Administration abstract:

On this publish I attempt to discover if Paypal is struggling solely from momentary points or if they’ve structural issues. My take away from a somewhat brief evaluation is that the issues are certainly structural and subsequently the inventory will not be of curiosity to me in the intervening time.

Introduction

Paypal is a type of shares that’s each very current on my “”TwiX” timeline in addition to has been talked about in a few current discussions with buyers that I worth extremely.

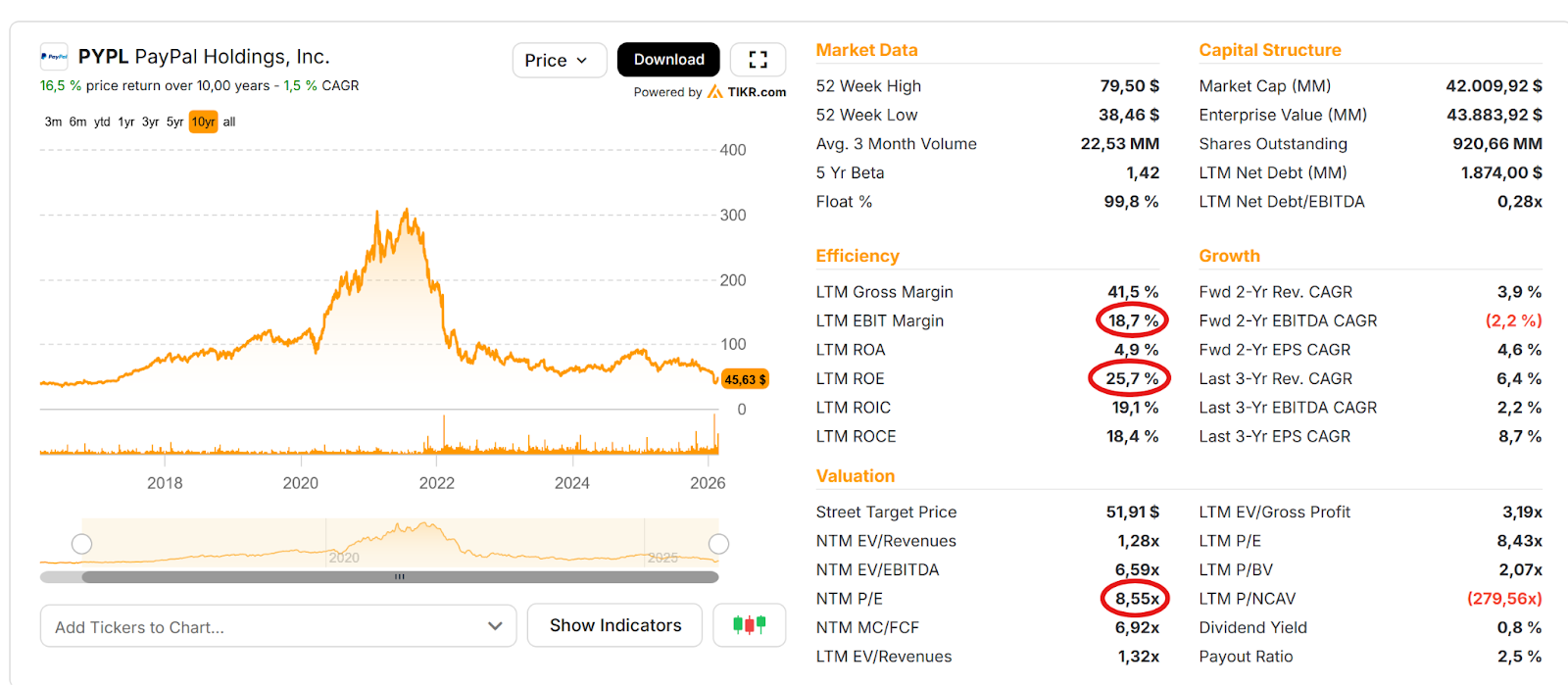

At first sight it appears like an honest “Worth” inventory. Single digit P/E, giant share purchase backs, excessive free money circulate, good margins, first rate ROE, a whole bunch of tens of millions of purchasers and so forth. So what’s to not like ? Right here is the TIKR overview:

Paypal can also be a type of shares the place everybody has an opinion as nearly everybody has a Paypal account or is utilizing different fee companies steadily So at first sight, it appears like a simple to know enterprise which could decrease their “barrier to entry” even for extra inexperienced buyers

Personally I’ve to confess that I discover the fee area tremendous complicated and never simple to know.

What downside does Paypal clear up ?

Paypal’s important enterprise is to permit retail clients to pay on-line for E-commerce actions and/or ship cash from one consumer to a different inside the Paypal community or through their extra P2P service Venmo.

Paypal has develop into profitable as a result of for shoppers it used to offer a really handy approach with out a whole lot of friction as in comparison with typing in your bank card particulars each time you utilize a brand new on-line service provider as an example. Paypal was additionally one of many first extensively accessible companies to ship P2P cash. You simply have to know the E mail deal with of the recipient.

Paypal describes itself as a “2-sided market place” connecting retail purchasers with E-commerce retailers.

For retailers, this was initially additionally very enticing as Paypal eliminated friction and elevated the likelihood {that a} buyer would really finalize the acquisition.

What Issues does Paypal have ?

When a extensively identified inventory comparable to Paypal appears clearly low-cost, my first thought is all the time the next:

What apparent issues does that firm have and do I’ve a “variant perspective” ?

Particularly for bigger US shares, assuming that everybody else is simply silly and you’re the just one who can determine a single digit P/E ratio is naive to say it in a pleasant approach.

For me, momentary issues could be an invite to dig deeper, whereas structural issues are a lot tougher to handicap.

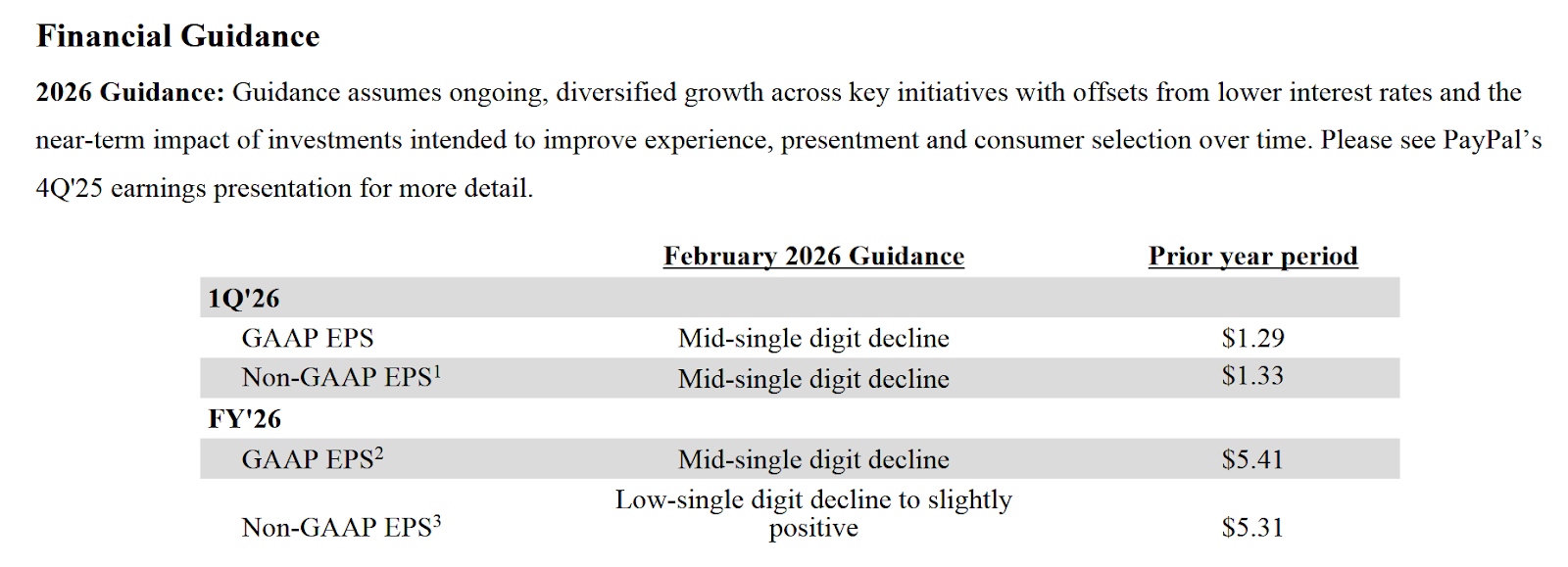

Paypal has some apparent points, considered one of them being having a brand new CEO with little expertise within the precise enterprise and having guided to decrease gross sales and earnings in 2026

The brand new CEO since March 1st, Enrique Lores, is a very long time HP Govt, who, based on Linkedin, has no direct fee or monetary companies expertise.

Lores has some robust incentives immediately linked to the share value. He’ll obtain the utmost quantity if the share value hits 125 USD till 2029. His most compensation could be ~125 mn USD. This seems like a big sum, however for Lorres, an long run HP govt, even that may not be life altering. He appeared to have earned round 19 mn USD and his internet price is estimated to be no less than 50 mn USD. So he’s wealthy already.

The larger downside is clearly that the 2026 outlook appeared very bleak. Particularly in comparison with competitor Adyen which guided to twenty% income progress in 2026 and past and to not communicate of Stripe which has grown gross transaction quantity by +34% in 2025.

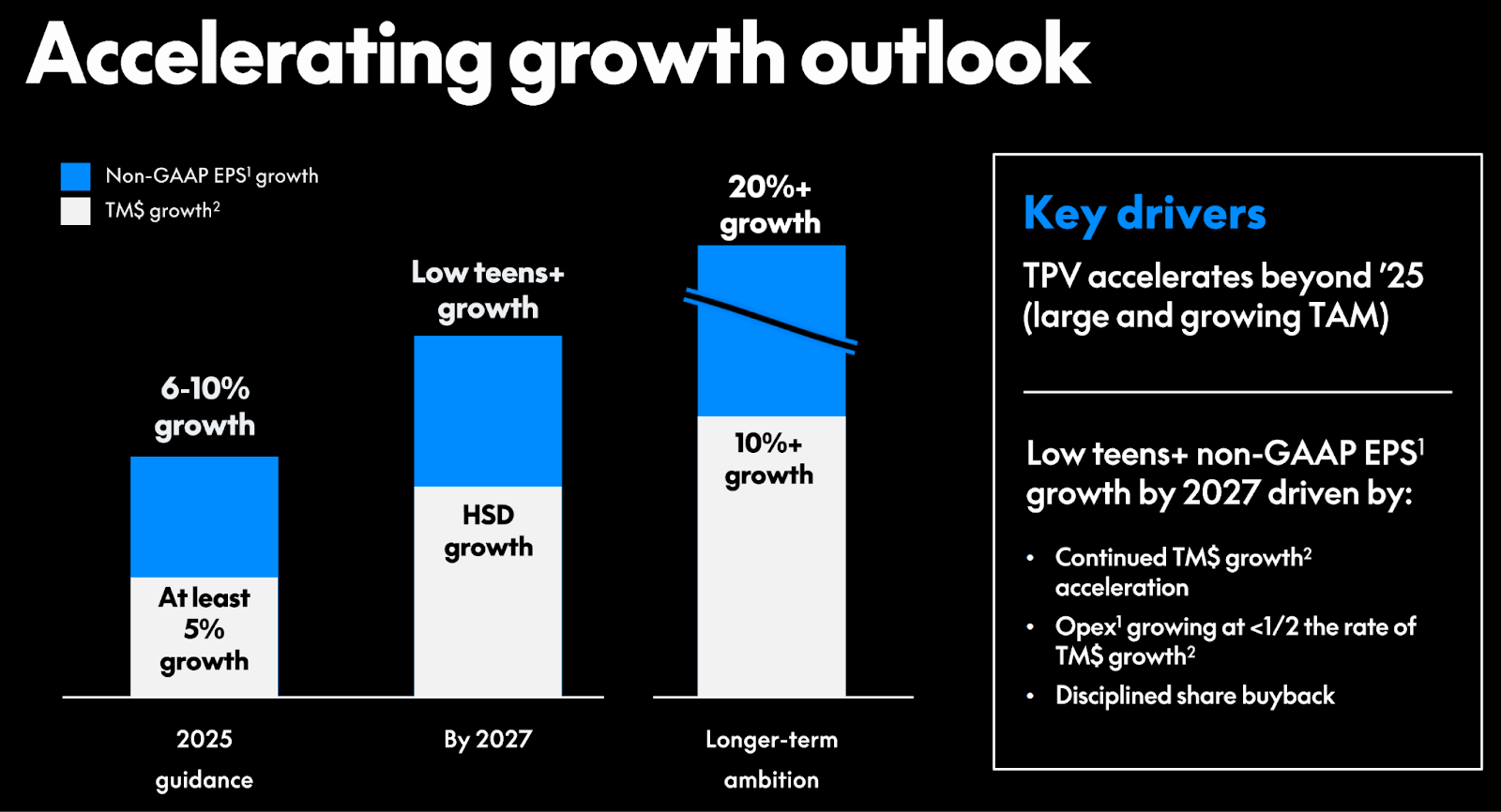

It’s particularly attention-grabbing to have a look at the 2025 investor day presentation. Again then, the previous CEO Alex Chriss, who had no less than some monetary companies background from Intuit really made a fairly convincing pitch positioning Paypal as a “commerce platform”. This was their ambition again then:

After shrinking in 2023, Paypal delivered some progress in 2024 and likewise some progress in 2025 however as talked about above, subsequent yr appears like shrinking once more.

2025 outcomes looke d“okayish” however on a quarterly foundation, progress decelerated every quarter which most definitely led to the dismissal of the previous CEO-.

One of many main points appears to be that Paypal runs no less than 6 totally different platforms inside Paypal based on this slide:

In response to this slide, one consumer may need 4 totally different IDs throughout the Paypal companies which aren’t linked up to now:

Technical debt: Separate & outdated technical infrastructure vs, opponents on the service provider facet

The chart factors to one of many important weaknesses of Paypal: Paypal might be thought-about already a legacy participant within the funds area. They’ve created separate platforms for separate use instances that are actually simply very tough and costly to deal with.

The newer opponents from the service provider facet like Stripe or Adyen all have one platform that runs all of their actions which makes it loads simpler to react and enhance upon.

What can also be attention-grabbing is that Paypal employs greater than twice the staff of Stripe and Adyen mixed. This can be a desk that Gemini compiled for me.

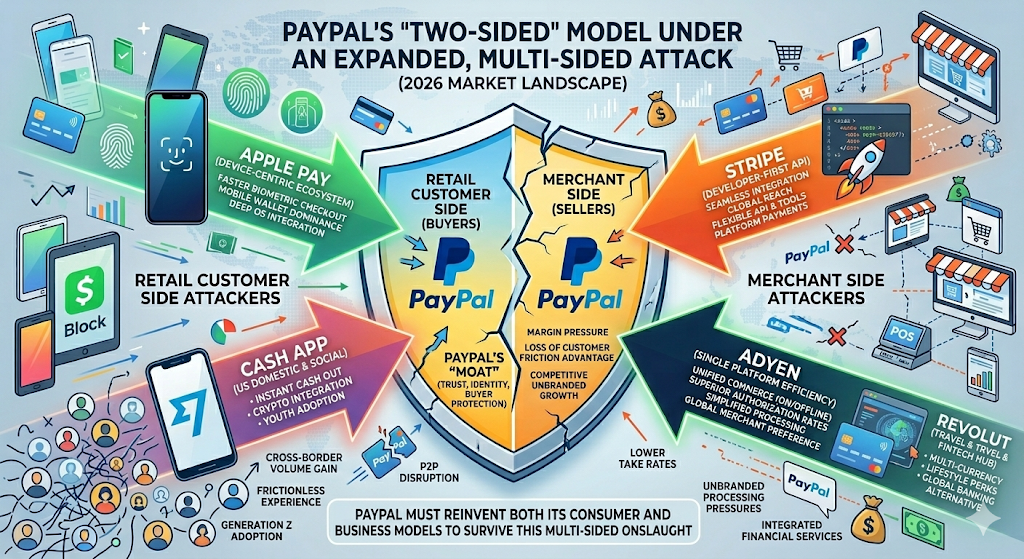

Further assaults on the retail consumer facet: Google Pay & Apple Pay, Revolout, Sensible, Money App and so forth.

As a “2 sided market palace”, Paypal sadly can also be topic to huge disruption on the retail buyer facet.

In case you are a cellular consumer, the likelihood is excessive that if you buy one thing offline or on-line it’s most definitely down immediately through your cellphone. You both maintain your cellphone to a POS terminal in a bodily store otherwise you affirm the acquisition with a finger print or face scan of your cellphone which is much more handy thant the Paypal Test-out.

At P2P degree, each Paypal companies are topic to a whole lot of opponents, comparable to Block’s Money app, Revolut’s free transfers or Sensible’s worldwide transfers.

So merely mentioned: there is no such thing as a place to cover for Papyal.

Paypal is the most costly possibility

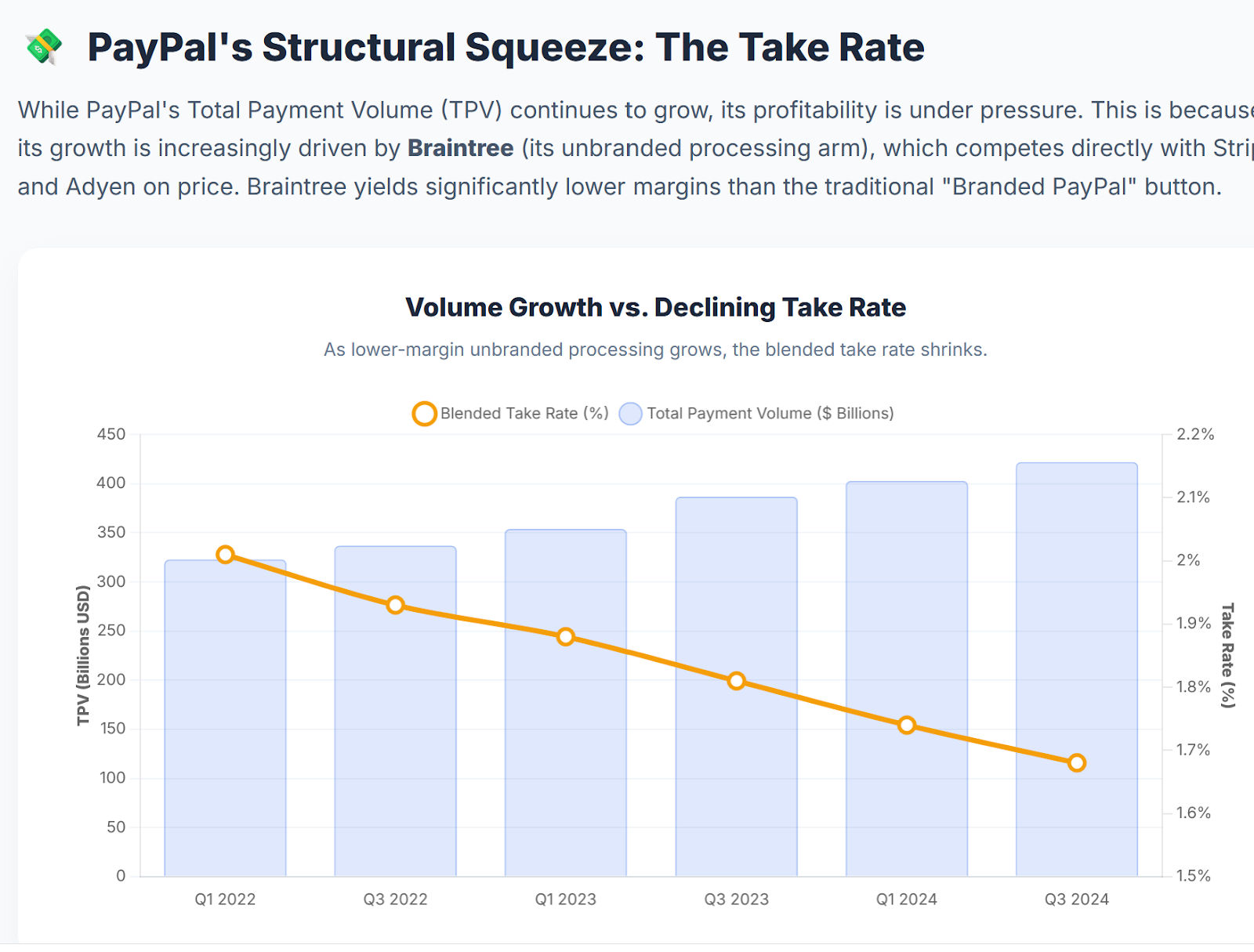

Some folks will argue that Paypal is at present possibly probably the most worthwhile of the funds gamers. The primary driver of this profitability is that Paypal costs considerably increased costs, each to retailers but in addition as an example for worldwide transfers.

What appears now as a power might turn into a weak spot. “Your margin is my alternative” was the well-known motto of Jeff Bezos. The “take fee” of Paypal is heading down for fairly a while (Chart from Gemini) as progress comes primarily from decrease margin merchandise:

Paypal is beneath assault from all sides

Bringing it altogether is that this graph that I requested Nano banana to create:

Paypal is the legacy participant that will get attacked from all facet from very agile and huge opponents who’ve a way more trendy infrastructure,

That’s the rationale why Paypal is affordable. The final CEO tried to counter that however clearly was not very profitable.

The Stripe take-over hearsay

Up to now few days, immediately a hearsay got here up that Stripe would possibly purchase Paypal. To be trustworthy, these sort of “somebody instructed Bloomberg” rumours are sometimes false.

So far as I perceive Stripe’s enterprise mannequin, Stripe would have little to achieve from a takeover. As a pure B2B firm, I’m not certain that the retail consumer base is of curiosity to them and if they might leverage that. And on the B2B facet, Stripe can already do what Paypal is doing and I’m not certain in the event that they need to clear up the technical debt.

I suppose Paypal could be a extra attention-grabbing goal for somebody who would possibly be capable of leverage the retail buyer base, however at 40 bn plus market cap plus premium it’s possibly to large to be swallowed by a lot of the Fintech gamers.

“Too exhausting” for me

For me, the result of this fast train is that Paypal’s downside appears to be rather more structural than momentary which for me makes it “too exhausting” to speculate into.

Perhaps the brand new CEO will pull all of the levers and handle to show across the enterprise. However possibly he is not going to. Will probably be attention-grabbing to see if he’ll be capable of implement a “kitchen sink” method and possibly sacrifice a couple of quarters with actually unhealthy outcomes or if the strain is excessive to maintain up share purchase backs which can make it tough to repay the “technical debt”.

In the meanwhile, Paypal appears just like the hero of Jethro Tull’s music “Too previous to Rock’n Roll”:

The previous rocker wore his hair too lengthy

Wore his trouser cuffs too tight

Retro to the top

Drank his ale too mild

Demise’s head belt buckle, yesterday’s goals

The transport caf’, prophet of doom

Ringing no change in his double-sewn seams

In his post-war-babe gloom

Now he’s too previous to rock and roll

However he’s too younger to die

Sure, he’s too previous to rock and roll

However he’s too younger to die

However anyway, this doesn’t seem like one thing that I might be comfy to be invested in regardless of the superficially enticing “worth KPIs”.

If somebody has a really totally different view from the enterprise perspective with regard to the aggressive panorama, I’m prepared to hear 😉

Bonus Soundtrack:

In fact my alternative is Jethro Tull – Too previous to Rock n’Roll

Jethro Tull – Too Outdated To Rock’n’ Roll (Supersonic, 27.3.1976)