Innoscripta

Innoscripta, an organization at which I appeared a number of days in the past, had a number of information objects over the previous few days.

First, they introduced that they plan to pay a 4 EUR dividend for 2025 in 2026. At a present share worth of ~70 EUR, that’s a dividend yield of 5,7% which is kind of substantial.

Then they lastly give you a steering for 2026 which appears as follows:

Munich, 25. February 2026 – innoscripta SE (ISIN: DE000A40QVM8, the “Firm”) expects a rise in income and earnings for the 2026 monetary yr based mostly on present enterprise growth and continued excessive demand.

The Firm’s Administration Board at present expects the next for the 2026 monetary yr:

- consolidated income of not less than EUR 140 million and

- EBIT of not less than EUR 80 million

The steering relies on the present order state of affairs, the scalability of the enterprise mannequin, and secure regulatory circumstances.

This steering represents an anticipated +36% gross sales development for 2026 (vs. + 60% in 2025) and +27% EBIT development (vs. +70% in 2025). The implied 2026 EBIT margin is 57% in opposition to 61%.

General, regardless of the decelerate in development charges, these are nonetheless very spectacular numbers. The inventory trades at present at round 14x 2026 P/E. Nonetheless, buyers don’t appear to be satisfied that this can be a good funding.

Perhaps the “AI concern” is the motive force right here. To be sincere, I discover it very troublesome for now, to get the conviction to take a position into the at present very damaging share worth momentum, however I’ll hold watching and hopefully have the ability to attend the AGM in Munich in particular person.

Nomad Meals

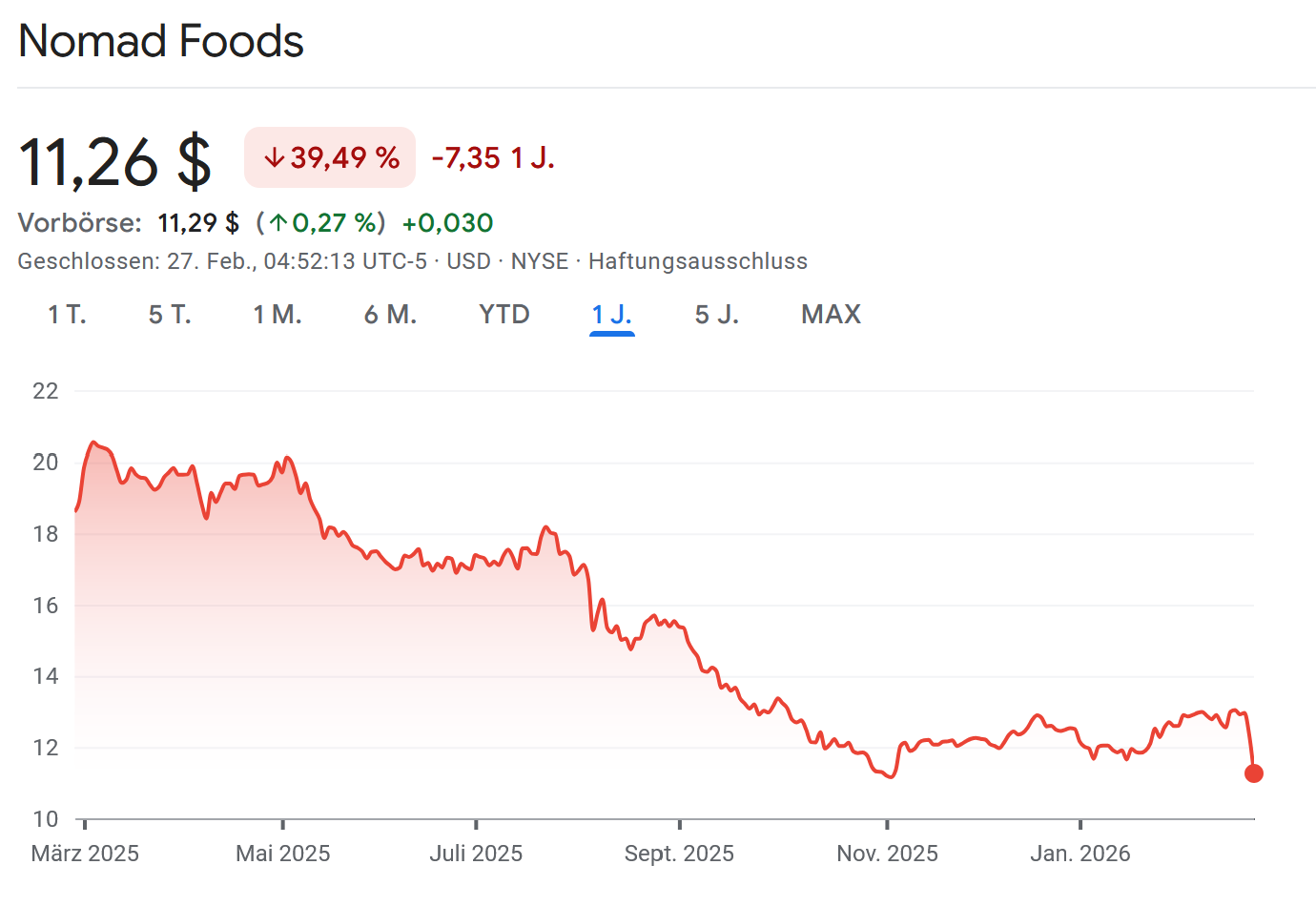

Nomad Meals is the frozen meals competitor of Frosta that I discussed within the Frosta write-up. Nomad launched 2025 numbers yesterday.

The image was not fairly in any respect. Gross sales down, margins down, earnings down. Unadjusted they really made a GAAP loss in This fall.

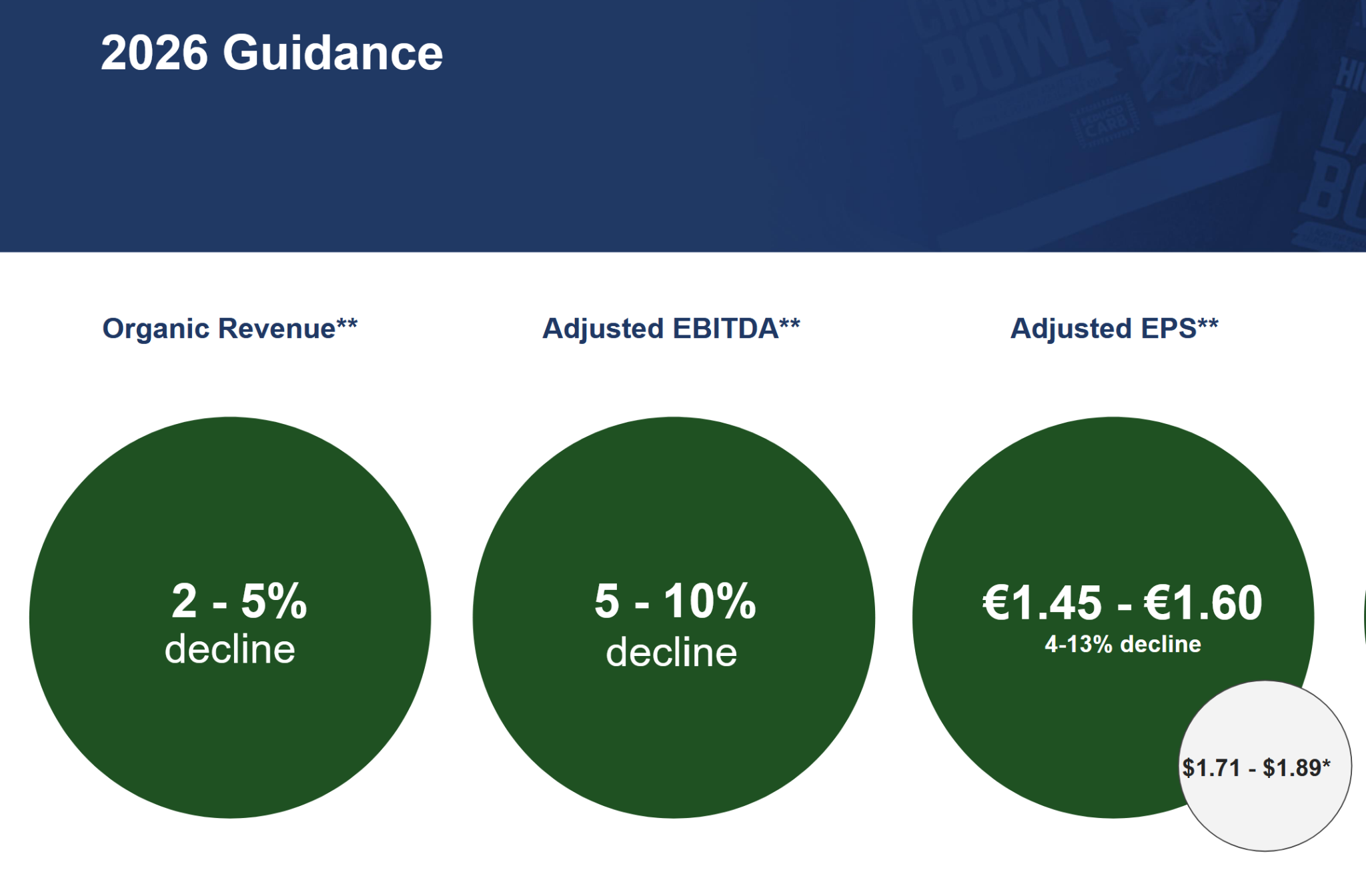

The steering for 2026 doesn’t look a lot better both, however slightly worse:

If we evaluate this to Frosta who’ve elevated gross sales double digits, improved gross margins and solely have proven decrease internet margins due to greater promoting spend, it’s fairly clear that Nomad Meals and particularly the Iglo model appears to be shedding market share.

My intestine feeling is that in Nomad’s case, the deal with Money technology and share purchase backs has perhaps led to underinvestment into the model which isn’t really easy and fast to reverse. Just about the identical “playbook” and points like Kraft-Heinz or Anheuser-Busch.

Within the shopper area, the safer long run bets are these guys who make investments long run into the model and never the spreadsheet jockeys.

With an additional EBITDA decline and present Debt/EBITDA of three,8x, I’m not positive for the way lengthy they will proceed to pay dividends and purchase again shares.

This one appears actually weak. For Frosta, there may very well be a msall danger that if Nomad will get actually determined and wishes money, that they begin to dump their merchandise into the market. So I feel it is smart to have a look at Nomad updates as a Frosta shareholder in any case.