DISCLAIMER: This isn’t funding recommendation. The creator may personal, purchase or promote shares with out advance discover. The assumptions is likely to be flawed or outright mistaken. PLEASE DO YOUR OWN RESEARCH !!!!

Government Abstract:

Norma Group, a beforehand PE owned German producer of small connector elements, is planning to make use of a part of the money it acquired from promoting a division to purchase again a big share (>30%) of its excellent shares through a young supply at a premium of as much as 20% in comparison with the present share value.

Though there are some shifting elements and the general case turned out to be extra sophisticated than I assumed initially, this represents a possible uncorrelated particular state of affairs for 3-4 months with an anticipated (likelihood) return of round 13% primarily based on my assumptions.

Norma Group Background/Introduction

Norma Group has clearly seen higher days. IPOed in 2011 as a beforehand PE held firm (3I), the inventory value did nicely till 2019 earlier than then dropping -80% when the inventory value reached a low of beneath 10 EUR per share in early 2025:

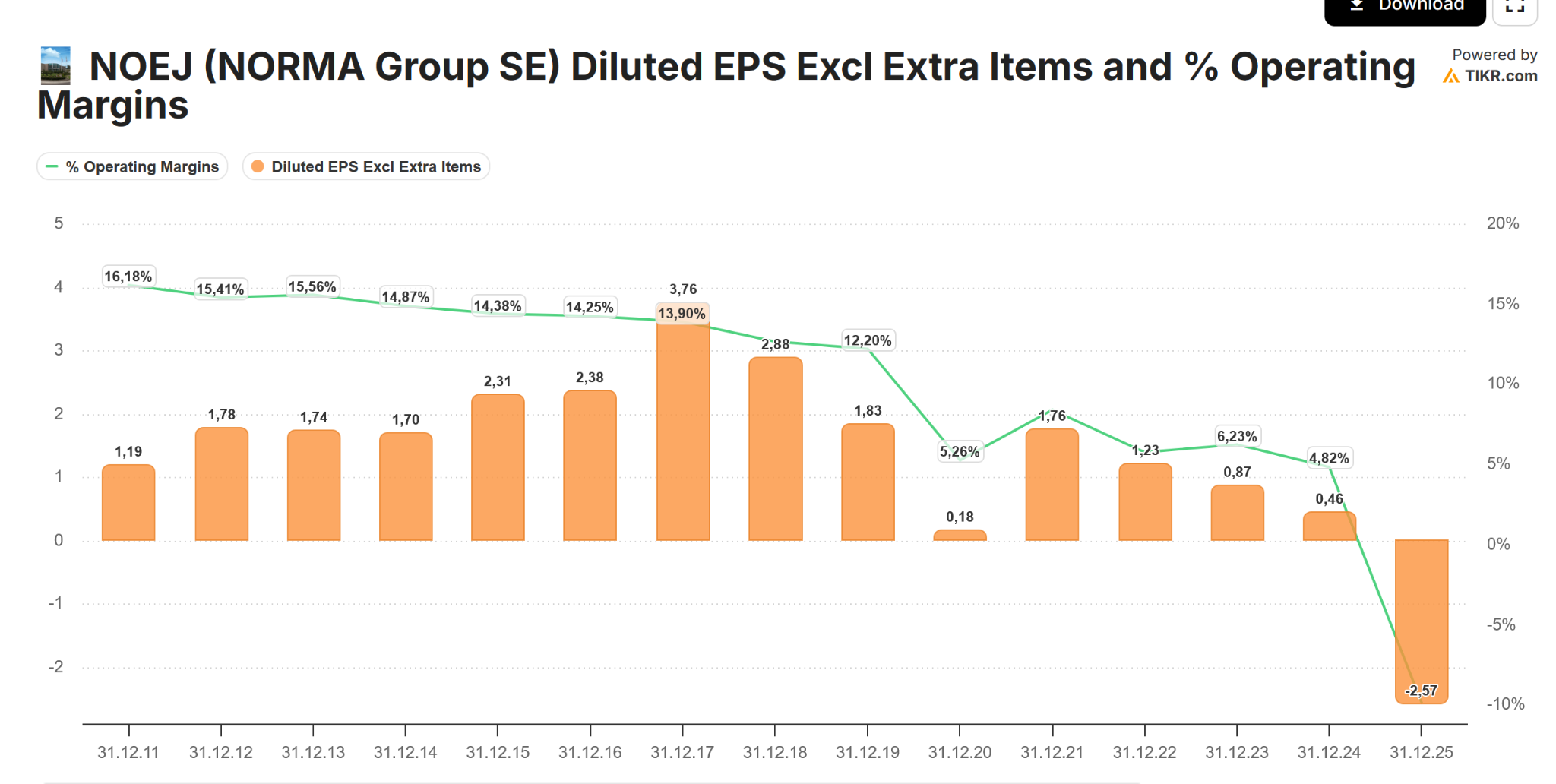

Curiously, in response to TIKR, Working margins had been on a downtrend because the IPO date and EPS peaked in 2017, however till 2019 nobody bothered an excessive amount of:

Norma was lively in what they known as “becoming a member of know-how”, primarily connectors and different small elements out of metallic and plastics for industrial purposes, the automobile business and “water purposes”. Right here a pattern image:

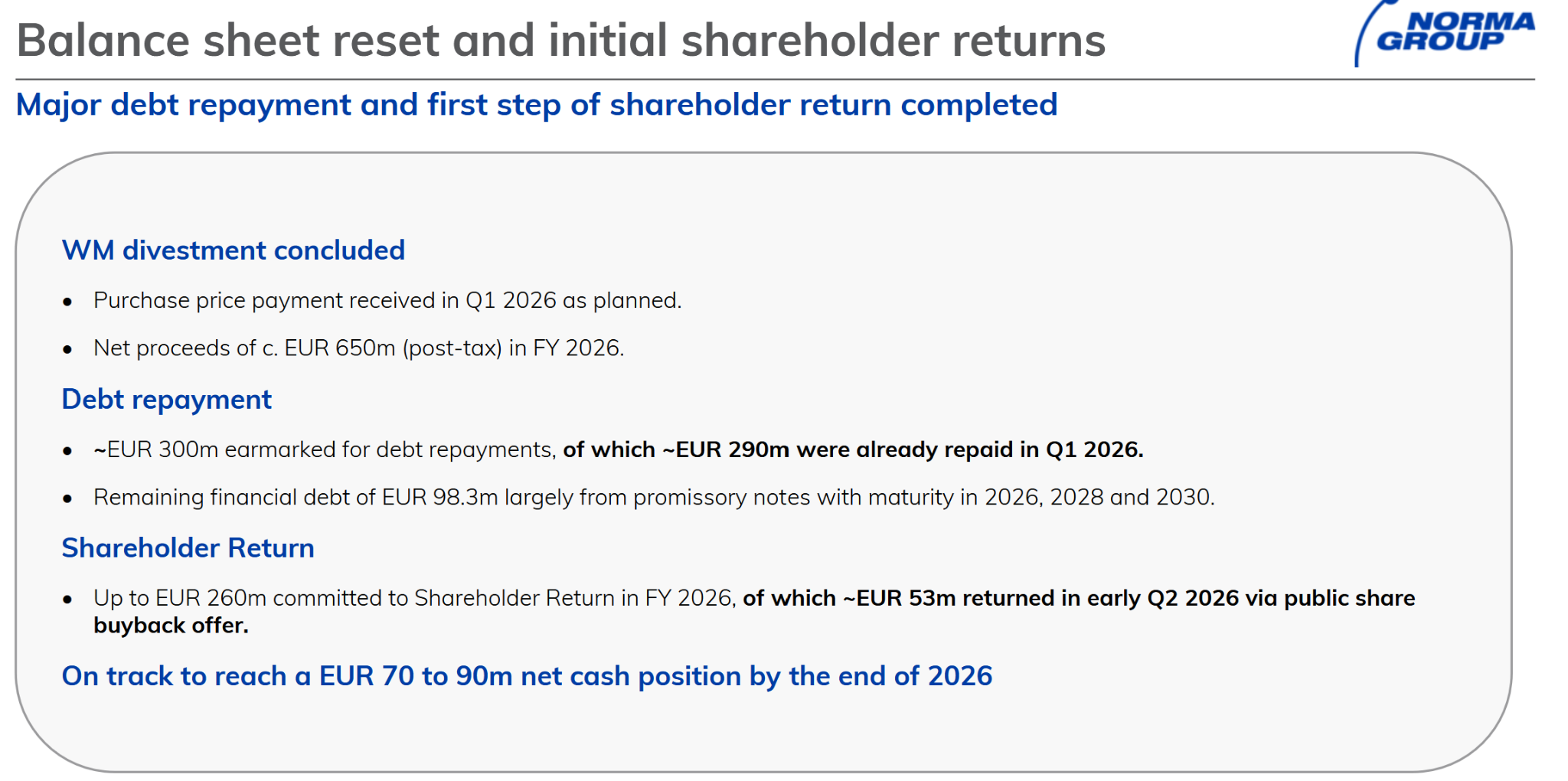

The latter, Water utility enterprise was bought for 850 mn EUR of which 650 mn EUR landed as Money on Normas Steadiness sheet. By some means they appear to have structured that deal very badly as they needed to pay plenty of tax which is uncommon.

Norma mentioned that they already paid again most of their debt and can preserve 70 mn for investments into the remaining enterprise and use the remaining to purchase again shares.

They already made a buyback tender supply of 10% in February at a value of 16,59 EUR.

Right here is the overview from the Q1 presentation:

Nevertheless, that solely partially resolved the Extra Money drawback which leads us to this

The particular state of affairs: A 30% (plus) buy-back tender at a (as much as) 30% premium

Three weeks in the past, Norma introduced a 208 mn EUR share repurchase tender at a premium of “10% to 30%” to a sure reference value.

Underneath German company legislation, on this case the AGM has to approve this choice earlier than the board can formally problem a young supply. The AGM will happen on July 1st in Frankfurt.

Trying into the detailed doc (which is the invitation to the AGM, TOP 10 plus the Supplementary Doc): We already know the next:

- The lengthy cease date for each, the acquisition and the cancellation of the shares is February twenty seventh 2027

- The purchase again premium shall be between 10% and 30% (the administration board has signaled that they’re going for 30%) in comparison with a sure “reference value”

- The overall quantity that shall be spent is 208 mn EUR in any case

- Shareholders will obtain a dividend of 0,14 EUR after the AGM in any case

- That reference value is outlined as follows

Initially I assumed that this was referring to the date of the preliminary board decision,which might have translated right into a reference value of 15,62 EUR, however after an in-depth dialogue with Gemini, I believe it’s the 90 day interval prior to truly publishing the supply.

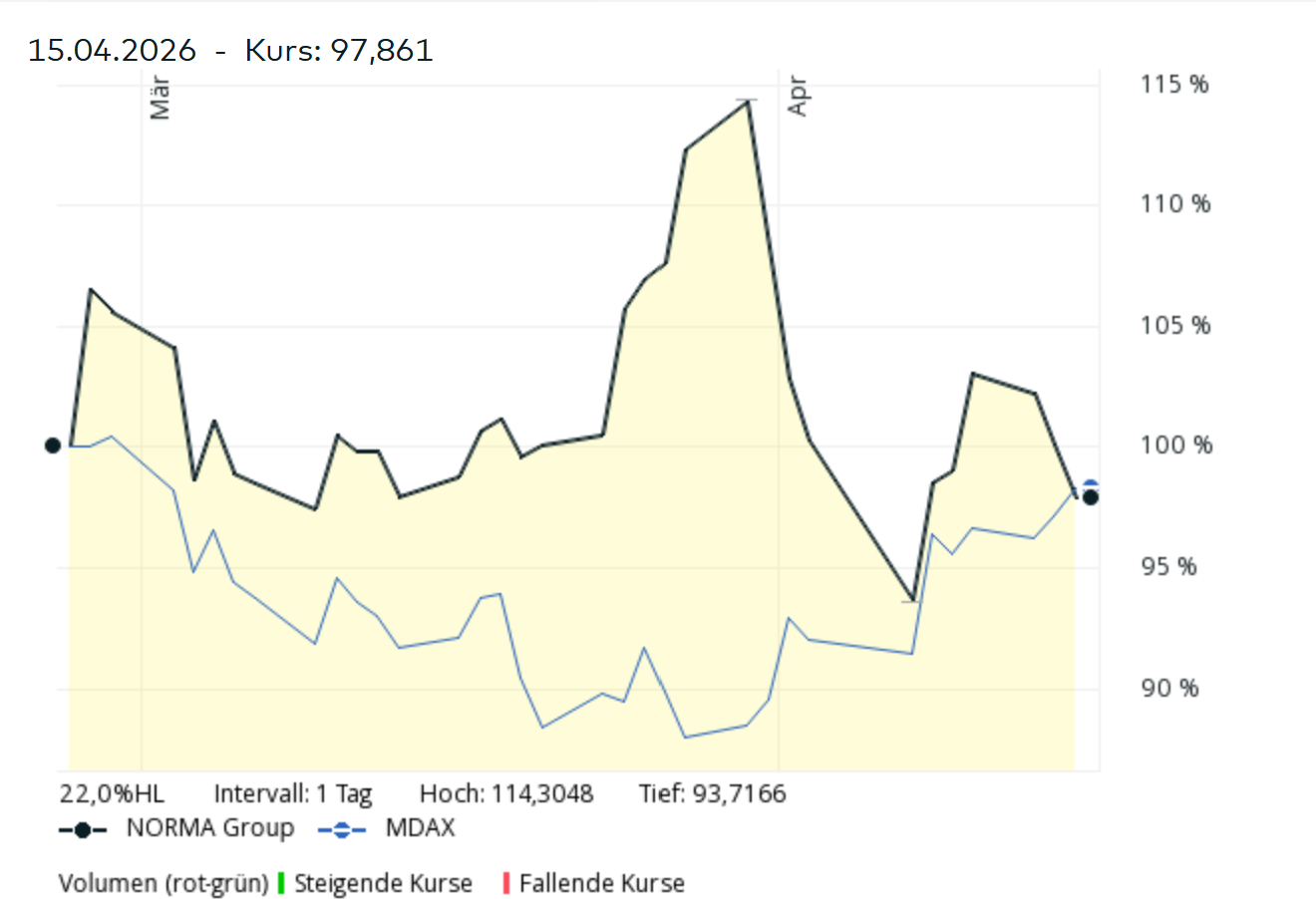

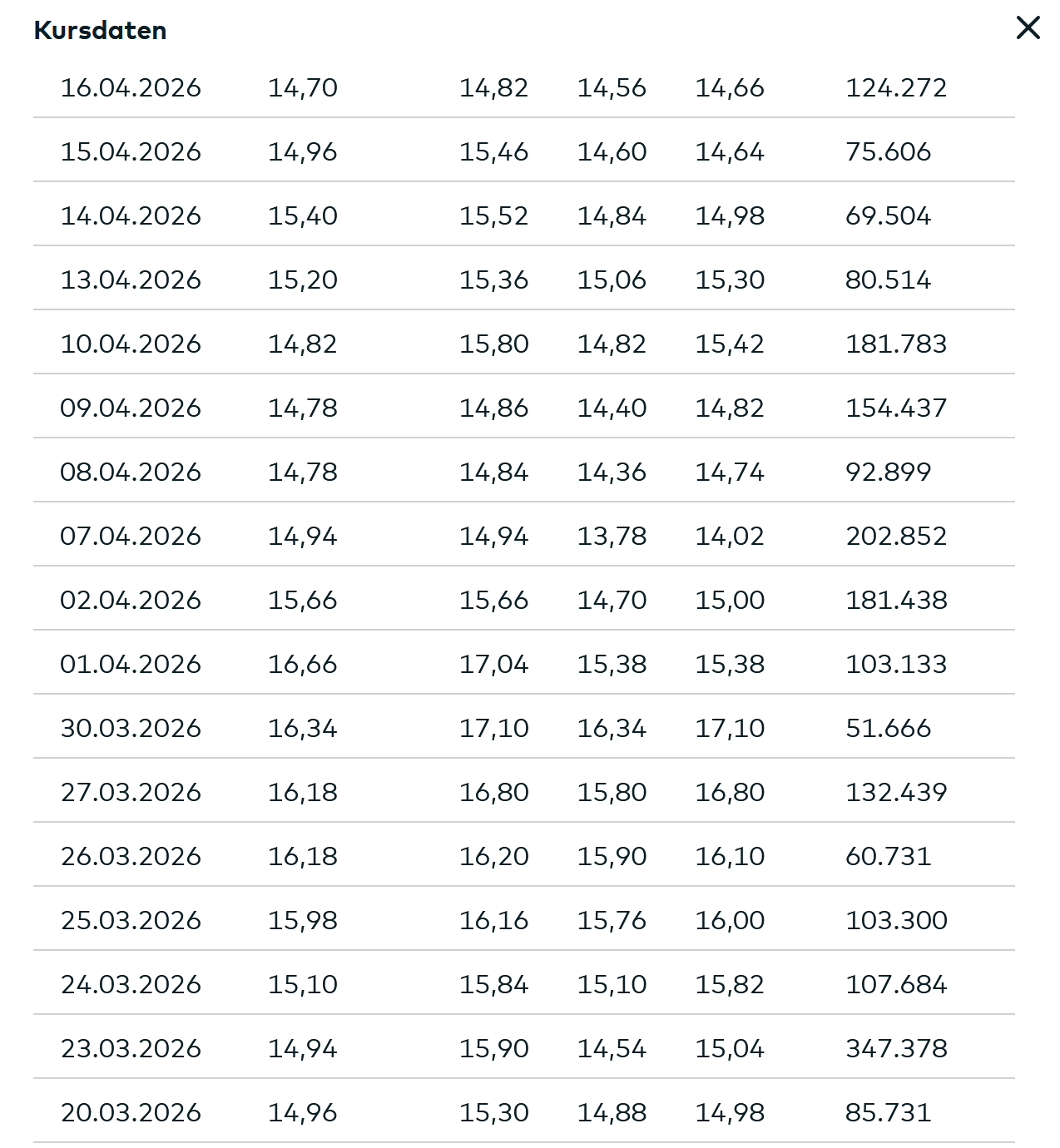

On the time of writing, the present 90 day common of Xetra closes is 16,09 EUR and rising so long as the share value is on the present 17 EUR as we are able to see on this chart:

- That the higher cap of the buy-back value is 20,87 EUR which is a “honest worth” estimate by the Administration

That is how this has been derived:

The Administration Board has subsequently, in preparation for the Capital Discount proposed to the Annual Normal Assembly, commissioned a valuation of the Firm in accordance with the IDW S1 normal as at 31 March 2026. This valuation resulted in a mean worth of EUR 20.87 per NORMA Group Share as at that date.

Trying again: How did the primary tender supply in March work out ?

In March, Norma made a buyback tender for 16,59 EUR per share for as much as 10% of the overall share capital.

This was launched on February twenty sixth 2026. The closing value the day earlier than was 14,92 EUR per share, so ~10% premium. The supply interval ran from Feb twenty seventh to March twenty seventh.

Curiously, 18,1 mn shares or round 57% of all shares had been tendered, which is rather a lot for such a small tender with a comparatively small premium. As solely 10% of the shares had been obtainable, solely 17,6% of the tendered shares had been purchased again. We are going to take a look at this later as soon as once more.

Curiously, as we are able to see within the chart, the share value reached a excessive of 17,10 EUR on the day after the top of the tender interval. One week later, on April seventh, the share value reached a low of 13,78 EUR, round -20% vs. the tender supply value:

Possibly that needed to do with the discharge of the 2025 numbers on March thirty first and the information that the CEO would step down.

The present Tender: What we don’t know

As I’ve outlined above, we all know sure issues in regards to the tender already, however not all the things. The primary variables that we don’t know are as follows:

- What would be the final premium & share value at which the tender will happen ?

Though they state that the buyback will occur at a variety of between 10-30% above the reference value, sure wordings point out that they’ll go in direction of the excessive finish. Essentially the most telling signal is the wording within the complement to the AGM invitation

“The worth clause described in part 2.2 permits the Administration Board to supply shareholders a repurchase value nearer to the intrinsic worth of the share.”

For me, it is a very sturdy indication, supported by their largest shareholder, which is able to be part of the Supervisory board, that they’ll goal for the higher finish of the vary or near their “honest worth”.

Simply to point out the numbers:

With 16,09 as reference value, the low finish of the vary can be 17,70 EUR per share, whereas on the excessive finish can be 20,87 (capped by the “Truthful worth”).

- What would be the acceptance fee of the tender ?

If we assume the 20,87 as the last word tender value, this could translate into 208 mn/20,87 EUR = 9,97 mn shares which represents 31% of all shares or ~35% of all shares ex present treasury shares.

So if all shareholders tender absolutely, the minimal acceptance fee for each shareholder ought to be 35% (round 2x the acceptance fee from the primary supply)

One other assumption is that Teleios, the 17,15% shareholder, won’t wish to decrease their stake once they concurrently be part of the board. So if we assume that they tender solely 35% of their shares, we are able to assume that one other 17,15-(0,35*17,15%)=11,2% of shares won’t be tendered for certain.

This interprets right into a “worst case” acceptance fee of round 40% for the situation with the utmost buy value.

Alternatively, it is usually very possible in such circumstances that not everybody tenders. I’ll clear up this problem by creating a number of situations and weighting them with my subjective chances. Extra on this later.

- At what value will one be capable to promote the shares that aren’t accepted within the tender

That is clearly a tough one, however it is usually essential to assume that one so as to have the ability to calculate an anticipated return for this particular state of affairs.

My assumption right here is that one ought to not less than get the present reference value of 16,09 EUR per share. I’ll share some ideas on the potential worth of the “stub” on the finish of this submit.

- Precise timing of the supply

To be sincere, I’m not 100% certain how briskly they’ll execute after the AGM approval. There is likely to be some regulatory necessities (entry into the corporate registry) or perhaps a number of the regular suspects will attempt to blackmail the corporate with authorized challenges.

However my assumption can be that the tender supply interval begins in August and shall be concluded in September. So from as we speak, the time required for this to totally play out shall be 3,5 to 4 months.

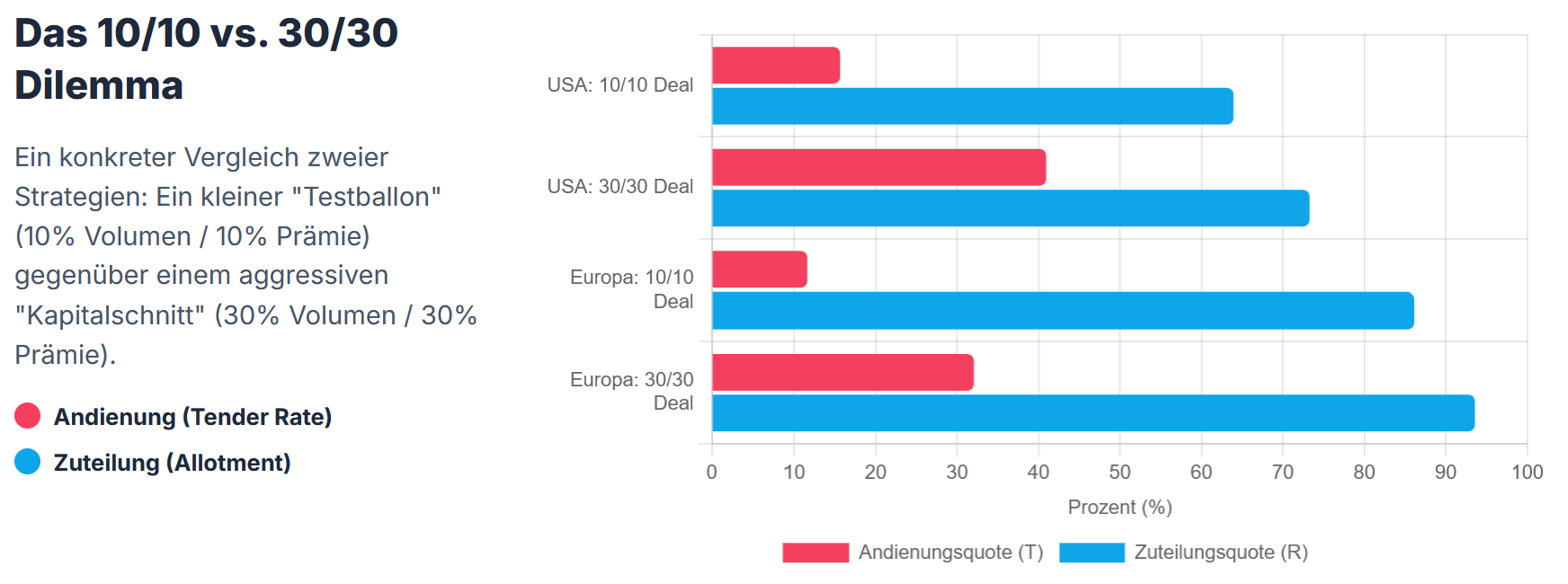

AI tour: Analyzing the potential tender fee and ensuing Acceptance fee

One important factor that one must estimate is the proportion of shares that can really be tendered. I’ve talked about to start with, that within the first tender, 57% had been tendered with solely 10% obtainable, leading to a comparatively small acceptance share of 17,6%.

Based mostly on empirical proof, a better premium will increase the tender fee, however a much bigger tender dimension relative to the excellent shares will increase the acceptance fee.

I requested Gemini to investigate tenders from the previous years and estimate a regression. Curiously, tender ratios are sometimes fairly low and acceptance charges a lot larger than one would usually suppose.

That is what Gemini estimated for a 30% Tender with a 30% Premium vs. a ten% Tender with a ten% premium each, within the US and Europe:

In response to their regression, a 90% Acceptance/Allotment ought to be anticipated and solely 30% of shareholders would tender. Now this sounds to good to be true and the primary tender of Norma earlier appears to have been already a transparent outlier.

So taking a look at historic information clearly helps however in any case one has to make one’s personal assumptions for this case.

Total; I do like to make use of AI fashions as a sparring companion particularly in these Particular Conditions. Though one must get used to its “cocky” behaviour, I do suppose the discussions and extra evaluation enhance the method and hopefully, in the long term over many transactions, the result.

Return estimation primarily based on a 30% premium to the reference value:

So now we have now all the things to estimate an total anticipated return, in fact primarily based on all of the assumptions I described above.

Right here is my return estimate primarily based on the 30% premium (capped at 20,87 EUR) and on a present share value of 17 EUR (together with the dividend and 16,09 promoting value for not tendered shares):

So 13,3% “anticipated return” over 3,5-4 months shouldn’t be too dangerous given the present 2,25% quick time period rate of interest in EUR.

In fact that is primarily based on my assumptions that I’ve laid out above and completely different assumptions result in completely different outcomes.

Lots of the uncertainties will go away over time reminiscent of:

- The AGM will happen on July 1st. After the AGM we’ll know if somebody desires to play video games with the tender supply or not and the way a practical schedule will appear like

- As soon as, the authorized necessities are met, the administration will formalize the supply and we’ll then know the precise premium

- Lastly, after the top of the tender interval, we’ll know the ultimate acceptance fee after which additionally the share value for the shares that may not be tendered

What occurs on the low finish, a ten% premium ?

This is able to in fact be much less engaging however one wants to contemplate the next: Norma intends to spend the complete 208 mn, so the idea right here can be that they purchase again extra shares and the acceptance ratio will go up. The minimal acceptance can be 47%.

Additionally, there can be extra worth for the stub, however I’ll stick to the 16,09 EUR as promoting value for the non-tendered shares. The likelihood of the acceptance charges additionally must be adjusted upwards.

Based mostly on these assumptions. my return expectation seems to be as follows:

So on the low finish which is mainly virtually the worst case, I might have a return of ~2% primarily based on a present share value of 17 EUR. Solely within the worst case, when mainly everybody tenders, there can be a small loss.

So primarily based on my assumptions, the state of affairs seems to be like a reasonably low cost “possibility” on a probably larger acceptance ratio.

Some ideas on the “Stub”:

If we assume that the tender will get by and that the shares will return to 16 EUR per share, we can have an organization that has round 18,7 mn Shares excellent at a market cap of 18,7*16= 300 mn EUR in the event that they pay the 30% premium

They plan to have a web money place of 70-90 mn EUR by the top of 2026 in response to their Q1 presentation, so EV can be between 210 and 230 mn EUR.

For 2026, Norma expects 820-830 mn EUR in gross sales and a 2-4% “adjusted EBIT margin” which might translate into ~16-35 mn in “adjusted EBIT”. On the midpoint, this interprets to 25 mn adjusted EBIT or an EV/Adjusted EBIT a number of of 8,4-9,2x.

Within the case of a ten% premium and a 16 EUR share value, the market cap can be ~270 mn EUR and EV/EBIT between 7,2-8,0 x EV/EBIT.

Not “grime low cost” however not costly both. Within the second half of 2026, they plan to current a “2028 technique”.

I believe regardless of the comparatively unexciting enterprise, the valuation of the stub is reasonable sufficient that I believe that from a basic aspect, the draw back threat is proscribed to a sure extent after the execution of the tender. In fact, if there may be an total market crash, nobody cares about fundamentals anyway.

One vital level right here: In the meanwhile, I’m not planning to guess on a turn-around.

For me it is a Particular State of affairs funding and I’ll exit as soon as the tender is settled.

Technicalities:

That is an fascinating element from the invitation to the AGM

To the extent technically doable with cheap effort, tender rights buying and selling (Andienungsrechtehandel) is to be established.

The shareholders’ declarations of acceptance are taken under consideration in response to shareholdings by tendering the tender rights attributable to the shareholding in addition to any further tender rights acquired from different shareholders.

So which means there is likely to be a mechanism that just like a capital enhance with subscription rights, on this case the tender rights is likely to be cut up of from the shares and traded individually.

I haven’t seen this earlier than and if that is carried out, it may create a particular state of affairs in itself, if these rights may commerce larger or decrease than the intrinsic worth. So from that perspective there is likely to be an extra “possibility” to enhance the result

Timing possibility

As we have now seen within the instance of the fist tender, through the official tender interval, the shares had already approached the tender value. Relying on how that is structured, I’ll undoubtedly make sense to tender somewhat late as a way to preserve the choice of promoting the shares at a good value earlier than the execution of the tender.

If we have now separate tender rights, then the chance shall be principally in analyzing the tender rights as talked about above.

Abstract:

On the present value of 17 EUR, I do suppose that the upcoming tender supply of Norma Group provides a good return to park some money for 3-4 months at an anticipated (likelihood weighted) return of 13% (not annualized).

Even on the low finish, beneath my assumptions one would be capable to make a 2% revenue and the very worse case would end in a small loss (lower than 1%).

For a particular state of affairs, I believe there may be additionally plenty of further optionality baked into this entire course of which for my part outweighs the uncertainties.

There are nonetheless a few shifting elements and the tender is somewhat advanced, so my total allocation to that is somewhat small at 3% of the portfolio.

I’ll watch this very carefully and I would enhance the place if the worth goes down or if new constructive data is available in and the worth stays low.

What I do like is that the dangers are very particular and never a lot correlated to the general market, which makes it engaging for the “alternative” a part of the portfolio.

I suppose that additionally the complexity of the supply creates a chance right here.

DISCLAIMER: This isn’t funding recommendation. The creator may personal, purchase or promote shares with out advance discover. The assumptions is likely to be flawed or outright mistaken. PLEASE DO YOUR OWN RESEARCH !!!!