Rocket Web Put up Mortem

Final week I discussed within the feedback on the weblog and on Twix that I obtained some “unhealthy vibes” and determined to liquidate my Rocket Web place even earlier than the deliberate SpaceX IPO subsequent week.

There have been general 3 issues that form of spooked me and let me to take the revenue (+30%) as an alternative of ready the yet one more week. Listed here are the three gadgets:

- I discussed initially, though it was not a part of my funding thesis, that there is perhaps an opportunity of a particular dividend. Now it has grow to be clear that there will probably be no particular dividend. Nonetheless, it additionally turned clear that Rocket Web intends to restrict data move to shareholders much more sooner or later which is clearly not optimistic

- SpaceX: One other information merchandise that spooked me was that SpaceX is aggressively pitching by way of German brokers for German retail buyers. German buyers had by no means entry to US IPOs earlier than. Some may discover this optimistic, I discover that relatively “stunning” and probably a touch that demand shouldn’t be excessive sufficient for Elon’s urge for food.

- One other stunning occasion was the “shock Capital improve” from Alphabet/Google. Apparently, this represented the biggest capital improve of all time at 85 bn USD however there was solely very restricted protection about it within the monetary information and principally about Berkshire’s participation. However extra on this later

General, I made a decision that the “straightforward cash” was now made with Rocket web and I used to be in a position to promote at round 25,80 EUR per share, netting a revenue of 30% inside 5 months, which is clearly one in all my higher “Particular conditions” investments.

I’m not 100% certain that the share value improve was pushed by SpaceX, possibly the fast improve within the worth of the Kalshi stake helped as effectively. I’m not certain if there are loads of different “performs” to profit from KalshI’s unimaginable progress.

One might argue that I left some upside on the desk right here however the success of this funding is nearly 100% relying for a while on another person paying me extra for the shares that I paid for, which is one thing I don’t really feel too snug for a particular scenario funding.

General, I used to be clearly fortunate with the timing on this one.

2. Extra SpaceX ideas: Hyperliquid Perps and Damodaran

Since I wrote my replace on Rocket Web and SpaceX a number of days in the past, fairly some issues occurred.

As talked about above, we now know that Elon loves Germany a lot that on the time of writing, German retail buyers can now entry this IPO by way of 8 or 10 completely different retail brokers.

Apparently, SpaceX form of already trades in an artificial for as a “perpetual future” on a crypto alternate referred to as Hyperliquid:

In accordance with some sources, to be able to evaluate apples to apples, one would want to low cost the worth by 10% to make it akin to the precise SpaceX shares. Which means on this “gray market”, an artificial SpaceX share solely trades at ~153 USD, above the 135 USD “sticker value” however contained in the 135-162 USD bookbuilding vary.

Though nobody is aware of for certain if this has any relevance, it’s not less than a reference level and it appears to be traded fairly liquid.

One other attention-grabbing supply is the try of a valuation by Prof. Damodaran. What I like about Damodaran is that he at leasts tries to place values on these form of conditions and could be very clear along with his assumptions. I do know most tech bros snigger about these makes an attempt however I feel avery severe investor ought to learn what Damodaran writes as a result of there’s at all times so much to study.

In a nutshell, Damodaran values SpaceX at about 100 USD per share. The ain modifications to his preliminary, pre prospectus valuation is that he elevated the margins for the House and Starlink enterprise, however considerably decreased the anticipated margins for the AI enterprise.

“My largest shift is in my estimated goal margin is for the AI enterprise, the place the dynamics which can be pushing gross margins down, i.e., elevated competitors and excessive prices of delivering AI providers, will persist; my estimated working margin drops from 45% to 25%. “

Damodaran can be good sufficient to say that within the first days after the IPO, valuation clearly doesn’t matter in any respect. However throughout the first 12 months or so, even for SpaceX, actuality will should be met in some way.

For me nevertheless the primary take away is the considerably diminished margins for the AI enterprise which leads me to the:

Stunning 85 bn USD Capital improve of Alphabet

Being a Company Finance/Treasury man by coaching, the information that Alphabet is elevating 85 bn USD by way of a capital improve actually shocked me.

The “package deal” itself is kind of advanced. After asserting initially 80 bn USD in complete proceeds, Alphabet ended up with ~85 bn.

In accordance with the FT, that is the biggest capital improve within the historical past of capital markets, the second largest was Petrobras in 2010 at round 70bn.

The monetary press targeted primarily on the ten bn stake that Berkshire Hathaway took as a part of the package deal. To be sincere, it is a very small amount of cash for Berkshire’s present dimension. It’s also exhausting to actually choose how good of an investor Greg Abel truly is.

The attention-grabbing factor about this capital improve is that up to now, not less than within the ~40 years that I observe inventory markets, capital will increase in dimension solely occurred within the following conditions:

- Major share portion in an IPO

- Emergency capital elevating in a disaster ( e.g. Banks within the GFC)

- Main M&A transaction the place the buying firm pays with new shares (Paramount)

In Google’s case, clearly not one of the three conditions applies. In accordance with TIKR, Alphabet nonetheless has web money regardless of ~100 bn in bonds excellent. So in idea they might situation much more debt.

I heard the argument that Fairness is “cheaper” than debt because the rate of interest on a debt providing could be 5% whereas the “earnings yield” on the present 30x P/E is “solely” 3,3%. Nonetheless this doesn’t replicate the tax protect from curiosity and particularly not the truth that Alphabet’s earnings will almost definitely improve for the foreseeable future and that very quickly that “earnings yield” for the issued shares will probably be a lot larger than the present 3,3%.

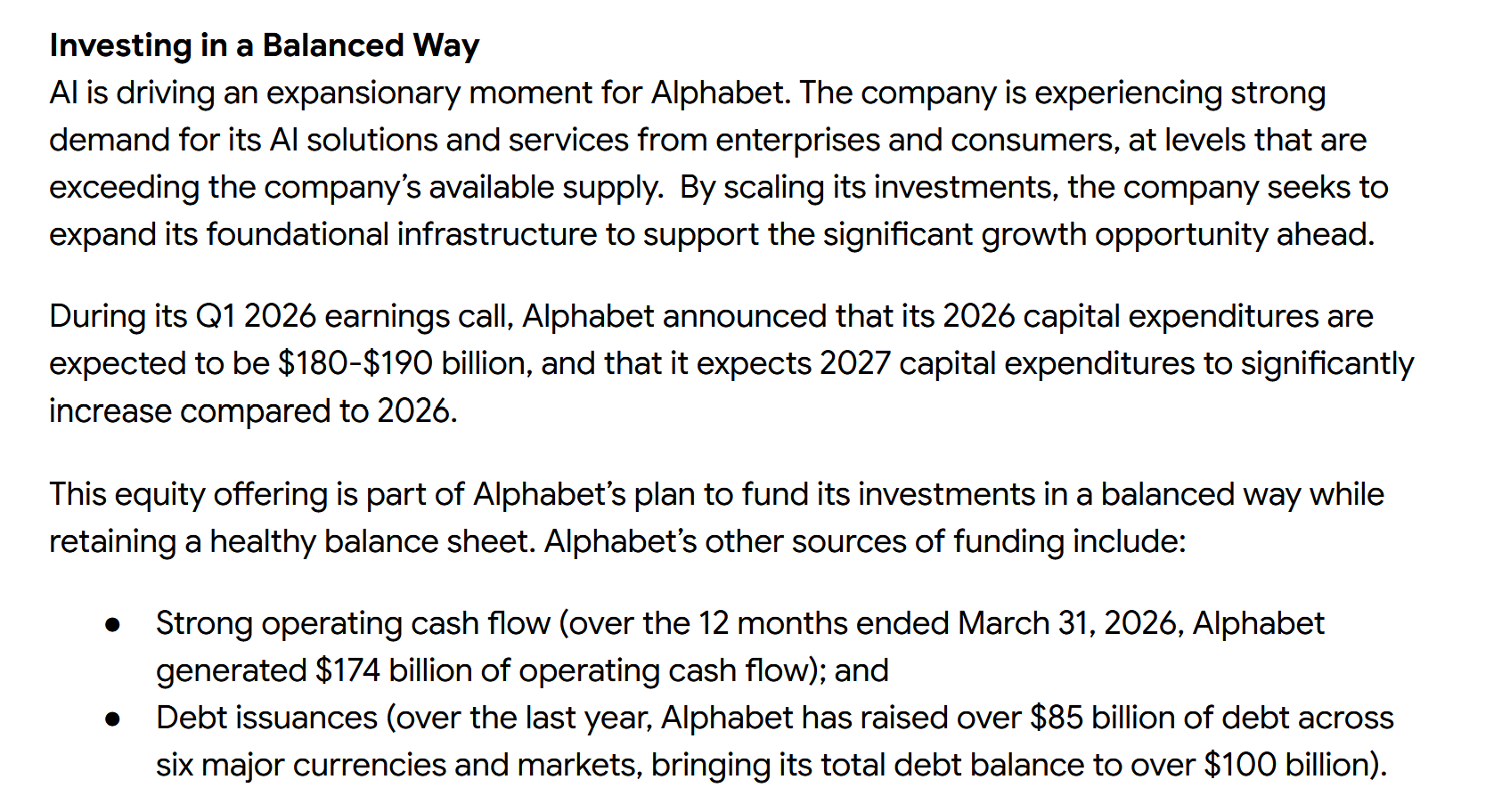

That is the primary “justification” of Alphabet for the capital elevate in addition to a 30 bn extra tax invoice:

If you happen to learn this rigorously, it’s clear that they might nonetheless fund the 2026 Capex kind of with working cashflow, however already in 2027, they plan to spend rather more than that.

The actually attention-grabbing factor is clearly: What are their plans past 2027 ? My greatest guess is that they plan with even bigger investments that aren’t offset by working money move.

Besides, why not wait till 2027 or so after they have a clearer viewpoint ? And I feel right here comes one thing into play which in my outdated Company Finance days was the golden rule of financing: “Elevate when you possibly can, not when you should”.

I feel the Alphabet guys may need seen SpaceX’s announcement, they know that OpenAI filed for an IPO and that Anthropic will come to the capital markets as effectively.

As giant because the listed capital markets are, there’s solely a lot urge for food for capital will increase. Possibly they even concern a big market correction which might require them to situation a a lot bigger variety of shares for a similar amount of cash.

Funnily sufficient, there have been rumours that even Meta appears to consider elevating giant quantities of capital to fund their AI Capex applications.

One different issue that may additionally play a task right here is that each, Non-public Credit score and Non-public Fairness which have been providing important quantities of capital up to now struggle with redemptions themselves and are probably overallocated to information centres already.

To me it’s fairly unclear the place all that is going. Nonetheless one factor now’s clearer to me:

The capital required to scale up this expertise is bigger than even the most recent and greatest funded gamers like Google anticipated.

In my view, because of this it is extremely unlikely that we see 5 firms scaling this in parallel on their very own (Alphabet, Meta, OpenAi, Anthropic & SpaceX). 1,2 and even 3 of these gamers may fold in some unspecified time in the future in time or would want to collaborate actually carefully with somebody like Microsoft or Apple to remain within the race. Or get assist from the Orange man in some kind.

Scrutinizing Knowledge Centre Infrastructure orderbooks

For extraordinary buyers this may also imply to raised scrutinize order books of firms which can be purported to revenue from an additional AI construct out and commerce at excessive multiples themselves.

In the intervening time, it’s sufficient if an organization releases “AI information centre” contracts to justify sky excessive multiples. I assume going ahead, possibly even before later, one actually wants to grasp from which counterparts these contracts are. As a result of not all of them is perhaps truly turn into beneficial.

In any case, as somebody who loves capital markets, it is a nice time to be alive and witness what’s going on in the meanwhile.