A key query in financial coverage is how labor market tightness impacts wage inflation and in the end costs. On this submit, we spotlight the significance of two measures of tightness in figuring out wage progress: the quits fee, and vacancies per searcher (V/S)—the place searchers embody each employed and non-employed job seekers. Amongst a broad set of indicators, we discover that these two measures are independently essentially the most strongly correlated with wage inflation. We assemble a brand new index, known as the Heise-Pearce-Weber (HPW) Tightness Index, which is a composite of quits and vacancies per searcher, and present that it performs better of all in explaining U.S. wage progress, together with over the COVID pandemic and restoration.

The Significance of On-the-Job Seek for Labor Market Tightness

Labor market slack is commonly measured utilizing the unemployment fee or the vacancy-to-unemployment ratio. In a current Employees Report (Heise, Pearce, and Weber, 2024), we construct on the theoretical basis by Bloesch, Lee and Weber (2024) who argue that wage inflation ought to as an alternative be strongly associated to quits and to vacancies per job seeker. The important thing argument is that on-the-job search is essential for understanding labor market tightness: since most new hires come from different jobs relatively than from unemployment, an applicable measure of labor market tightness should embody employed job seekers. Consequently, labor market tightness must be measured by vacancies per searcher, the place searchers mix employed, unemployed, and non-employed job seekers, relatively than simply vacancies over unemployment, or the unemployment fee.

The instinct behind this argument is that when vacancies per searcher is excessive, competitors for employees induces companies to lift supplied wages to stay aggressive. On the similar time, employees may have extra alternatives to vary jobs, resulting in the next quits fee. Because of this, the quits fee and vacancies per searcher are key elements of the wage Phillips curve and extra empirically informative than the unemployment fee or different measures of slack.

Our current Employees Report confirms this prediction in U.S. information. Crucially, we outline searchers as a weighted sum of the variety of short-term and long-term unemployed, employed, and non-employed employees, the place the weights are based mostly on estimates of those totally different employees’ search intensities. We then present that quits and vacancies per searcher outperform different commonplace measures of labor market tightness as predictors of wage progress. The desk beneath demonstrates this level by reporting outcomes from easy univariate regressions of the U.S. wage Phillips curve, rating indicators by their skill to suit U.S. wage information since 1990. We regress three-month wage progress from the Employment Price Index (ECI) on the measure listed, the place we standardize every of the measures to have imply zero and commonplace deviation of 1 to assist make comparisons of estimated coefficients. Column “Coefficient” presents the estimated coefficients and column “Match” exhibits the regression match.

We additionally create a composite measure of labor market tightness that takes a weighted common of quits and vacancies per searcher, utilizing regression coefficients from a regression of wage progress on these two variables because the weights. This composite index, which we name the HPW Tightness Index, is ranked first within the desk, indicating that it outperforms all different particular person variables. In accordance with the “Match” column, it explains about 60 % of wage progress throughout our pattern interval. The regression coefficient signifies {that a} one commonplace deviation enhance within the index is related to a 0.21 proportion level rise in wage progress.

Quits and Vacancies per Searcher Outperform Different Measures of Labor Market Tightness

| Measure | Coefficient | Match |

| HPW Index (Quits + V/S) | 0.21 | 0.60 |

| Quits fee | 0.20 | 0.55 |

| V/S | 0.20 | 0.52 |

| Employee hole | 0.18 | 0.44 |

| V/U | 0.17 | 0.41 |

| NFIB issue hiring | 0.17 | 0.41 |

| Conf. Board job issue | 0.17 | 0.40 |

| Hires/vacancies | 0.17 | 0.38 |

| Unemployment fee | 0.16 | 0.34 |

| Job discovering fee | 0.15 | 0.33 |

| Acceptance ratio (AC) | 0.16 | 0.30 |

| Log persevering with claims | 0.13 | 0.22 |

| Hires fee | 0.12 | 0.21 |

| Separation fee | 0.00 | 0.00 |

Notes: The “Coefficient” column reviews the rise in wages (in proportion factors) related to a one-standard deviation enhance in every indicator, whereas the “Match” column reviews the R‑squared worth from easy time-series regressions. All measures of tightness are ordered by their match. Estimates use information from 1990:Q2–2024:Q2, when quits information can be found, or shorter horizons within the few instances the place much less information can be found. We evaluate quits and vacancies per searcher towards the next different measures of labor market tightness: the employees hole (Vacancies-Unemployment)/Labor power; vacancies divided by the unemployment fee; the NFIB survey measure of small companies’ notion of employee availability; the Convention Board’s survey measure of shoppers’ notion of job availability; the hires/vacancies ratio; the unemployment fee; the job-finding fee; the Acceptance Ratio of job-to-job transitions divided by unemployment-to-employment transitions (Moscarini and Postel-Vinay, 2023); the log of the variety of persevering with claims for unemployment insurance coverage; the hires fee; and the separation fee. Wages are measured utilizing the employment value index. See Heise, Pearce and Weber (2024) for particulars.

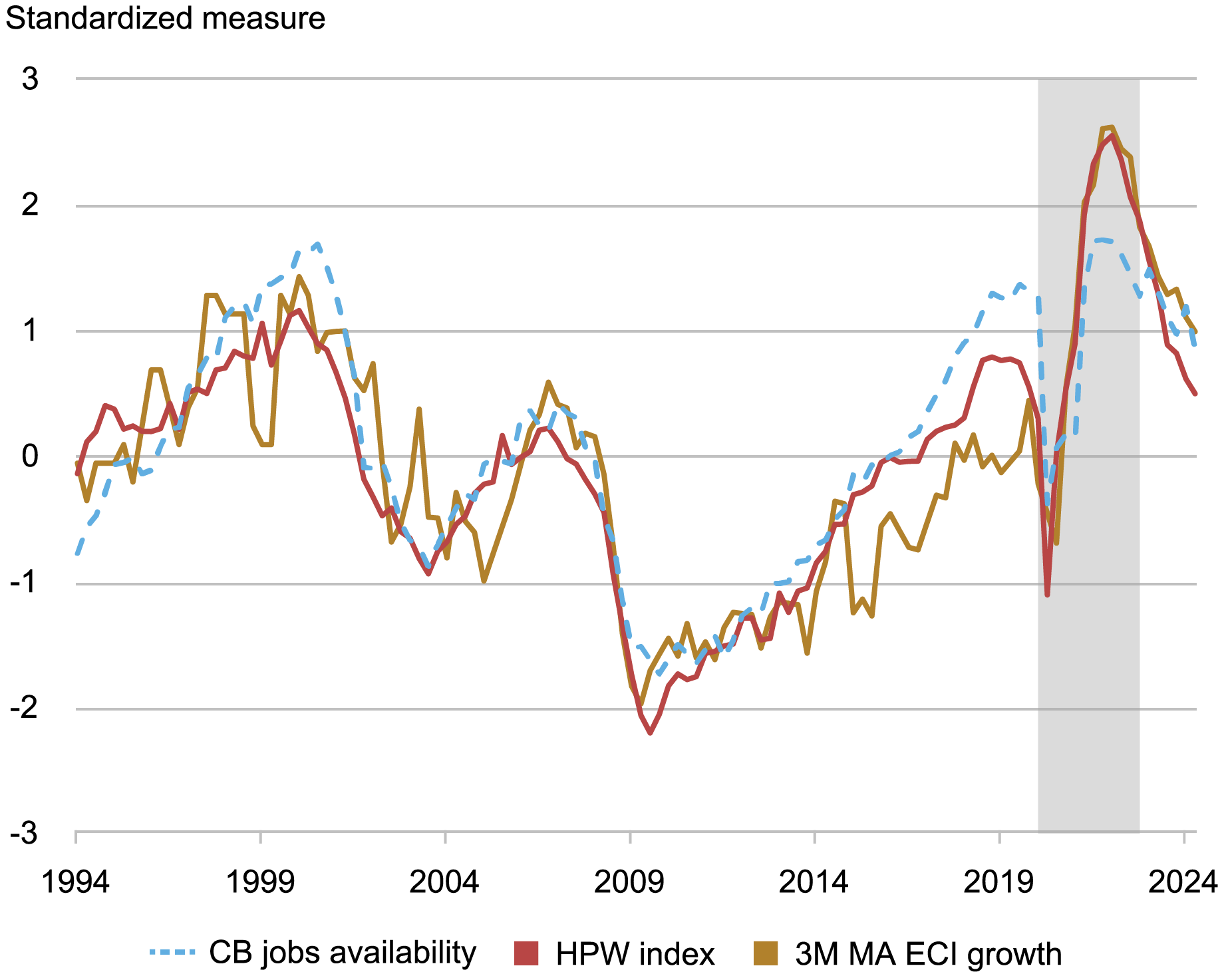

The chart beneath demonstrates the match of the HPW Index visually by plotting it towards wage progress, measured utilizing a three-period shifting common of the three-month progress within the ECI (each sequence are normalized to have a imply of zero and variance of 1 for ease of comparability). We evaluate our measure towards a standard measure of labor market tightness: the Convention Board’s survey measure of shoppers’ notion of job availability. Each the Convention Board measure and the HPW Index observe wage progress properly within the pre-pandemic interval. Nonetheless, within the pandemic interval, our measure performs considerably higher.

The HPW Index Tracks Wage Development Properly Even Throughout COVID

Supply: Authors’ calculations. Notes: The HPW Tightness Index, based mostly on quits and vacancies per searcher, tracks wage progress properly even through the COVID pandemic and restoration. All sequence are normalized to have zero imply and variance of 1 for ease of comparability. Wage progress is measured utilizing the employment value index. “CB Jobs Availability” is taken from the Convention Board. COVID interval and restoration 2020:Q1—2022:This fall is shaded.

No Proof for Nonlinearities in Wage Inflation

Given current curiosity in nonlinear results of labor market tightness on value inflation (Benigno and Eggertsson, 2024), we additionally examine whether or not there’s a nonlinear relationship between labor market tightness and wage inflation. We don’t discover any proof of nonlinearities. Certainly, there’s nothing uncommon within the wage/tightness relationship, both through the interval of maximum tightness within the aftermath of COVID, or later. This may be seen within the chart beneath, the place we offer a scatterplot of the HPW Tightness Index towards wage inflation. We discover a near-linear relationship between the 2 variables.

No Proof of a Nonlinear Relationship Between Wage Development and Labor Market Tightness

Notes: The connection between the HPW Tightness Index and nominal wage progress seems linear. Wages are measured utilizing the employment value index. Line match is a polynomial match based mostly on native observations.

Concluding Remarks

In abstract, the HPW Tightness Index of quits and vacancies per searcher performs properly in summarizing labor market tightness for the needs of figuring out wage inflation, in line with theoretical ends in Bloesch, Lee and Weber (2024). The connection remained sturdy through the COVID interval and restoration, suggesting that the empirical relationship documented is strong to even massive, uncommon financial shocks.

Sebastian Heise is a analysis economist in Labor and Product Market Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jeremy Pearce is a analysis economist in Labor and Product Market Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jacob P. Weber is a analysis economist in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The right way to cite this submit:

Sebastian Heise, Jeremy Pearce, and Jacob P. Weber, “A New Indicator of Labor Market Tightness for Predicting Wage Inflation,” Federal Reserve Financial institution of New York Liberty Road Economics, October 9, 2024, https://libertystreeteconomics.newyorkfed.org/2024/10/a-new-indicator-of-labor-market-tightness-for-predicting-wage-inflation/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).