A central use of reserves held at Federal Reserve Banks (FRBs) is for the settlement of interbank obligations. These obligations are substantial—the typical every day whole reserves used on two major settlement techniques, Fedwire Funds and Fedwire Securities, exceeds $6.5 trillion. The entire quantity of reserves wanted to effectively settle these obligations is an lively space of debate, particularly because the Federal Reserve’s present quantitative tightening (QT) coverage seeks to empty reserves from the monetary system. To raised perceive the usage of reserves, on this put up we study the intraday flows of reserves over Fedwire Funds and Fedwire Securities and present that the mechanics of every settlement system end in starkly completely different intraday calls for on reserves and differing sensitivities of these intraday calls for to the overall quantity of reserves within the monetary system.

Background

As a part of the conventional course of enterprise, banks settle obligations amongst themselves by drawing upon reserves they maintain on the FRBs. For cash-only obligations, banks most frequently use the Fedwire® Funds Service, a large-value real-time funds system. The entire every day worth of transfers remodeled Fedwire Funds is substantial, with the typical every day worth despatched within the second quarter of 2024 equal to $4.5 trillion.

One other settlement system operated by the FRBs that makes use of reserves is the Fedwire® Securities Service, a real-time delivery-versus-payment system. This technique is linked to the FRBs’ book-entry ledger, on which the U.S. Treasury, Fannie Mae, Freddie Mac, and different businesses subject securities. Amongst different companies, Fedwire Securities allows the simultaneous motion of securities towards reserves throughout accounts. There’s additionally a considerable every day motion of reserves over Fedwire Securities, with the typical every day worth of reserves delivered within the second quarter of 2024 equal to $2.1 trillion.

For each settlement companies, banks normally provoke transactions on behalf of their clients. These clients, or the underlying nature of the transaction, can dictate that the transactions be accomplished by sure deadlines inside the day. The intraday move of reserves out and in of a financial institution’s account, nonetheless, could be fairly giant relative to a financial institution’s steadiness. A earlier Liberty Avenue Economics put up confirmed that in 2015, a 12 months of ample whole reserves, the biggest ten banks nonetheless confronted outflows over Fedwire Funds (alone) that had been bigger than their beginning-of-period steadiness on the FRBs. Banks then, usually must strategically handle the timing of transactions over each settlement techniques, balancing the calls for of their clients for earlier settlement inside the day towards the financial institution’s steadiness of reserves on the FRBs (and the financial institution’s urge for food to entry intraday credit score from the FRBs).

What Is Every System’s Intraday Liquidity Calls for?

Fedwire Funds is designed to accommodate solely credit score funds, so the account holder sending reserves initiates the switch. Accordingly, when an account holder’s steadiness is working low, that financial institution usually strategically delays sending funds over Fedwire Funds till later that very same day, with the expectation that incoming funds will replenish that financial institution’s steadiness (see “Intraday Liquidity Administration: A Story of Video games Banks Play” and “How Considerable Are Reserves? Proof from the Wholesale Cost System”). Therefore, when a financial institution is dealing with a constraint on the reserves it’s holding inside the day, the financial institution is more likely to reply by delaying funds remodeled Fedwire Funds till later within the day.

Fedwire Securities is designed in order that the account holder sending securities (and receiving reserves) initiates the transaction. Provided that account holders worth holding reserves for intraday liquidity wants, even on the margin, the account holders that face obligations to ship securities for a given day will usually ship these securities as early as attainable.

These intraday calls for on reserves drive the distribution of transactions inside the day throughout every settlement service. The chart beneath reveals the p.c of whole transactions by worth that happen inside 1.5-hour buckets over the Fedwire Funds operational day (9 pm of the day earlier than to 7 pm of the present day, japanese time) for the second quarter for 2024. There’s an uptick in funds made with the opening of enterprise on the U.S. East Coast, however the busiest interval is from 3-4:30 pm. This late-day bunching of funds is in keeping with banks managing intraday liquidity calls for, an remark made in “Adjustments within the Timing Distribution of Fedwire Funds Transfers.”

Banks Settle Greater than Half of Fedwire Funds Transactions within the Final Third of the Day

% of every day whole transactions

Notes: The chart reveals the p.c of all every day transactions occurring in every 1.5-hour bucket over the Fedwire Funds operational day (9:00 p.m. of earlier calendar day to 7:00 p.m. of the present day, Japanese Time). The pattern is the second quarter of 2024.

Turning to Fedwire Securities, the next chart reveals the p.c of whole transactions by worth that happen over this settlement system’s operational day (8:30 am to three:15 pm, Japanese Time) within the second quarter of 2024. The principle takeaway is that greater than 60 p.c of whole transactions by worth happen proper on the opening of Fedwire Securities. As with Fedwire Funds, this habits is in keeping with banks valuing reserves for intraday liquidity. Moreover, the focus of settlement on the opening creates substantial calls for on reserves—within the first half-hour after opening, about $1.05 trillion of reserves, on common, are transferred over Fedwire Securities.

Most Fedwire Securities Funds Happen within the First half-hour after Opening

% of whole every day transactions

Notes: The chart reveals the p.c of all every day transactions occurring in every half-hour bucket over the Fedwire Securities operational day (8:30 a.m. to three:15 p.m. every day, Japanese Time). The pattern is the second quarter of 2024.

How Does the Intraday Timing of Funds Change with the Degree of Combination Reserves?

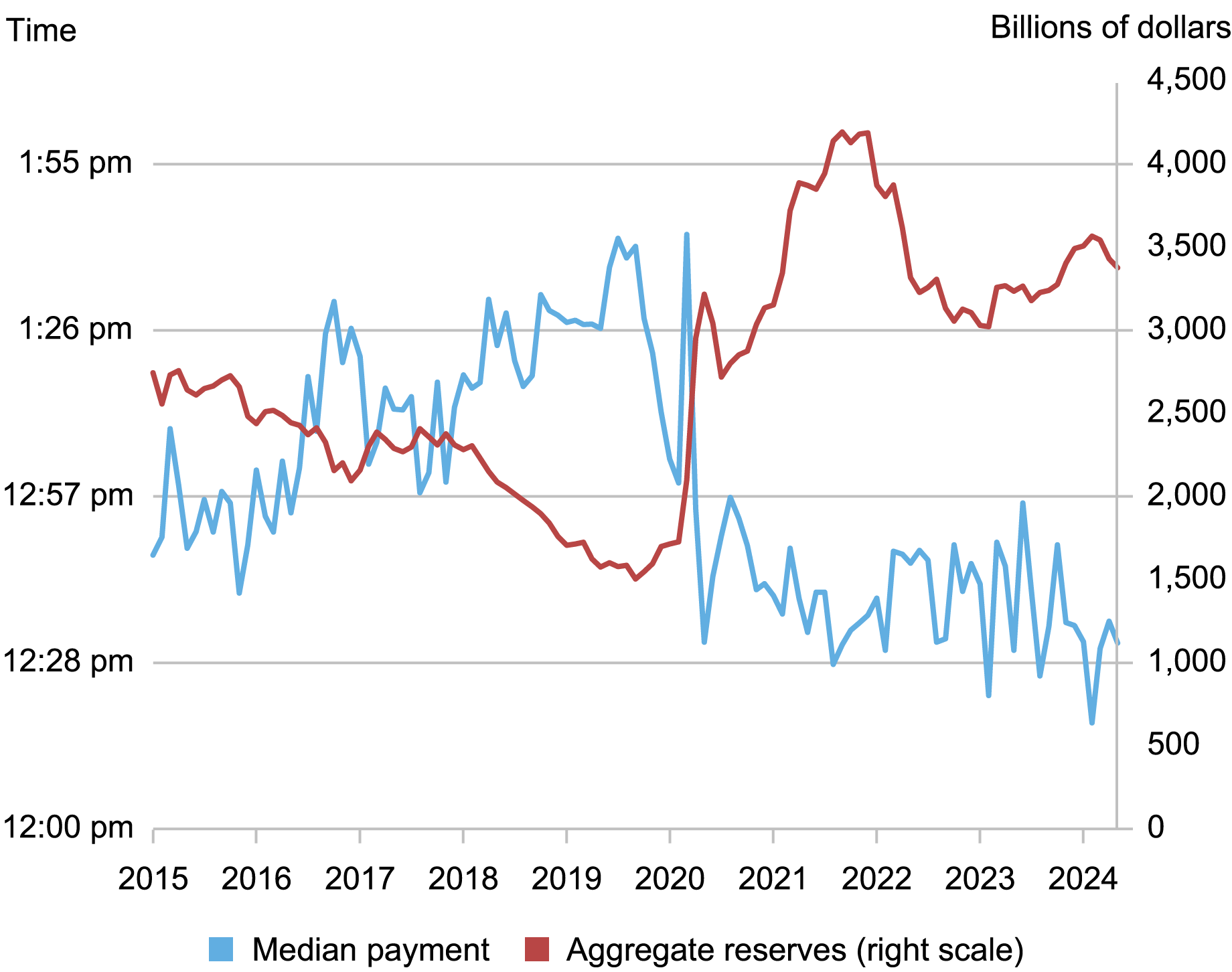

When the Federal Reserve adjustments the overall quantity of reserves held by banks, it instantly impacts the intraday demand for reserves by banks. Specifically, when the Fed will increase the overall quantity of reserves, banks’ concern over the intraday flows of reserves diminishes, as mentioned beforehand. This dynamic is seen within the chart beneath that plots combination reserves alongside the time of day when half of the overall worth of Fedwire Funds funds have been despatched (time of median cost). When there are low ranges of combination reserves, banks delay funds by a considerable quantity. Certainly, from 2015 to 2019, the regular decline in combination reserves from greater than $2 trillion to lower than $2 trillion is accompanied by an virtually one-hour shift later within the time of the median cost. Moreover, the substantial improve in combination reserves from 2019 to 2022 coincides with a big shift in funds being settled earlier within the day.

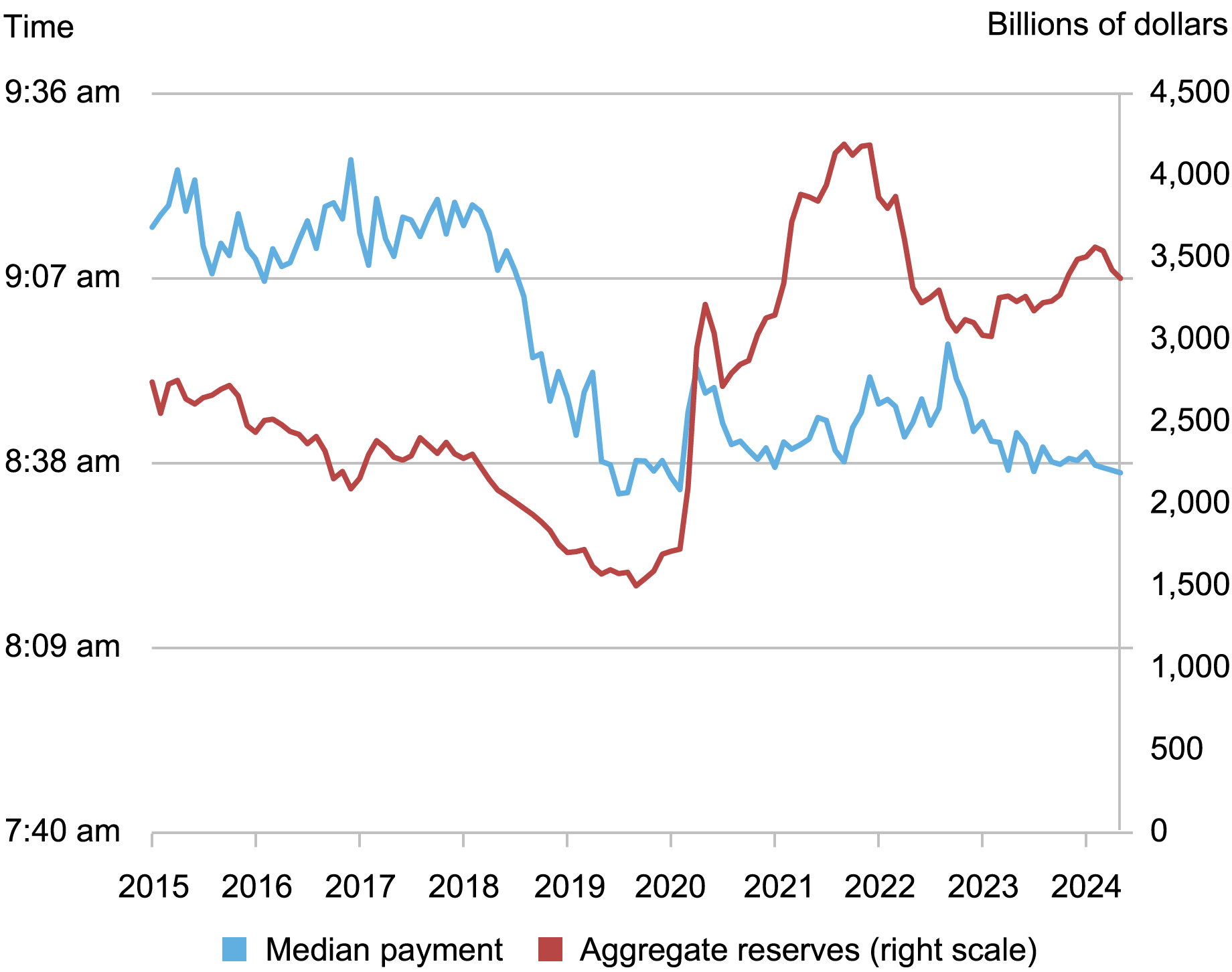

This affiliation between intraday settlement timing and combination reserves is just not seen with Fedwire Securities. Moderately, the timing of those transactions stays bunched at opening from 2015 to now. Beginning within the first half of 2018 and ending within the first half of 2019, there’s a 30 minute earlier-in-the-day shift within the time of median cost, however this shift is because of adjustments within the custodial enterprise and is unrelated to the extent of whole reserves.

The Timing of Fedwire Funds Funds Reacts to the Complete Degree of Reserves …

… Whereas the Timing of Fedwire Securities Funds Does Not.

Notes: The highest chart reveals when within the day the primary 50 p.c of whole transfers has occurred over Fedwire Funds (navy line). The underside chart reveals when within the day the primary 50 p.c of whole transfers (as measured by the money quantity) has occurred over Fedwire Securities (navy line). In each figures, the maroon line displays the overall quantity of reserves held by banks. Each figures span January 2015 to Could 2024.

Takeaway

The timing of funds over Fedwire Funds has garnered consideration as a result of shifts within the timing of funds are informative about banks’ demand for reserves and, consequently, the general degree of whole reserves within the system. Banks additionally want substantial quantities of reserves to settle their obligations on Fedwire Securities, particularly proper at opening. Not like what’s seen in Fedwire Funds nonetheless, the intraday timing of settlements on Fedwire Securities is invariant to adjustments within the whole quantity of reserves within the system.

Adam Copeland is a monetary analysis advisor in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Sarah Yu Wang is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Find out how to cite this put up:

Adam Copeland and Sarah Yu Wang, “The Dueling Intraday Calls for on Reserves,” Federal Reserve Financial institution of New York Liberty Avenue Economics, October 21, 2024, https://libertystreeteconomics.newyorkfed.org/2024/10/the-dueling-intraday-demands-on-reserves/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).