30-year fastened was roughly 6.625% in mid-August.

It fell to about 6.125% yesterday (mortgage charges are supplied in eighths) earlier than bouncing a bit immediately, per MND.

Now it’s nearer to six.25%, which remains to be a reasonably good transfer decrease in such a brief period of time. It’s additionally so much farther from 7% than it was all yr.

If you happen to recall, it was round 7.25% in early January, so we’re a few full proportion level decrease now.

And if you happen to zoom out, mortgage charges are fairly near three-year lows.

So positive, mortgage charges bounced as anticipated, however not by a ton and within the grand scheme, look fairly good nonetheless.

By the best way, if you happen to’re evaluating this to final September, when mortgage charges jumped after the Fed reduce, that was principally associated to a scorching jobs report launched shortly after.

Right now, we’re coping with a sequence of ice-cold jobs experiences so the dynamic has shifted tremendously.

Most significantly, mortgage charges will proceed to maneuver decrease if the identical weak jobs knowledge we’ve been seeing currently continues to return down the pike.

Fed Price Cuts/Hikes Not often Match the Course of Mortgage Charges

September seventeenth, 2025: Price reduce, mortgage charges up

December 18th, 2024: Price reduce, mortgage charges up

November seventh, 2024: Price reduce, mortgage charges DOWN

September 18th, 2024: Price reduce, mortgage charges up

July twenty sixth, 2023: Price hike, mortgage charges down

Might third, 2023: Price hike, mortgage charges down

March twenty second, 2023: Price hike, mortgage charges down

February 1st, 2023: Price hike, mortgage charges down

December 14th, 2022: Price hike, mortgage charges down

November 2nd, 2022: Price hike, mortgage charges UP

September twenty first, 2022: Price hike, mortgage charges down

July twenty seventh, 2022: Price hike, mortgage charges down

June fifteenth, 2022: Price hike, mortgage charges down

Might 4th, 2022: Price hike, mortgage charges down

March sixteenth, 2022: Price hike, mortgage charges UP

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) dwelling patrons higher navigate the house mortgage course of. Comply with me on X for decent takes.