1. Mortgage charges will fall into the 5% vary

2. Residence costs will likely be flat (if not decrease)

3. Affordability will enhance however stay constrained

4. Residence gross sales will rise, however not as a lot as anticipated

5. The house builders will battle to maneuver stock

6. Extra debtors will flip to adjustable-rate mortgages

7. The most important mortgage lenders will achieve market share

8. Extra owners will faucet fairness to keep up existence

9. We’ll see quick gross sales make a return

10. The housing market gained’t crash

Bonus: We’ll see some type of new housing coverage rolled out by the Trump Administration.

2025 Was a Little Higher Than 2024

Welp, one other yr has come and gone, and whereas it wasn’t a lot completely different than 2024, issues have been a bit of brighter for the mortgage and actual property trade.

Should you recall, the saying in 2024 was “survive ‘til ’25.” There doesn’t appear to be an identical slogan for 2026 so maybe the worst is behind us.

Certain, some nonetheless assume we’re on the cusp of one other housing crash, however if you dig into the main points, all of the elements merely aren’t there.

As an alternative, likelihood is it’ll be a bit of extra of the identical in 2026, although with situations slowly returning to regular.

In fact, actual property is native so efficiency will all the time range by market.

Mortgage Charges Will Fall Into the 5% Vary

I all the time begin with mortgage charges as a result of that’s all the time essentially the most talked about subject.

My normal considering is mortgage charges will lastly dip into the 5s in 2026, possible by the primary quarter.

I get that there’s resistance at these ranges, however we’re additionally solely about 20 foundation factors away.

Finally, it’s going to solely take a nasty jobs report or two to get us there, assuming inflation continues to indicate indicators of enchancment.

The month-to-month financial savings won’t be big, however it could be sufficient to get extra price and time period refinances to pencil.

And it could be a psychological victory for potential dwelling patrons from a sentiment standpoint.

You’ll be able to see all of the 2026 mortgage price predictions within the related submit to see what others assume. The fast takeaway is generally flat.

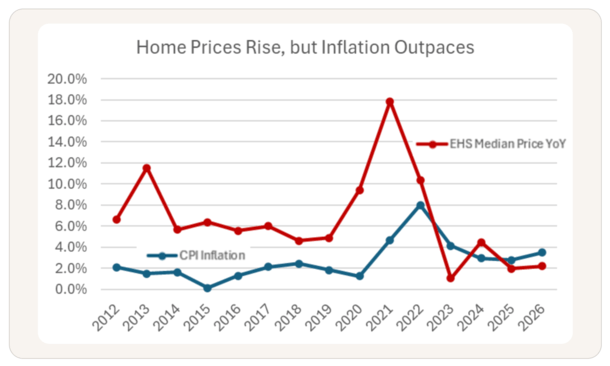

Residence Costs Will Be Flat (or Even Decrease)

Simply as most pundits anticipate flat mortgage charges in 2026, most anticipate dwelling costs to be comparatively unchanged as effectively.

The forecasts range considerably, however Zillow solely expects a 1.2% rise in property values subsequent yr.

And it’s an even decrease 0.5% improve from Compass chief economist Mike Simonsen.

Over at Realtor, they anticipate a 2.2% improve, which continues to be fairly flat, and never significantly better than the two.2% seen this yr.

Which means actual dwelling costs, adjusted for inflation, can be down, even when they’re up on a nominal foundation.

In some markets, such because the hard-hit Solar Belt, dwelling costs might really fall on a nominal foundation.

I don’t anticipate huge declines, however it’s definitely attainable to see damaging YoY adjustments given rising stock and poor affordability.

Affordability Will Enhance However Not Sufficient

Talking of housing affordability, the mix of decrease mortgage charges and flat (or decrease) dwelling costs will likely be a constructive for potential dwelling patrons.

The issue is it’s possible not going to be sufficient to actually transfer the dial. We’ve seen affordability slowly enhance this yr for these similar causes.

And it’ll possible proceed into 2026, however won’t be sufficient to get a borrower’s DTI ratio in vary. Or just entice them to leap off the fence.

On the similar time, it might not sway somebody to checklist their dwelling, realizing they’ll have to buy a alternative property.

We’ve had lots of would-be sellers dominate the market lately, and we even have would-be patrons too.

It’s a standoff that has slowly gotten higher, however continues to be fester as a result of not an entire lot has modified.

Residence Gross sales Will Rise, However Fall Wanting Expectations

I do consider dwelling gross sales will rise in 2026, however from very low ranges. Keep in mind, present dwelling gross sales have been at a near-30 yr low in 2024, simply above 4 million.

This yr they rose marginally and subsequent yr they’re anticipated to inch up additional, however stay near 4 million.

Fannie Mae pegs the present gross sales price at about 4.4 million, which is a good 7.5% enchancment, however effectively under what NAR expects.

Extra of the identical issues will plague the housing market in 2026, together with poor affordability, mortgage price lock-in, and restricted for-sale stock.

It may very well be loads worse, however it’s not going to be a bonanza, even with mortgage charges probably falling under 6%.

Particularly if the financial system takes a flip as shopper spending lastly catches as much as us, and job losses mount.

The Residence Builders Will Wrestle

The previous few years the house builders have been on a roll as a result of they have been form of the one recreation on the town.

No one was itemizing their properties, so that they had little competitors, regardless of poor dwelling purchaser demand.

As well as, they have been in a position to purchase down mortgage charges considerably utilizing a particular benefit often called a ahead dedication.

This meant mortgage price buydowns into the 2s and 3s (and even decrease), sufficient to entice skittish patrons to make the leap.

Nevertheless, they’ve seen their stock start to pile up as gross sales have slowed, with transactions anticipated to fall 1.6% this yr, per Fannie Mae.

They do anticipate a 4.5% uptick in new dwelling gross sales in 2026, however I’m not absolutely satisfied given the places of recent properties are in areas with a provide glut.

And even with huge gross sales concessions, the builders are struggling to maneuver properties.

The one caveat is that if they get some type of increase from a brand new coverage change, or some type of subsidy push.

Extra Debtors Will Depend on ARMs

Recently, there’s been a shift to adjustable-rate mortgages, which have come down with short-term charges just like the federal funds price.

With the expectation that the 30-year mounted might have peaked and may very well be flat, some are selecting an ARM to attain an excellent decrease cost.

It may possibly make sense if the rate of interest unfold is favorable, although it’s a must to watch out as a result of some lenders barely provide a reduction versus a 30-year mounted.

We’ve additionally seen the house builders flip to ARMs as a substitute of fixed-rate mortgages as a result of it’s cheaper for them to drive down the month-to-month cost for his or her clients.

Once more, perceive what you’re getting isn’t nearly as good as a 30-year mounted. Although immediately most ARMs are mounted for 5-7 years or longer, such because the 5/6 ARM and 7/6 ARM.

That’s lots of time to hope for even decrease charges sooner or later and within the meantime, pay much less and pay down the mortgage sooner (because of the decrease price).

The Greatest Mortgage Lenders Will Get Even Greater

The story of 2025 was mortgage lenders buying actual property firms and mortgage servicers, all in an effort to develop even bigger.

We noticed Rocket purchase each actual property brokerage Redfin and main mortgage servicer Mr. Cooper.

And the nation’s high lender, United Wholesale Mortgage, purchase Two Harbors, one other bigger mortgage servicer.

Then there was Decrease, which scooped up actual property portal Movoto and later partnering with actual property brokerage HomeSmart.

As well as, Compass acquired rival brokerage Wherever Actual Property and that might profit the popular lender Assured Fee.

I anticipate extra of those kinds of offers to occur in 2026 and for the closed ones to start to bear fruit.

This coincides with the brand new set off regulation rule, which requires lenders to have permission to succeed in out to debtors (or a previous relationship).

Guess who could have a previous relationship? Yep, the large guys who personal all these different firms and/or service the present loans.

That provides them extra recapture alternatives whereas concurrently shutting out their rivals.

That is good for the large guys, however might harm shoppers if there’s much less lender selection.

Extra Owners Will Faucet Their Fairness to Preserve Spending

We already noticed dwelling fairness lending rise fairly a bit the previous couple years, however it nonetheless pales compared to the early 2000s.

As well as, there are only a few cash-out refinances lately, so most fairness extraction is just coming by way of second mortgages like HELOCs and dwelling fairness loans.

As such, the numbers, whereas larger, aren’t all that loopy. I’ve mentioned for some time that if and when owners actually go nuts tapping fairness, we might run into issues once more.

Particularly if dwelling costs fall and/or if lenders get extra liberal with most CLTVs.

The issue lately is many householders have to faucet fairness simply to maintain up with their spending, which is a nasty signal for the broader financial system.

Whereas that sounds horrifying, lending requirements immediately are nonetheless manner higher than they have been within the early 2000s.

And as famous, most owners are conserving their low-rate, mounted first mortgages intact as a result of they’re so low-cost.

The Return of the Quick Sale

I’ve been listening to increasingly more rumblings of quick gross sales return to the housing market.

That is when property homeowners are underwater on their mortgages (owe greater than the property is price) however nonetheless have to promote.

They have been quite common throughout 2008-2013, however have been just about non-existent since then as dwelling costs surged and mortgage charges hit document lows.

However we’re now at a tipping level once more with dwelling costs falling in some markets, notably locations like Florida and Texas.

Those that took out 3%-down mortgages who’ve seen their property fall in worth may very well be in bother in the event that they NEED to promote.

That is particularly pertinent for the current vintages of dwelling patrons, assume late 2022 and 2023, when mortgage charges have been additionally excessive.

Little or no of the mortgage steadiness has been paid off and when mixed with a flat/decrease gross sales value and transaction prices, it may very well be quick sale territory.

To that finish, we’d additionally see an uptick in foreclosures as loss mitigation choices start to tighten up as effectively.

However once more, the excellent news is the overwhelming majority of householders both personal their properties free and clear, or have a mortgage price within the 2-4% vary.

The Housing Market Received’t Crash in 2026

One thing I’ve identified just a few occasions is that the majority of immediately’s mortgages have been originated when charges hit document lows.

This was in early 2021, and since then, dwelling costs have additionally surged larger. This implies your typical house owner has a brilliant low price, a small mortgage steadiness, and a low LTV ratio.

Sure, current dwelling patrons are within the precise reverse place, having purchased on the top of the market with 6-8% mortgage charges.

However right here’s an essential element. Residence gross sales fell off a cliff when affordability tanked, as we’ve seen with the transaction numbers hitting these 30-year lows.

Whereas it’s been arduous on the trade, whether or not it’s actual property brokers or mortgage officers and mortgage brokers seeing fewer transactions, it’s good for the market.

It’s a wholesome response for gross sales to sluggish if situations warrant it. Within the early 2000s, we compelled gross sales by with highly-questionable financing, which is usually what causes bubbles.

Due to the ATR/QM rule, we simply haven’t seen the identical stage of high-risk lending this cycle, even when FHA loans are a weak spot.

Like I mentioned, the housing market gained’t be freed from distressed gross sales in 2026, however it gained’t be something like GFC situations.

It’s really regular to have distressed gross sales and never an outright bull run yearly.

Will the Trump Admin Lastly Ship Housing Coverage Change?

One final bonus prediction. I consider the Trump admin will come by with some type of coverage change in 2026.

Granted, this isn’t a daring prediction as a result of Trump himself mentioned the opposite day that he would “announce a few of the most aggressive housing reform plans in American historical past.”

So he higher present up with one thing midway first rate. In fact, he pinned the blame of excessive dwelling costs on unlawful migration in that very same speech.

In the meantime, they actually went up due to document low mortgage charges mixed with low ranges of dwelling constructing post-GFC.

However given his admin has already floated all forms of wild concepts, such because the 50-year mortgage, transportable mortgage, and making extra mortgages assumable, which all fell flat, it’ll possible be one thing much less thrilling.

Maybe deregulation for dwelling builders to construct sooner and cheaper. In fact, new builds aren’t the be all, finish all answer, particularly since their stock is already piling up.

Anticipating the house builders to construct extra after they can’t even transfer present stock can be foolish.

Although if there have been some subsidies for patrons, it might probably assist. They simply must be aware of balancing provide and demand, and never simply making the market scorching once more.

Within the meantime, we’ll proceed to attend for the promise he made throughout his marketing campaign to deliver mortgage charges again down to three% and even decrease!

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) dwelling patrons higher navigate the house mortgage course of. Observe me on X for decent takes.