DCC/Intertek

As anticipated in my submit from a month in the past, KKR now got here again with a greater provide after DCC’s board rejected the preliminary of 58 GBP per share.

This time, KKR provided 65,25 GBP in money per share, plus a dividend of ~1,47 GBP per share to be acquired in July.

This can be a 12,5% improve (ex dividend) from the preliminary provide. Lower than I anticipated however it appears the board off DCC is already proud of this:

Having rigorously evaluated the Revised Proposal along with its advisers, the Board of DCC considers that the monetary phrases of the Revised Proposal are at a stage which the Board of DCC could be minded to advocate to DCC shareholders ought to a agency intention to make a proposal pursuant to Rule 2.7 of the Irish Takeover Guidelines be introduced by the Consortium on the identical monetary phrases, and topic to the passable settlement of the complete phrases and circumstances of any provide and passable settlement and execution of definitive transaction documentation.

Simply to be clear right here as a reader requested why the value didn’t immediately soar to the provide worth.: KKR hasn’t made a proper provide but. That is so to say the “pre-discussion”.

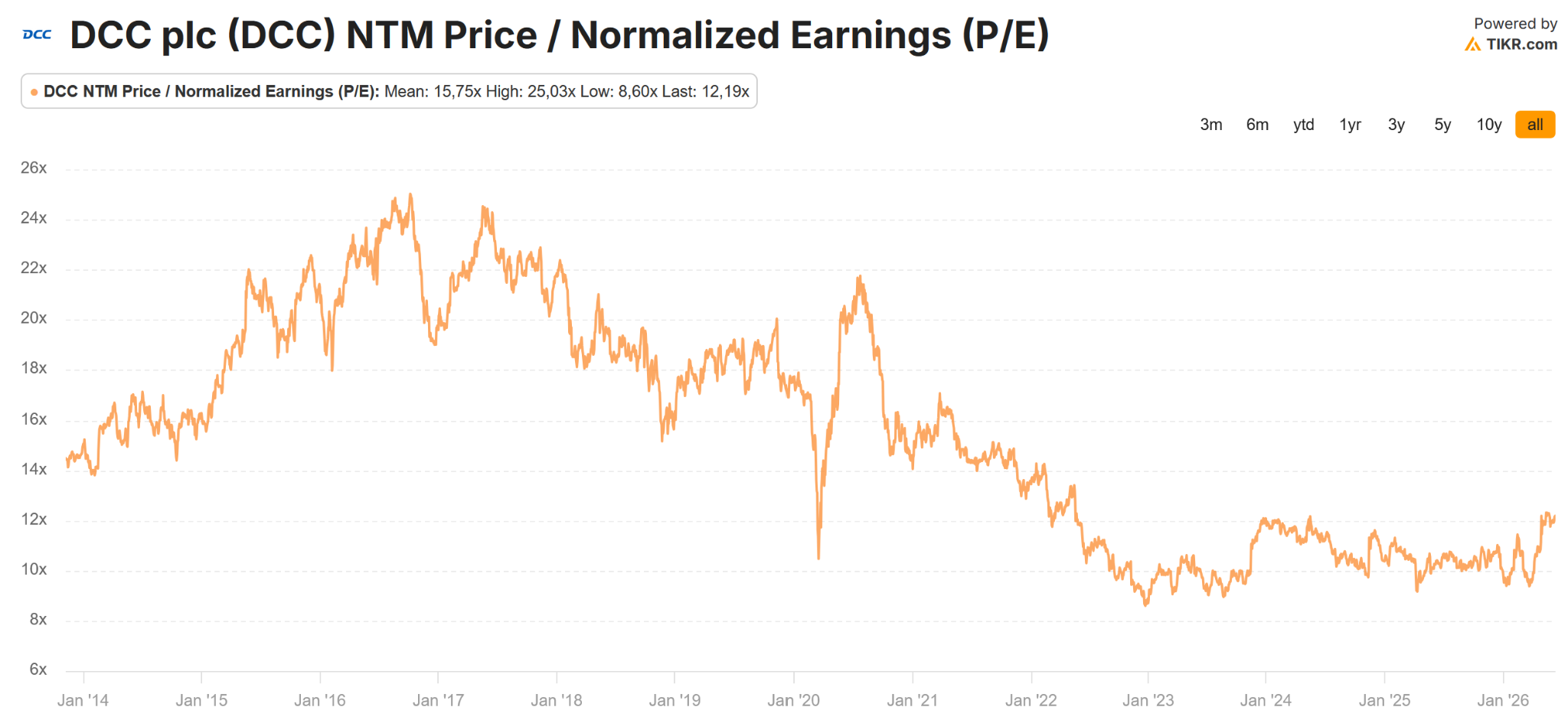

DCC’s long run share worth, the provide worth equates roughly the share worth DCC had 10 years in the past:

Trying on the historic P/E, we will additionally see that 2026 was the interval in time when individuals thought that DCC is a 24x NTM P/E enterprise:

As DCC’s board appears to have already accepted the bid, the one additional upside could be now a counterbid from one other PE fund or a strategic purchaser.

I’m not certain how possible that’s, however perhaps not 0% both.

Intertek

As I had talked about Intertek earlier, it’s unfold to the (potential) 60 GBP plus dividend provide from EQT has tightened slightly, as a result of there was a hearsay that Swiss primarily based testing firm SGS could be considering a competing provide.

Such rumours are literally not uncommon in these conditions. Generally they’re launched by hedge funds who may not need to wait till the provide is executed however get out near the provide worth lengthy earlier than that. In different circumstances, the hearsay really turns into true.

Smart Plc – What’s the potential impression of the AML concern

A couple of days in the past, Smart Plc shocked its buyers, after it was revealed that authorities in Belgium are investigating Smart with regard to Anti Cash Laundering rules in an quantity of 500 mn EUR.

The FT interestingly reported a couple of comparable incident in Belgium in 2024, following the Russian invasion in Ukraine.

I feel what’s necessary to know is that the subsidiary in Belgium shouldn’t be a tiny little subsidiary however mainly dealing with all Euro transactions for WISE. I suppose this has regulatory causes.Sadly, Smart doesn’t report what share of its volumes have one leg in EUR, however it’s clearly a really vital foreign money.

The dimensions of a possible wonderful

The query that I had and tried to resolve with AI is the next: Suppose Smart is “responsible”, what could be the wonderful they must pay and what or the opposite penalties ?

In actuality, with out making this to sound innocent, these form of AML points should not that uncommon, so there are precedents.

Here’s what Gemini is saying:

- the utmost cost from a legal perspective (if responsible) in Belgium is “solely” 1,6 mn EUR

- the utmost penalty from an administrative facet could possibly be as much as 10% of gross sales or in Smart’s case round 190 mn EUR

- In observe, the fines usually appear to be a stage of 1% of the amount. So total, Gemini estimates the wonderful to be within the vary 5-10 mn EUR. Which might be not a lot.

Oblique prices: Extra compliance

The extra important half could possibly be price will increase via moreover required Compliance features. Gemini estimated that complete compliance prices (which the estimate at 260 mn GBP at Smart) might improve by 30%, which might be round 80 mn GBP/100 mn EUR per yr, which might be fairly vital.

I feel that’s perhaps an over-estimation, as to this point, this solely issues the European operations. however nonetheless, 10-30 mn EUR per yr could possibly be lifelike.

Moreover, now we have now in fact US shareholder litigation and probably some reputational points.

An additional threat is that extra compliance additionally perhaps means much less buyer satisfaction and slower progress.

If we take Could twenty ninth as a reference, the place the share worth was at 9,35 GBP, as of the time of writing, the share worth is down ~1,15 GBP or -12%. In financial phrases, Smart misplaced greater than 1 bn GBP in market cap.

Cost typically has a troublesome time in 2026

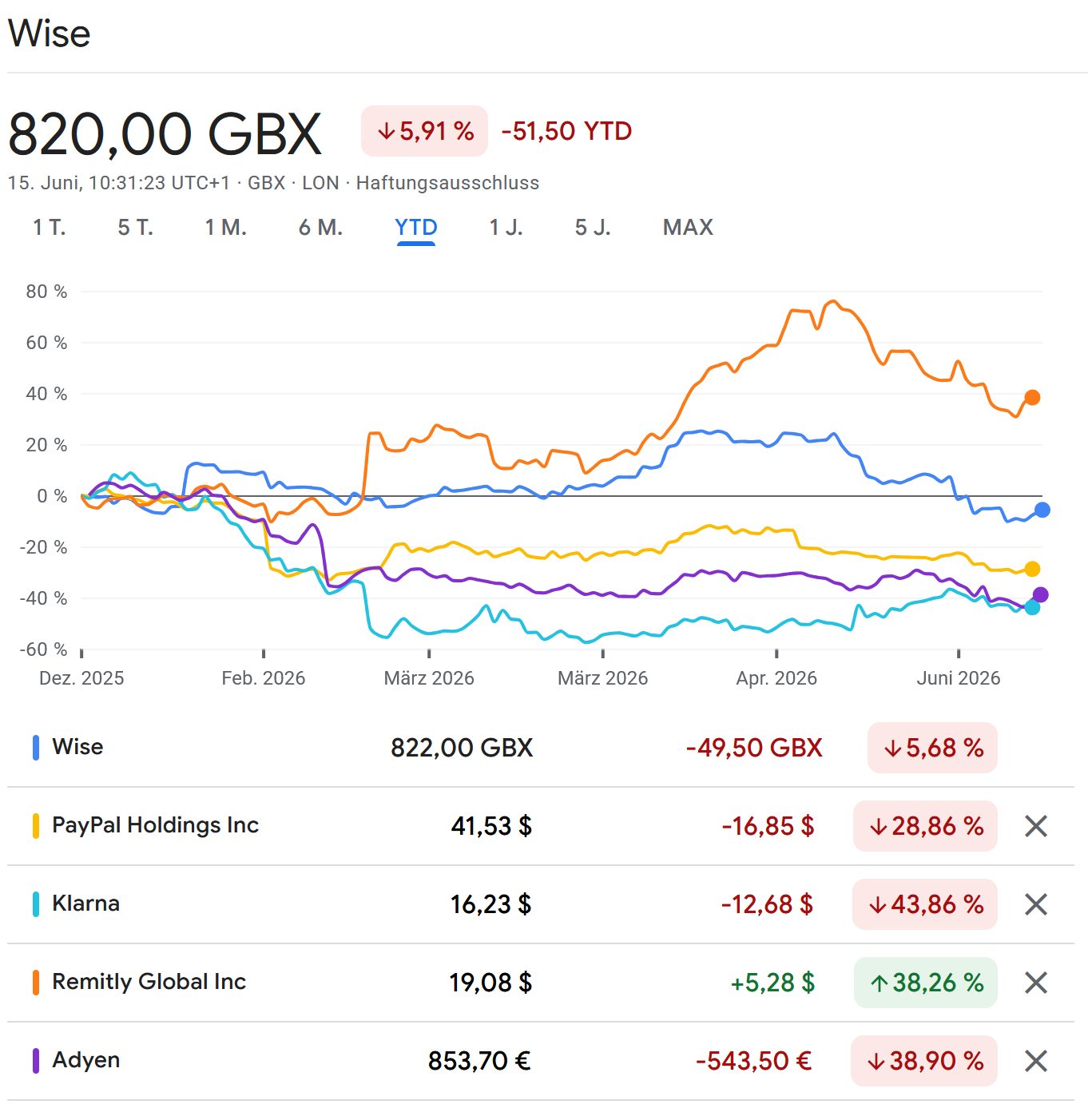

One other side is that funds typically should not doing that nicely in 2026. I’ve collected a small peer group right here the place Smart continues to be one of many higher performers:

So the place does that depart us with Smart:

For me, it’s presently too early to say if and the way this might impression Smart sooner or later. The share worth drop clearly costs some ache and AML is all the time a threat for cash switch companies, however I’m not 100% certain if now’s the time to extend the place. So I personally will look ahead to the following 2 or 3 quarters to see if progress retains up and perhaps add then.

If the share worth falls considerably from right here, I’d somewhat promote and watch.