There are charts floating round (once more) claiming that the 30-year mounted mortgage is again to 7%.

These are hyperbolic and deceptive and getting used to sow worry and doom associated to the current uptick in charges.

In actuality, mortgage charges are a few half-point increased than they have been a month in the past, however nowhere near 7%.

Certain, we’ve seen mortgage charges surge increased for the reason that strikes in Iran, however they continue to be firmly within the 6% vary.

And likelihood is they received’t retest these 7% ranges once more, final seen in Could 2025.

Pay Consideration to the Supply! And Their Intentions…

It appears at any time when mortgage charges have a nasty week or a nasty month, the doomers come out and submit the very best mortgage charges they will discover.

They accomplish that as a result of they know they’ll be rewarded with plenty of engagement and views on social media platforms.

Worry sells. And so they prosper!

What’s humorous is that this occurs like clockwork each time mortgage charges pattern increased for a protracted time frame.

There’s some obscure mortgage price chart that all the time appears to be manner increased than the highly-cited nationwide averages from the likes of Freddie Mac and Mortgage Information Day by day.

The intent is obvious – to make potential house patrons assume mortgage charges are unhealthy and that house shopping for is unhealthy.

And that the housing market will certainly crash, in any case these years, as a result of mortgage charges are HIGH once more.

The reality of the matter is mortgage charges are certainly increased than they have been a month in the past due to the tensions within the Center East.

Nearly everyone seems to be conscious of this. But when we zoom out, mortgage charges are solely a few half a share level increased than they have been in February.

Importantly, these month-ago charges have been the bottom we had seen in roughly 3.5 years!

In different phrases, mortgage charges are increased, however solely relative to some actually low ranges.

Mortgage Charges Are Nonetheless Decrease Than They Have been a 12 months In the past

Which means they continue to be beneath year-ago ranges, regardless of this nasty uptick seen in current weeks.

Right now final yr the 30-year mounted was averaging round 6.75%, per Mortgage Information Day by day.

It will definitely elevated to 7%, albeit briefly in each April and Could earlier than falling steadily thereafter to these 2022-lows we had up till the beginning of March.

The hole is narrowing although, as charges have been greater than a full share level beneath year-ago ranges in January and February.

And now they’re solely about .25% decrease than spring 2025 ranges, which is hard for the housing market.

There’s additionally the chance we rise above year-ago ranges within the subsequent few weeks as a result of the 30-year was as little as 6.60% in early April 2025.

In different phrases, sure, mortgage charges are having a tough time in the intervening time, however to say they’re again at 7% is deceptive at finest.

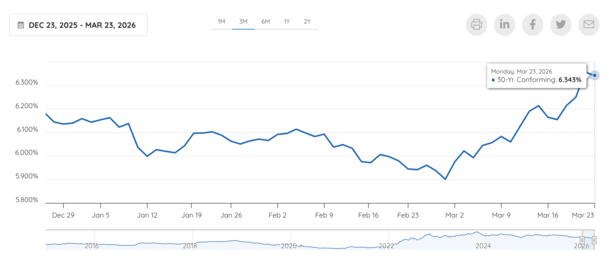

They’re nowhere actually shut. And for those who take a look at precise price locks, the 30-year mounted continues to be round 6.375%.

For instance, Optimum Blue pegged locks at 6.343% yesterday for a 30-year mounted, which is a far cry from the 7s.

Sure, it’s up from 5.90% in late February, which is unlucky, however nonetheless fairly a bit decrease than these scary 7% charges.

Most Mortgage Charge Quotes Nonetheless within the 5s and 6s

As well as, most banks and mortgage lenders I monitor day by day are nonetheless promoting charges within the low 6s or 6.5% at worst.

And if we’re speaking about FHA loans or VA loans, these are nonetheless being marketed within the high-5s.

So all stated, issues aren’t as bleak as you is perhaps led to consider on social media. Shocker I do know.

Merely put, take these fear-mongering posts with an enormous grain of salt.

However for those who’re purchasing mortgage charges, store much more aggressively as a result of there will probably be extra price dispersion than regular in the intervening time given all of the volatility.

This implies banks and lenders can have a wider vary of charges than common so the chance of overpaying (by not purchasing) is increased.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house patrons higher navigate the house mortgage course of. Observe me on X for warm takes.