Nobody has requested for it, however right here it’s, the following episode of my Personal Fairness sequence. Earlier episodes of the Personal Fairness sequence could be discovered right here:

Personal Fairness Mini Sequence (1): My IRR isn’t your Efficiency

Personal Fairness Mini sequence (2) – What sort of “Alpha” are you able to anticipate from Personal Fairness as a Retail Investor in comparison with public shares ?

Personal Fairness Mini Sequence (3): Listed Personal Asset Managers (KKR, Apollo & Co)

Personal Fairness Mini sequence (4) : “Investing like a “billionaire” for retail traders within the UK inventory market through PE Trusts

Personal Fairness Mini Sequence (5): Commerce Republic provides Personal Fairness for the plenty (ELTIFs) -“Good attempt, however hell no”

Personal Fairness (Mini) Sequence 6: Personal Fairness for the plenty – Y2K version

Personal Fairness Sequence (7): Secondaries – The Magic Cash Machine for the PE trade

Background:

Everybody within the various (non-listed) funding area has been speaking concerning the Blue Owl Personal Debt “redemption gating” occasion these days, however in my private opinion, one other story which has not been so broadly reported is rather more attention-grabbing.

The case of the primary Stonepeak Infrastructure Flagship fund is at the very least equally attention-grabbing for the entire Personal Fairness sector and I’ll attempt to clarify why.

Historically, the Personal Fairness enterprise mannequin could be summarized from the the angle of the Asset Supervisor or Normal Associate (“GP”) as follows:

GPs take an enormous junk out of any upside (normally 20% ,typically extra) however themselves have little or no draw back danger as they cost a hefty 2% p.a. charge in any case and solely, if in any respect, make investments comparatively little cash themselves into the funds they handle.

So let’s take a look at Stonepeak. Stonepeak is among the main Various Infrastructure Fairness Asset Managers on this planet and has 89 bn USD Property underneath Administration. It’s nonetheless privately owned.

Infrastructure was really one of many few vibrant spots within the Personal Fairness area prior to now few years, the place fundraising nonetheless works, in distinction to the “regular” non-public Fairness funds.

Though the dividing line between Infrastructure and Personal Fairness is somewhat bit blurry, Infrastructure investments are sometimes “capital heavy” and regarded extra secure regardless of normally important leverage. Typical property are ports, Airports, railways, toll roads but in addition stuff like container leasing, warehouses and many others. (amongst others Stonepeak purchased the Canadian Port Operator Logistec which I owned)

Goal returns for Infrastructure funds are normally a bit decrease than for Personal Fairness (normally perhaps 10-15% p.a. vs. 15-20%) and fund period is commonly a bit longer. However infrastructure must be even be extra sturdy, i.e. have much less draw back than a PE fund.

Stonepeak was based in 2011 and launched its inaugural “Flagship” fund in 2012.

Now comes the attention-grabbing half:

Just a few weeks in the past, the founding father of Stonepeak, Mr. Dorrell, pledged private assist for the moderately badly performing preliminary flagship fund.

Though it isn’t uncommon that Various Assetmanagers would possibly perhaps scale back charges going ahead if a fund performs actually badly, that is the primary time that I’ve really seen that an proprietor really places in private cash to make good on the not so nice efficiency of the traders. Right here is the way it ought to work:

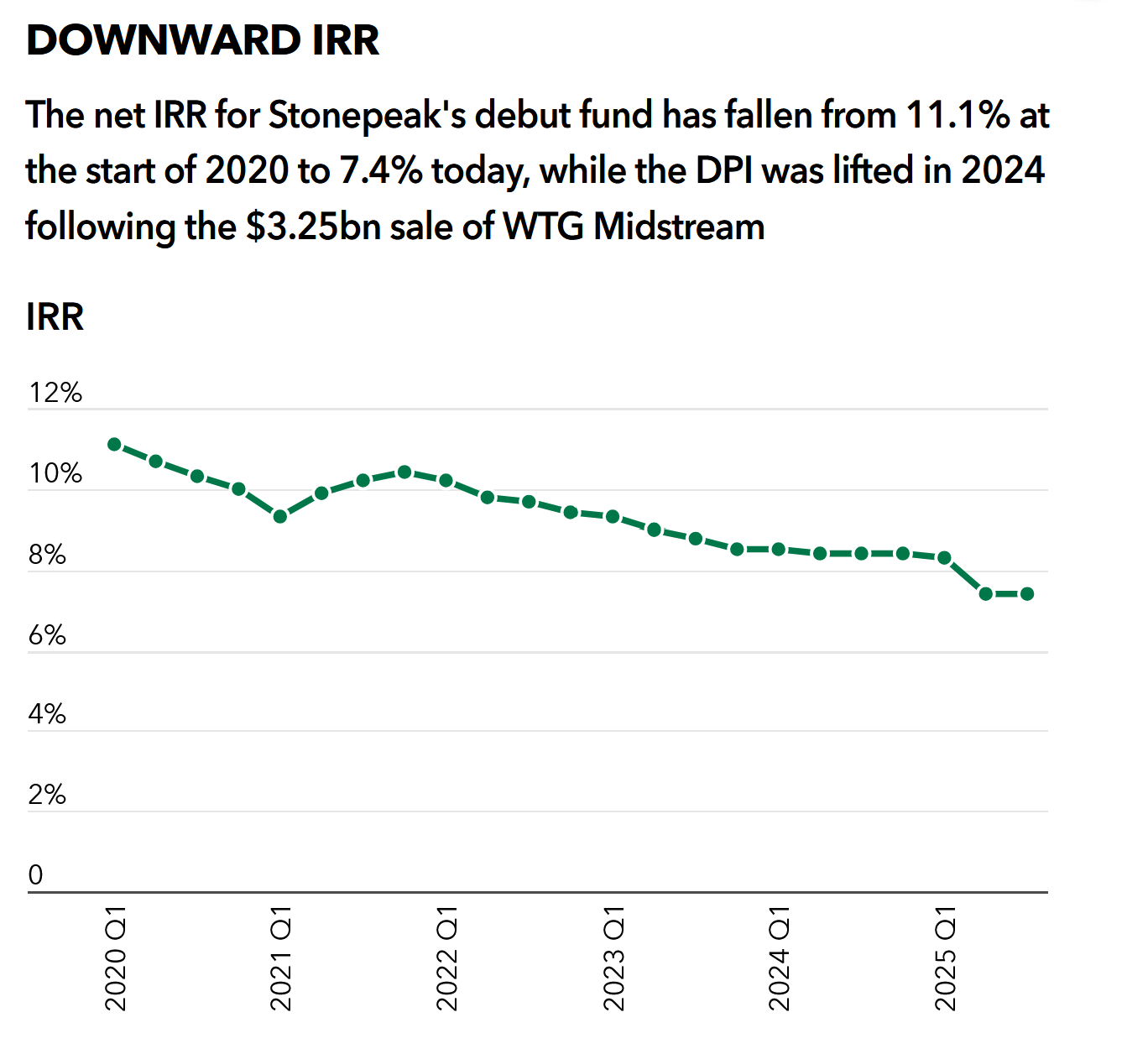

In response to the article, the preliminary fund had “promised” 12% internet IRR to traders at launch however at present, after 14 years it solely reveals an IRR of seven,4%. Not a catastrophy at first look but in addition not nice both for such a classic that ought to have benefitted from a big decline in rates of interest which was particularly useful for “lengthy period” infrastructure property.

What can also be actually attention-grabbing is that graph that reveals how calculated IRRs have developed within the final years from the angle of traders on this fund:

Till 2020, i.e. for the primary 7-8 years every thing regarded tremendous. However what occurred then ? And why is that this related ?

I assume it’s now time to let you know somewhat bit a few “soiled secret” of the Personal Fairness (and Personal Infrastructure) world.

Every time a brand new agency will get created and launches an preliminary fund, it takes a very long time till traders can see precise outcomes. On common, within the infrastructure area, funding are bought perhaps 6-10 years after they’ve been purchased.

Nevertheless, Asset Managers don’t need to wait till then to lift a brand new fund. They need to elevate funds extra regularly with the intention to earn extra charges. Usually the “fund elevating” cycle is ~ 3-4 years.

Even skilled traders make investments largely based mostly on previous efficiency, typically simply merely extrapolating these previous numbers sooner or later.

So what do you do when you don’t have any exits to indicate ? After all, you simply mark up your portfolio your self based mostly on some loosely outlined metrics which frequently is coincidently very near the goal return. So simply to say this once more: To start with, nearly all PE/Infrastructure funds are marking up their investments “at will” to indicate a good efficiency, in fact with the hope that afterward, they are going to really notice these returns or much more.

You then can current this (unrealized) return to traders and so they fortunately make investments into the following fund and the following and many others.

In Stone Peak’s case they had been fairly busy and raised one other 3 funds throughout the time when efficiency was wanting nonetheless OK for the initital fund in 2020 as we are able to see right here:

The funds obtained greater and greater, Fund III was ~7 bn and Fund IV 14 bn. And they’re at present elevating fund V with a goal dimension of 15 bn,

Most of that cash obtained raised with traders wanting on the monitor document and saying: Fund I seems good at 11% p.a. (or perhaps much more to start with) and I assume Stonepeak was telling them that this was marked “conservatively” (GPs at all times say that about unrealized values).

Nevertheless it turned out to be mistaken and clearly overvalued. And that is clearly embarrassing for Stonepeak.

If I had been a possible Stonepeak investor doing Due Dilligence, I’d ask: “How can I belief all the opposite efficiency numbers of your funds when the one one which is sort of realised appears to have been considerably overvalued ?”

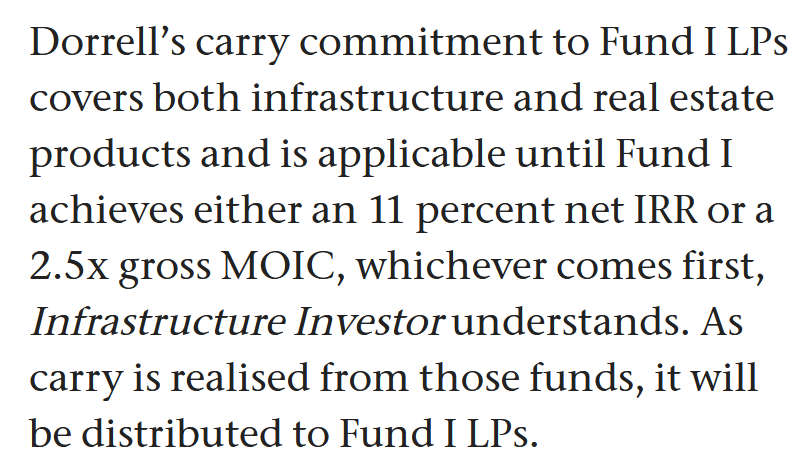

I assume that’s why Dorrell desires to make these traders “entire” with private cash:

As the primary fund is considerably smaller than the observe up funds, this is not going to bankrupt him, however anyway, this is an trade first.

The trade relevance in my view is the next:

We will anticipate much more such instances the place the preliminary, very optimistic efficiency will prove not so optimistic in any respect and even funds might lose cash (2019 to 2021 vintages as an illustration).

Up to now, this has at all times been the only downside of the investor, by no means for the GP.

Michael Dorrell now created a excessive profile precedent that will probably be taken up with gusto by many disillusioned traders.

The sensible LPs will use the Stonepeak precedent to ask their GPs for a similar “Dedication” to make good on their preliminary promise.

In any other case they won’t make investments right into a subsequent fund. Some GPs, particularly the very massive ones will resist, some will perhaps simply shut up store, however I assume quite a lot of GPs will get underneath quite a lot of stress.

Total, this could be a primary step to alter the connection between GPs and LPs going ahead. If you’re an investor in any listed Various Asset supervisor, I believe it is best to actually take note of this. It may very well be that sooner or later, outcomes would possibly get much more unstable and basically decrease if funds underperform.

One other related level is the next:

This case additionally places a highlight on how arbitrary particularly early valuations are for these investments. Already final 12 months, I heard rumors that auditors have begun to problem valuations of PE funds as they see secondary transactions with giant reductions.

I might additionally think about that traders need higher disclosure of unrealized return figures throughout Due Diligence and the way these seemingly nice early efficiency numbers obtained cooked up, or perhaps not 😉

In any case, I’m positive that there willl be quite a lot of attention-grabbing discussions already occurring between disillusioned traders and GPs, that’s for positive.

Timing sensible, this comes at a fairly inconvenient time for many PE corporations anyway. As this chart reveals, the final 12 months was not so good for the share value efficiency of the massive outlets:

Possibly we are going to see a turn-around in some unspecified time in the future sooner or later, however for the second I see extra headwinds than tailwinds for the trade total. If extra GPs are compelled to compensate traders, then valuations for these guys would want to return down considerably.