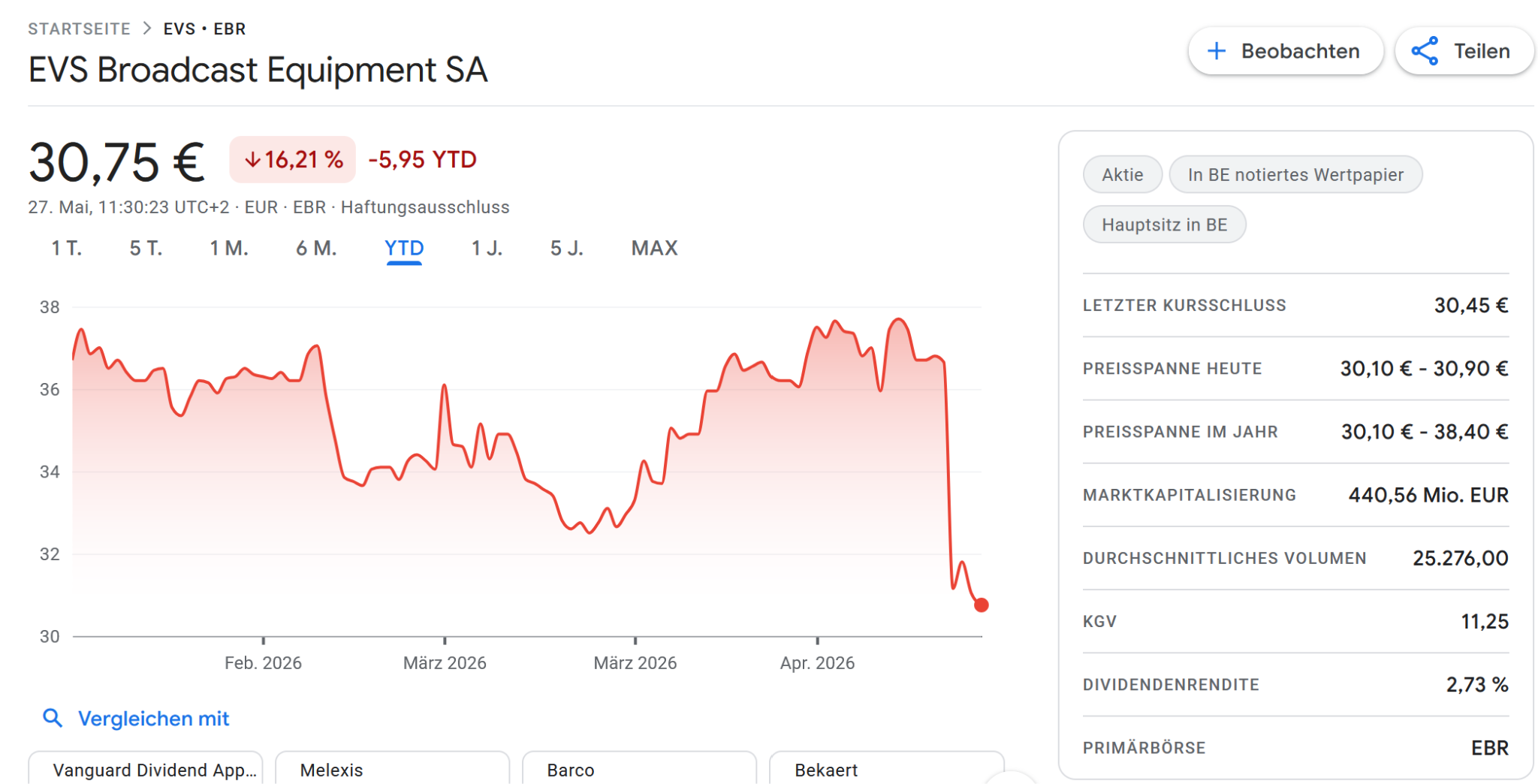

EVS Broadcast

Let’s begin with probably the most disappointing replace first: EVS Broadcast bought slammed down after their Q1 buying and selling assertion:

I believe three objects spooked buyers, together with myself:

First, after confirming the steering, each within the CEO and CFO assertion, the press launch out of the blue comprises this sentence within the Outlook part:

“Specifically, the present scenario within the Center East could have an effect on full-year income efficiency and could lead EVS towards the decrease finish of the steering vary. On the similar time, given the energy of the pipeline and the alternatives at present recognized, we consider there stays potential to offset this affect by execution in different areas of the enterprise. “

Second, as soon as once more they point out that the 2026 yr will probably be “again loaded”, i.e. buyers may have little visibility how issues will develop till the top of This fall.

And at last, the departure of the CFO woman and not using a direct alternative can also be not optimum. I assume there was some rigidity within the board.

Longer time EVS shareholders know that they at all times information cautiously, however 2026 as an “occasion yr” ought to have been an excellent yr and now it appears that it’ll not be materially higher than the yr earlier than.

Anyway, for the time being I’m clearly not growing my place in EVS, relatively the alternative. It was one in all my bigger positions and I believe except one thing modifications (like possibly an enormous share buyback program), I’ll stay relatively cautious.

Jensen Group

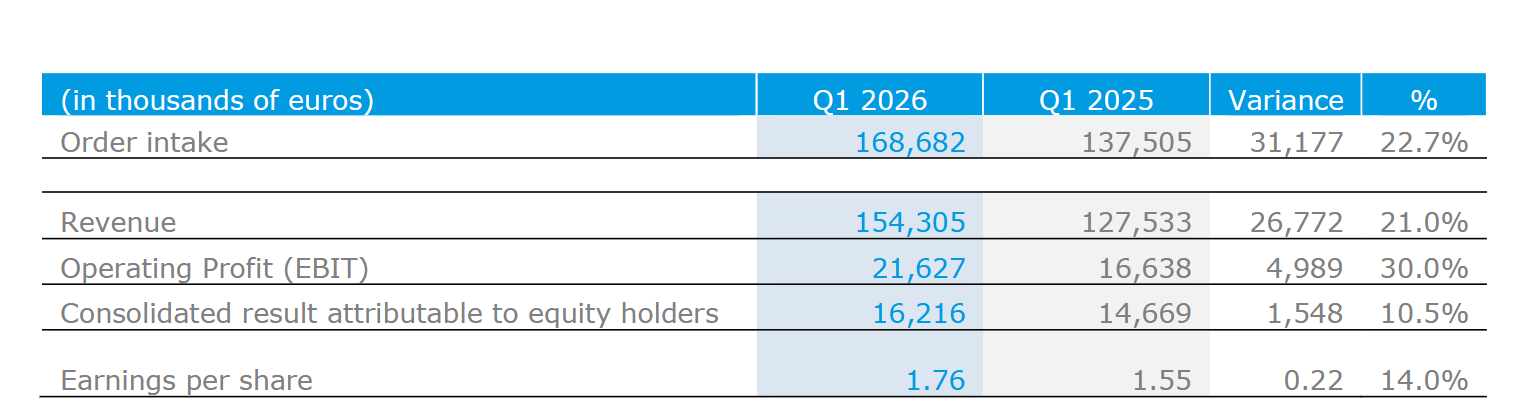

Fortunately sufficient, my second Belgian inventory, Jensen Group, is the precise reverse of EVS. As soon as once more they began with a fantastic quarter into the yr and are “firing on all cylinders”.

The numbers look unbelievable, the one query is why internet earnings solely rose by +10%, however possibly there was a tax impact:

They maintain shopping for again shares ( a brand new 10% buyback program has been accepted), book-to-bill is >1 and regardless of a brand new all time excessive, the inventory continues to be low cost as earnings develop as quick because the inventory value goes up.

There’s at present Completely nothing to complain with this firm in addition to the truth that buyers suppose that 11xP/E is the proper valuation for such an excellent firm.

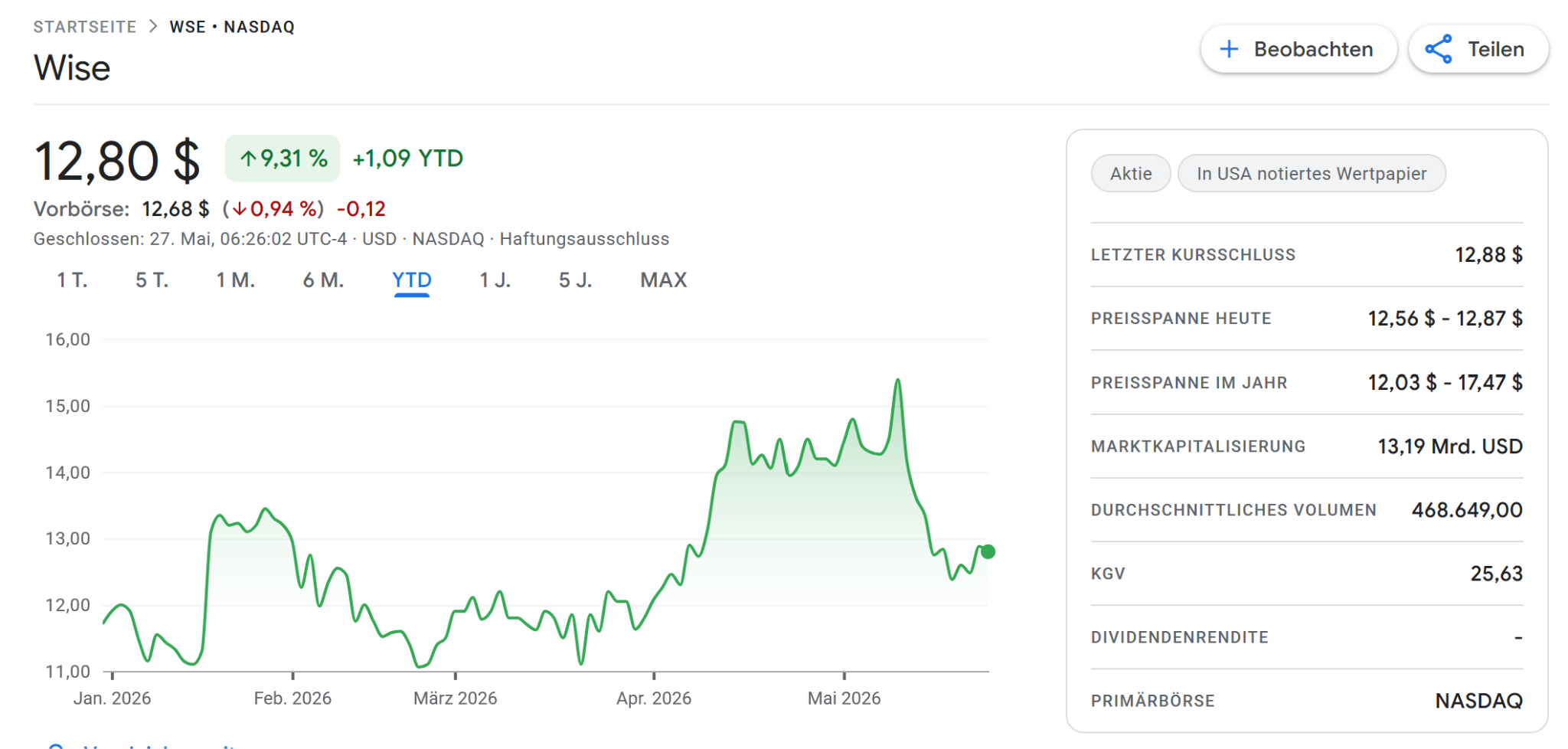

Clever Plc

Clever Plc lastly listed on the Nasdaq and as a consequence, I do now have a Nasdaq listed share in my portfolio. The share value went up earlier than the itemizing and really reached its peak on the day of the itemizing on Might eleventh, solely to drop considerably within the aftermath:

The itemizing for me was not the last word motive to speculate, however in fact it’s fascinating to see how a lot the inventory dropped straight after the itemizing.

One issue might need been that JP Morgan appears to have diminished its value goal by greater than 10% following the itemizing.

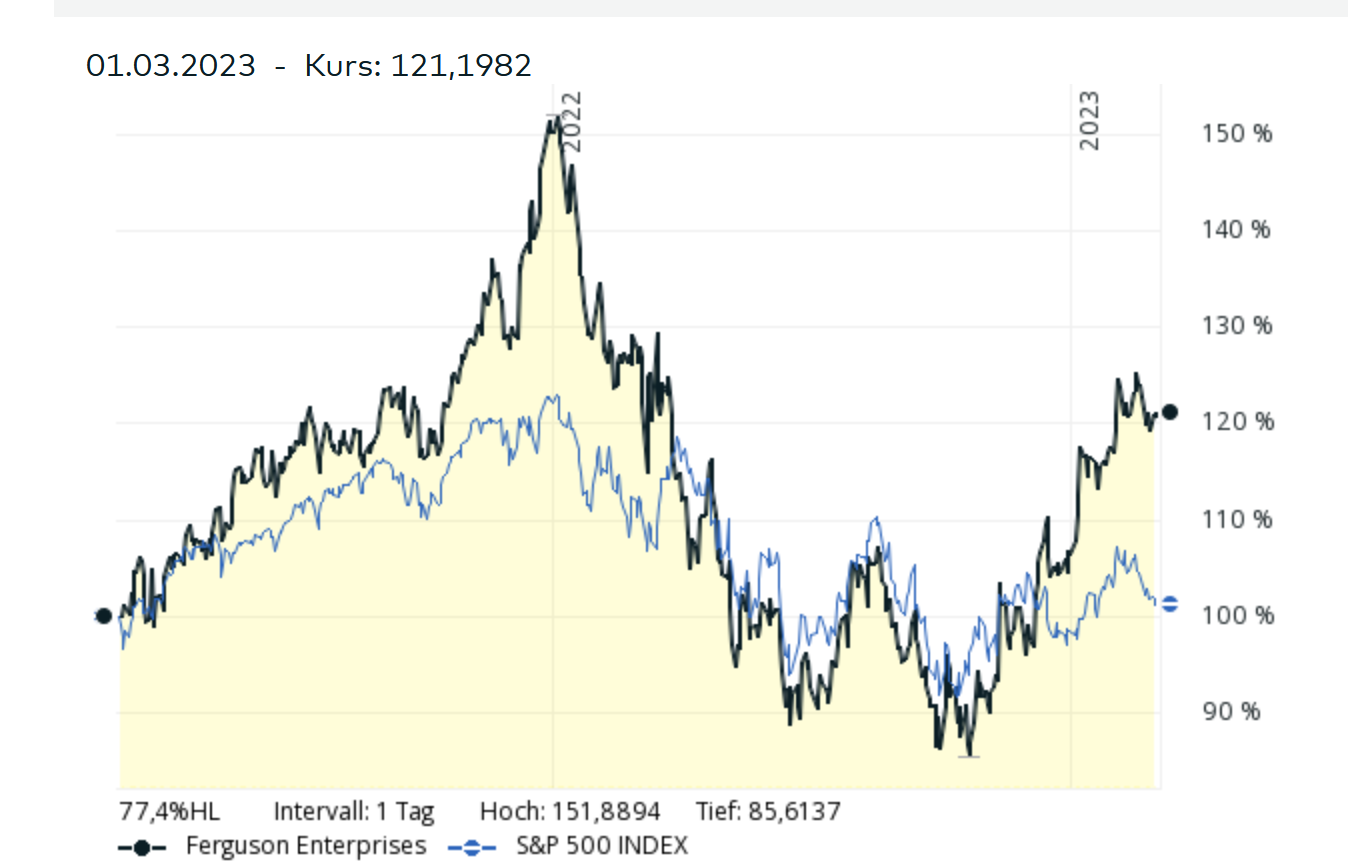

Though not precisely so, this resembles somewhat bit wehn Ferguson (Wolsely) moved its major itemizing to the US in March 2022. As we will see within the historic chart, the inventory outperformed considerably earlier than that transfer however then underperformed for a while thereafter:

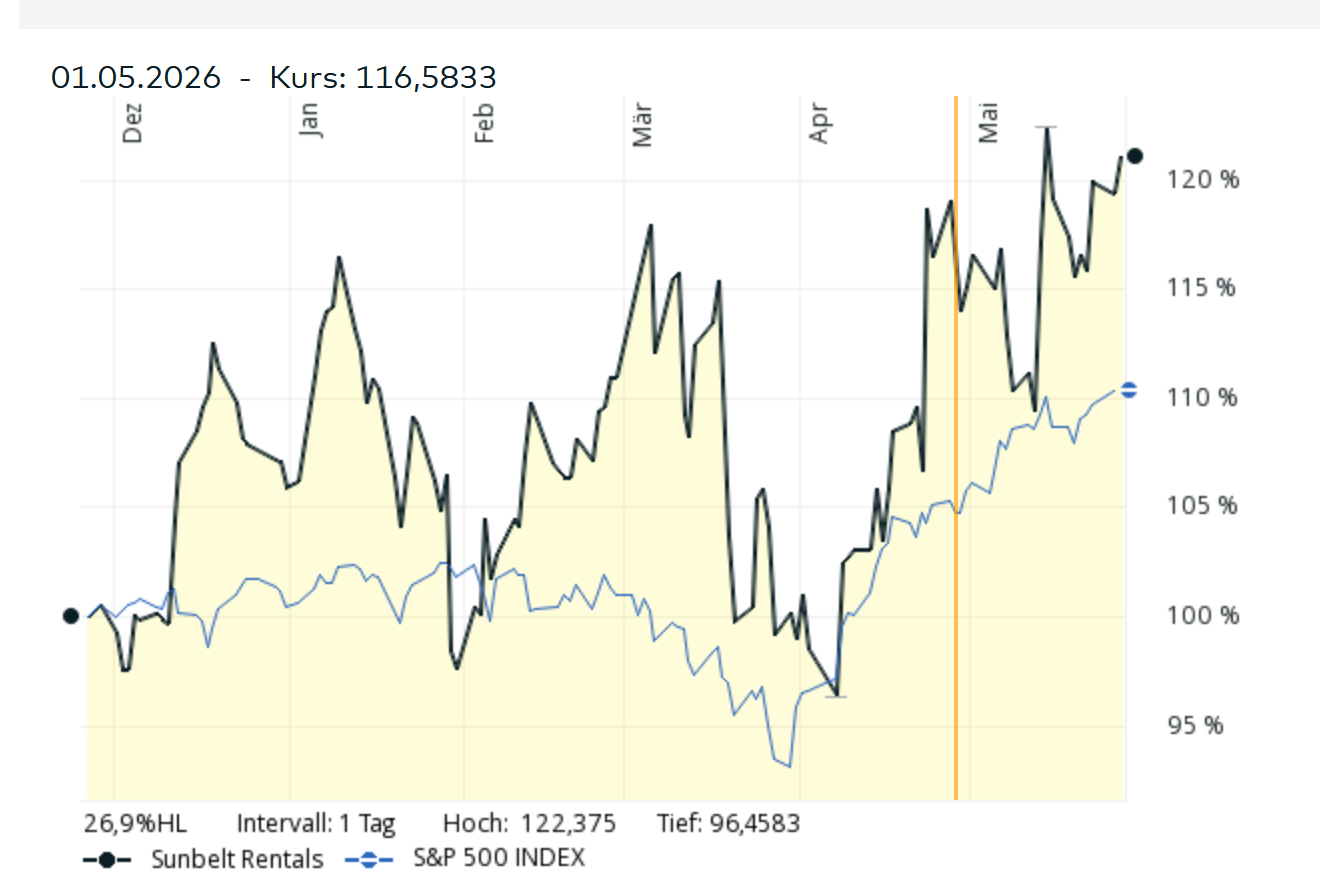

Sunbelt leases (the previous Ashtead) additionally so a drop in relative efficiency a couple of days after its itemizing at first of MArch 2026, however that’s most probably as a result of begin of the Iran conflict:

Anyway, from a basic facet, there hasn’t been any change with regard to Clever’s prospects, so no motion there.

Installux

Lastly, a few of my readers would possibly do not forget that I owned the French Micro Cap Installux for a while (purchased in 2012 in the course of the EUR disaster) however offered in 2021 with an honest return regardless of the inventory being nonetheless low cost.

Yesterday, out of nowhere, Installux out of the blue revealed that they purchased out the most important minority shareholder, French Worth Asset Supervisor Amiral at a share value of 500 EUR per share vs. 290 EUR which was the final commerce earlier than that announcement.

Apparently, the Canty household now has ~88% of the shares and is extending the supply to all different shareholders. Apparently the five hundred EUR are nearly the all time excessive from 2021:

Installux is an fascinating case research insofar because the household clearly had little or no incentive to indicate to the surface how good the enterprise truly is. Their long run mission was clearly to get full management of the corporate. Amiral actually had quite a lot of persistence right here.

On the finish of the day it reveals that in case you make investments into shares like Installux, timing and persistence is absolutely every part. You both should get in when they’re extraordinarily low cost or be fortunate to be there when the household lastly needs to realize full management.

On the constructive facet, the Canty household by no means did something fishy and the ultimate supply appears type of truthful.