Administration Abstract:

On this put up, out of pure self-interest, I seemed somewhat bit deeper into Terry Smith’s controversial 6M Fundsmith report and deal with the “Energetic vs. Passive” debate, how Fundsmith’s Buys and Sells look below my very own Momentum scoring and a few ideas on adjustments in funding administration types.

Intro & Background

Terry Smith, the outspoken Boss of UK “High quality Worth” Fund Supervisor Fundsmith dropped a fairly sudden 6M letter to buyers the place he principally communicated a fairly drastic pivot in comparison with what he stated over the previous 15 years.

In an “unprecedented” transfer, he switched ~50% of the portfolio inside 6 months which could be very uncommon for his fund. In earlier years, annual turnover of the portfolio was on common lower than 10%.

His mantra of “do nothing” was repeated in each letter and sometimes repeated in his talks.

In the newest letter, he blames, as a number of instances earlier than, “passive ETFs” for market distortions and claims that these energetic managers which can be at present profitable are almost certainly “momentum chasers”.

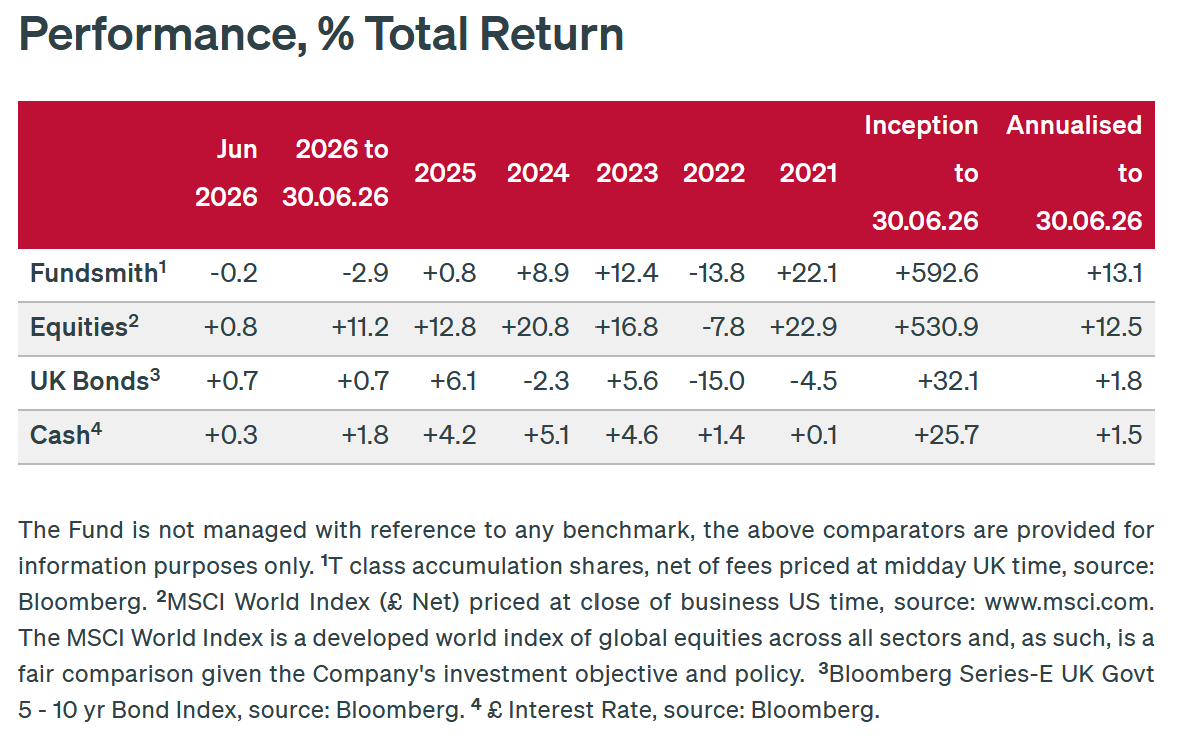

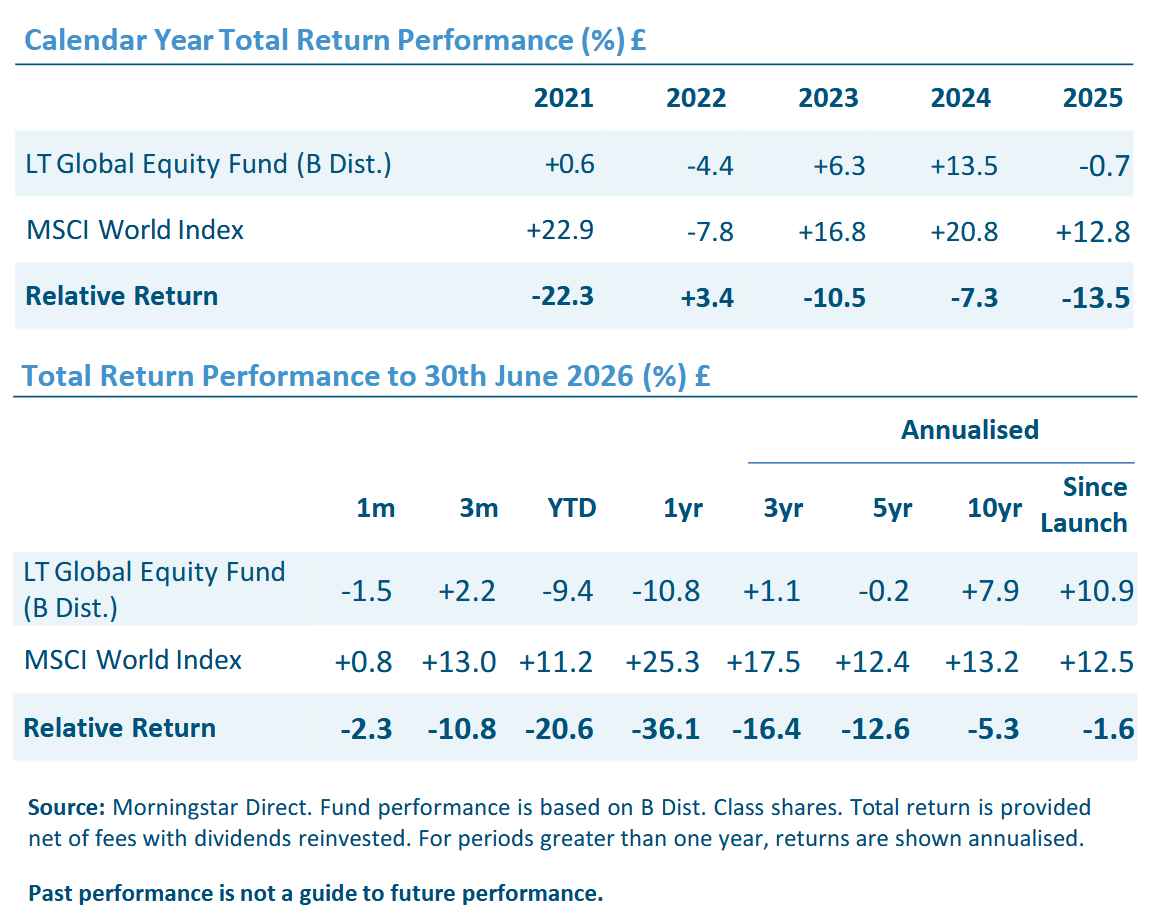

Fundsmith to be clear is just not the worst energetic fund. With a TER of ~1% they’re additionally not on the extraordinarily costly facet and since inception, the observe report continues to be fairly okay. Nonetheless, a fast have a look at his latest fund factsheet exhibits that for the previous 4 ½ years, the fund underperformed the MSCI World fairly drastically:

He underperformed each, in up markets and within the down yr 2022. So it’s clearly not a “low vol” impact.

However I discovered that letter fascinating because of the following elements wherein I’ll dive somewhat bit extra:

- Energetic vs. Passive

- Smith’s one way or the other inconsistent remedy of “momentum” which is an element I’ve been paying extra consideration to since a while now

- The query of the right way to typically shift/pivot/adapt an funding technique (if in any respect)

- Energetic vs. Passive

I truly learn the Substack put up that Terry Smith referenced which might be discovered right here:

It summarizes fairly nicely the overall view from many energetic managers why an excessive amount of index investing could be very harmful and may finish in a complete collapse of the inventory market. Whereas there may be a (smallish) chance for this state of affairs, it sounds somewhat bit like the standard “Outdated man shouting to the clouds” cartoon.

Alternatively, the article additionally doesn’t actually cowl that as a complete, Energetic Administration simply has by no means actually justified its fairly vital value.

Within the “good outdated instances”, energetic funds had been the gate keepers between particular person buyers and the inventory market with the one different being inventory brokers.

Lately nonetheless, the convenience of shopping for an ETF and the low value is clearly a really enticing worth proposition in comparison with “classical” funds the place usually nonetheless an middleman is clipping an extra payment (and or the financial institution).

Within the US, the biggest marketplace for funds globally, ETFs on the whole are additionally considerably extra tax environment friendly than (energetic) Mutual Funds.

Solely claiming that there will likely be Doom with too many passive constructions is just not so convincing and fairly seems to be like an try and scare regulators in defending the nonetheless very worthwhile enterprise of underperforming asset managers and wealth advisors.

For my part, as of late an energetic supervisor actually must have a extra convincing story than simply that one from Mr. Evan-Cook dinner. Your actually need to supply one thing to buyers that they’ll’t get via low value Index ETFs which isn’t really easy.

Only a few days in the past, FT Alphaville tried to debunk one other narrative: That if there are just a few energetic managers left, there will likely be an enormous bounty for these remaining managers.

They argue that the other is true: Because the remaining ones are the good ones, there will not be sufficient “patsies” to make the “massive hay”:

In any case, it will likely be fascinating to see how the energetic vs. passive debate continues, however there received’t be a magic turnaround any time quickly in my view. Index ETFs are right here to remain and the Energetic Administration business actually wants to seek out methods to create precise worth for buyers not directly.

2) Momentum

Within the letter, it nearly appears that Terry Smith has written components with out trying on the entire “enchilada”.

On web page 3&4 he exhibits a chart that Momentum is dangerously excessive as final seen in 1999 earlier than the Dotcom Increase. After which, just a few pages later he writes the next:

We are going to take extra account of momentum — each elementary and share worth — in our funding selections. Particularly, we will likely be a lot much less keen to deploy the time-honoured method of shopping for high quality firms once they hit a glitch

As a few of my readers may keep in mind, I did begin to embrace momentum into my resolution course of a yr in the past. However in a much less drastic method than Terry Smith and extra “gradual”.

In my complete Scoring system, Momentum is mirrored by 4 indicators as a part of an general rating that additionally contains “High quality” and “Valuation”:

For “momentum” my crude evaluation seems to be as follows:

- Present EPS momentum (i.e. EPS LTM is larger than the earlier yr): 1 Level if Sure, 0 in any other case

- Inventory worth is above the 200 day shifting common 1 Level if Sure, 0 in any other case

- The inventory worth efficiency of the final 6 Months (1 Month lag) is optimistic or destructive (1 Level of Efficiency is > +5%, -1 level if Efficiency is <-5%, 0 factors in any other case)

- The inventory worth efficiency of the final 6 Months (1 Month lag) is optimistic or destructive (1 Level of Efficiency is > +5%, -1 level if Efficiency is <-5%, 0 factors in any other case)

So general, my “momentum rating” can go from minimal of -2 to a most of +4 inside a complete rating that may attain, together with High quality and Valuation, scores a complete rating of 18.

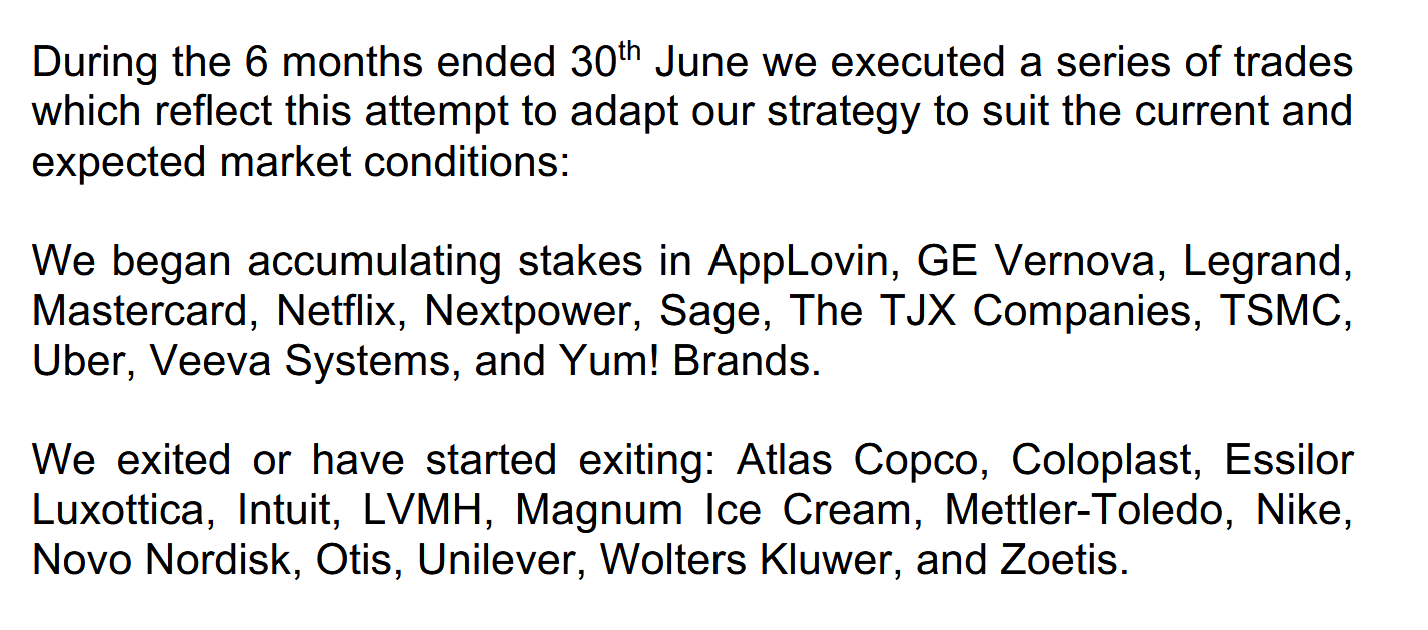

So for enjoyable I simply tried to attain the shares that Fundsmith bought and acquired. Right here is Terry’s abstract:

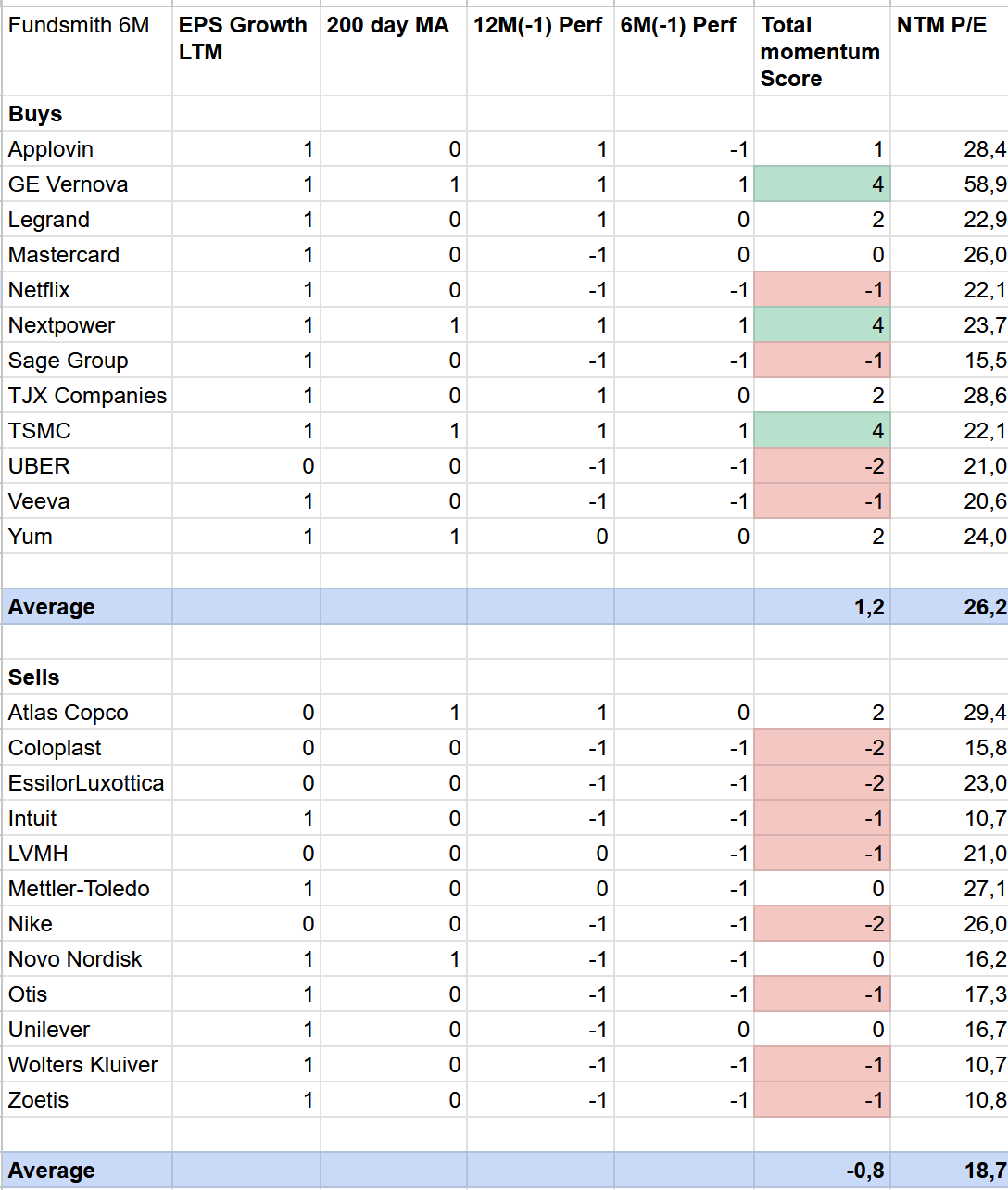

And right here is the desk scoring Terry’s shares, each, the buys and sells with my crude momentum measure:

Two issues stand out in mixture:

The shares that he bought, on common, look certainly worse from a momentum perspective than those he purchased. And the shares he bought are loads cheaper than those he purchased.

It’s additionally fascinating that solely 3 of the shares he purchased would get a most Momentum rating in my system (GE Vernova, TSMC and Nextpower). Among the shares have fairly destructive Momentum below my definition (Uber, Netflix & Veeva).

It’s additionally apparent that he needed to have some publicity to the Datacentre /AI theme through TSMC, GE Veronica, NextPower, Legrand and possibly UBER.

Total it seems to be to me that he nonetheless focuses on fundamentals however seems to be for extra “optimistic elementary momentum”.

One query I’ve been asking myself is why he didn’t promote a few of these shares earlier. One instance which I’ve seemed into below one other context is Essilor Luxottica. Right here is the chart of the implicit NTM PE over the previous 10 years:

We will see that till the top of 2025, the inventory was valued at 40x NTM P/E, far above the typical.

If we have a look at the margin and Return on Capital ratios over time we will see that after the merger between Essilor and Luxottica, margins by no means recovered there earlier stage and Return on Capital was a miserable mid single digit.

That begs the query why you’d wish to personal such a inventory at such a valuation within the first place.

Anyway, Terry Smith clearly now needs to keep away from “unloved” shares and is trying to make investments extra into shares that do at the least from a elementary perspective nicely, even when the brand new shares are on common considerably costlier than the bought ones.

With such an method, in my view, his “do nothing” mantra received’t work, as a result of within the present setting, fundamentals can change ven extra rapidly than earlier than.

Will probably be fascinating to see if and how briskly he’ll flip over his portfolio going ahead.

3) If and the right way to shift/pivot/adapt an funding technique

One “peer” to Terry Smith is Nick prepare from Linsell Practice funds who has an analogous “high quality centered” method. In his 6M letter (International Fund) nonetheless, he’s fairly including to his losers than promoting them. One distinguished instance is Intuit:

However shopping for a consensus AI loser inventory right this moment doesn’t imply arguing no danger from AI (or anything we haven’t but seen coming). It means taking a calculated danger, primarily based on

probability and the trade-off with worth, and accepting the emotional discomfort of showing unconventionally improper. To provide a pertinent instance, Intuit was simply the Fund’s worst performer in June, declining 21% in USD phrases, down now practically two-thirds from final yr’s highs. While 2025’s valuation was arguably steep at a c.2.5% free money circulation yield, the collapse to what’s now over 10% feels egregious. As above, we expect it seemingly that the prior

bullishness resulted from the overall extrapolation of previous successes – with, it should be stated, some justification: Intuit has grown revenues organically at double-digit charges yearly this decade, while its EPS is up 4.5-fold versus FY2016. However the ahead bearishness, predicated we assume on acute (however sometimes unsupported) fears of AI disintermediation, feels disproportionate. The non-GAAP a number of on subsequent yr’s EPS (which administration nonetheless information to develop at c.16-18%!) is now right down to 11x. To attain a standard nominal return (say the US market’s historic 9% p.a.) now implies destructive ahead earnings progress. As little as a yr in the past, analyst debate centered on whether or not Intuit might sustainably hit 20% income progress versus the prior mid-teens charges

I believe the Nick Practice vs. Terry Smith “contest” is an fascinating case examine on the deserves of fixing your funding method abruptly.

One wants to say that Nick Practice’s observe report for this fund is even worse than Terry Smith’s, underperforming the MSCI World by a fairly broad margin since inception in 2011:

Total, I believe in each lengthy funding profession, it will likely be essential to vary and adapt one’s method to funding to be able to keep related.

Probably the most well-known instance right here is Warren Buffett who modified his method essentially at the least 2 instances. From Graham Deep Worth to High quality to “Full scale take-over conglomerate” investing. Along with his preliminary method, he would by no means had been in a position to attain the scale that he has reached right this moment. The identical with listed-minority investments on the whole.

From what I’ve seen, a speedy improve in AUMs for any supervisor is usually ultimately way more a curse than a blessing. Sure, you earn much more charges however until a supervisor considerably adjusts the technique, returns will endure after a sure improve nearly inevitably.

The query is clearly how to do that in a method that doesn’t create confusion on the investor facet and is hopefully constructive for the longer term outcomes.

In Terry Smith’s case, I’m struggling somewhat bit together with his earlier mantra that “do nothing” is the one and solely factor after which abruptly change that inside a 6 month interval. My feeling would have been that he ought to have toned down the language somewhat bit earlier already, until he actually did this pivot on brief discover.

In Nick Practice’s case, doing nothing (or not a lot) after now being down since inception is possibly additionally not 100% optimum.

For lots of institutional buyers, 3 years are possibly the utmost they’ll tolerate underperformance earlier than they pull the set off. Each Fundsmith and Lindsell &Practice are clearly previous that mark.

From my perspective, each energetic fund supervisor ought to notice that luck is an enormous a part of the sport and when issues are good, one ought to give some credit score to good luck as a substitute of claiming all of the outperformance as a consequence of superior abilities. I assume which may make issues somewhat bit simpler when inevitably issues don’t look so nice.

In any case, I do suppose {that a} shift in technique must be ready and executed together with related and documented adjustments in course of and likewise personnel.

What you clearly additionally want is a few endurance. Don’t anticipate {that a} structural change will enhance efficiency on day one. It will want time.

In any case, as talked about above, Energetic Fairness Administration is dealing with a whole lot of headwinds any method, which makes it much more tough to dig your self out from an “efficiency gap”.

Abstract:

It’s clearly too early to inform if and what we will study from Terry Smith’s latest actions, however on the floor they give the impression of being somewhat bit like a “panic transfer”.

Going ahead, Lindsell & Practice will likely be a very good comparability as a result of they appear to maintain doing what they’ve been doing and are even doubling down on their losers.

In any case, for me personally it is clearly some form of proof that utterly ignoring “momentum”, being elementary or purely inventory worth pushed is just not a good suggestion. “Do nothing” in my view is tougher than ever and possibly not the dominant technique going ahead. For my part, utilizing momentum as an extra think about inventory selecting and portfolio administration can clearly enhance the method to a sure extent.