Frosta

Frosta, the German “Hidden frozen Meals champion” that I wrote up in February already launched 6M outcomes this week.

Highlights:

General gross sales quantity improve by +11,7%. simply beating the market which was round +3%. The true kicker is that the Frosta Model itself grew by +25% and appears to be additional accelerating.

Amongst different issues, Frosta has launched two new traces of frozen meals: “Excessive Protein” meals with extra meat and “a la carte” restaurant high quality meals. Each new traces are at a barely increased priced level than the unique.

I discover this a intelligent technique, to not improve the costs of their basic vary however quite supply even higher meals at a better worth level.

After tax revenue solely elevated by 2,4%. Gross margins elevated a little bit from 48,3% 6M 2025 to 48,8% in 6M 2026, internet revenue margin declined barely from 5,5% to 4,9%.

Nevertheless, the outlook for the complete 12 months is VERY constructive.

If we take the 2 midpoints, 13% gross sales improve and 6,5% internet margin, we might find yourself at 50 mn EUR internet revenue or an EPS of seven,35 EUR.

Contemplating that Frosta has ~10 EUR Web money Money per share, this interprets into 13x P/E for a strongly rising firm that’s executing extraordinarily nicely.

If we simply examine this with the self proclaimed “Main European Frozen Meals” firm Nomad meals, we will clearly see from whom Frosta is taking market share:

As all the time, Traders weren’t impressed very a lot:

I used nevertheless the chance to extend my Frosta place from 3,2% to 4,5%. And I’ll maintain shopping for if the share worth stays beneath 100 EUR.

Forsta is in my view one in all these typical “Peter Lynch” investments: As a german, you’ll be able to simply go right into a grocery store, look how empty the Frosta Shelfs are and purchase your self a number of packs to check the standard you get for the quite reasonable worth.

Paypal

In March I wrote about Paypal and simply discovered it “too arduous” for me, given my restricted data within the Cost sector.

Even again then, the rumor was that Stripe is likely to be involved in Paypal however I discovered it not likely sensible as there was a restricted match:

Now the Stripe hearsay has resurfaced however with an fascinating “twist”: Stripe and PE big Introduction (100bn AuM) appear to have teamed up provided 60,50 USD per share for Paypal, however the Paypal Board appears to have rejected that bid as too low.

The share worth jumped to round 57 USD, leaving solely a 5-6% unfold. which signifies that some arb gamers appear to count on and worth in an elevated supply.

As it’s fairly early within the course of, I’ll maintain watching this. If the worth goes down a bit and we might see a variety nearer to 10%, this could possibly be a probably fascinating particular state of affairs.

From a structural perspective, teaming up with Introduction makes plenty of sense for Stripe as a result of then they will select precisely the elements that they like and Advents monetizes the remainder.

Introduction additionally simply has closed fundraising for its eleventh flagship fund with a complete of 26 bn USD in Commitments, in order that they do have some respectable firepower.

Easyjet

Speaking about elevated supply: On June twenty ninth, I had written about Castlelake’s try and take over Easyjet. Again then the inventory was buying and selling at 5,72 GBP and Castelake had elevated its bid to six,50 GBP.

On July fifth, Easyjet approved then an elevated supply of 6,90 GBP. And solely 2 days later, all of the sudden Apollo confirmed up with a 7,15 GBP bid.

Easyjet’s board shortly supported that supply and Apollo has now time till August seventh to give you a proper bid.

So shopping for Easyjet again then would have been a good suggestion, however the Apollo transfer was clearly not simple foreseeable.

Apparently, the unfold this time could be very small, so it appears market members predict a better counterbid from Castlelake.

Generally, the UK market appears to be working sizzling with takeovers, Rotork/ABB is one other instance.

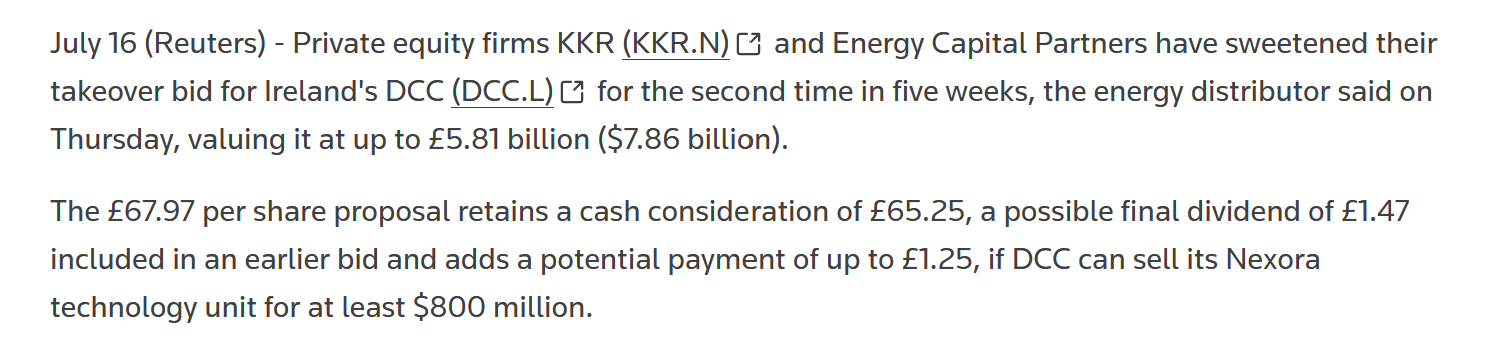

DCC

Lastly a small replace to DCC: OkKR and DCC have now added a “Sweetener” to the deal: If DCC manages to promote its US Audio distribution enterprise, shareholders will get an additional 1,25 GPB per share:

July twenty seventh is now the brand new cease date for KKR to formalize the bid.