With mortgage charges above 6.50% nowadays, the common residence purchaser right this moment really pays extra in curiosity than the acquisition value.

For instance, a $400,000 residence with 20% down and a 6.5% rate of interest equates to $408,000 in complete curiosity over 30 years.

And that’s when you put down 20%. Many residence patrons don’t put down 20% or wherever shut.

For these patrons, the mathematics is even worse, one thing highlighted in a current report from Greatest Curiosity Monetary and Intelligent Actual Property.

Whereas month-to-month fee would possibly nonetheless be the main target, it’s one more arduous capsule to swallow for a potential residence purchaser right this moment.

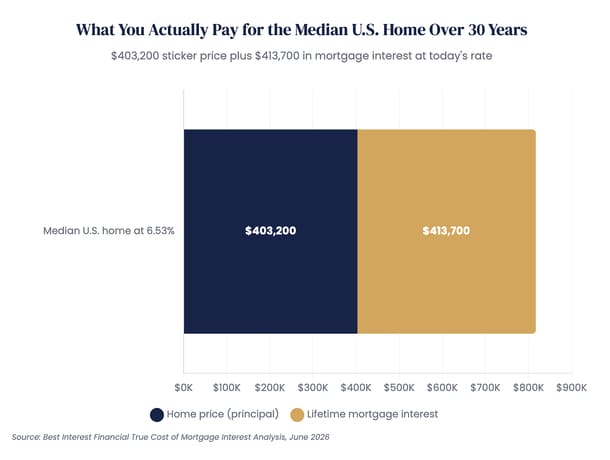

You Pay Extra In Curiosity Than the Dwelling Prices?

Greatest Curiosity Monetary and Intelligent Actual Property got here up with this fascinating little graphic displaying a median residence value would price extra in curiosity over 30 years than the acquisition value.

The reason being easy; mortgage charges are rather a lot larger right this moment than they had been within the current previous.

So a $403,200 residence with a 20% down fee and a 6.53% 30-year mounted would set you again $413,700 in curiosity.

It might sound arduous to consider given the rate of interest is a low 6.53%, however that’s how mortgage curiosity works.

As a result of it’s amortized over such a protracted time frame, and the excellent steadiness is so massive for many of that point, you pay a ton of curiosity over three a long time.

With a 20% down fee, complete curiosity really exceeds the house value as soon as your 30-year mounted mortgage fee is over 6.4%.

At present, mortgage charges are nearer to six.7% so the full curiosity expense is even larger than this.

To make issues even worse, the everyday residence purchaser would possibly put down as little as 3% (what Fannie Mae and Freddie Mac enable as an absolute minimal).

On this case, an rate of interest of 5.45% is excessive sufficient in order that complete curiosity equals the acquisition value.

As famous although, most folk solely concentrate on their month-to-month fee and what they’ll afford, not what they’ll really pay in curiosity over the lifetime of the mortgage.

As well as, most gained’t preserve their loans for the total time period for one purpose or one other, whether or not it’s an early sale, refinance, or prepayment.

The takeaway is that the decrease the down fee, the decrease the speed wanted for curiosity to exceed the price of the house.

For instance, when you put nothing down on a house buy, a mortgage fee as little as 5.30% means curiosity exceeds the acquisition value.

Whether or not that issues to you is one other query.

What You Can Do to Cut back Whole Mortgage Curiosity

If it bothers you that you just’re going to pay extra in curiosity than what you paid in your residence, there are alternatives.

The good factor a few mortgage is it’s usually permissible to prepay it as you see match with out penalty.

So if you wish to pay an additional $250 monthly, you’re ready to take action. That would scale back the full curiosity expense considerably.

For instance, let’s use a $400,000 buy value with 20% down fee and a 30-year mounted fee of 6.75%.

The full curiosity is simply over $427,000 over the total 30 years, assuming you retain the mortgage to time period.

Alternatively, when you pay $250 further every month the full curiosity drops to $296,623.

You’re now not paying extra in curiosity than the price of the house. Woo hoo!

You’d additionally pay the mortgage off almost eight years earlier as nicely. Good.

The purpose right here is that there’s optionality with mortgages and also you’re not caught with solely the “minimal fee.”

In case you have the means, you possibly can pay further everytime you’d like and cut back that curiosity expense.

Utilizing the $250 further instance, you wind up with an equal rate of interest of about 4.97%.

That means a 30-year mortgage set at 4.97% would produce nearly precisely the identical complete curiosity.

Learn on: Strive my early mortgage payoff calculator to run your personal state of affairs.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 20 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on X for decent takes.