Within the third quarter of 2024, debtors and lenders agreed, as they’ve over many of the previous three years, that credit score for residential Land Acquisition, Improvement & Building (AD&C) tightened. On the borrower’s aspect, the online easing index from NAHB’s survey on AD&C Financing posted a studying of -12.0 (the damaging quantity signifies credit score was tighter than within the earlier quarter). On the lender’s aspect, the comparable internet easing index primarily based on the Federal Reserve’s survey of senior mortgage officers posted an identical studying of -14.8. Though the extra internet tightening was comparatively delicate within the third quarter (as indicated by damaging numbers that had been smaller, in absolute phrases, than that they had been at any time since 2022 Q1), each surveys point out that credit score has tightened for eleven consecutive quarters—so credit score for AD&C should now be considerably tighter than it was in 2021.

In accordance with NAHB’s survey, the most typical methods during which lenders tightened within the third quarter had been by reducing the loan-to-value (or loan-to-cost) ratio, and requiring private ensures or collateral not associated to the undertaking—every reported by 61% of builders and builders. After these two, lowering the quantity lenders are prepared to lend was within the third place, with 56%.

Extra data from the Fed’s survey of lenders—together with measures of demand and internet easing for residential mortgages—is mentioned in an earlier publish.

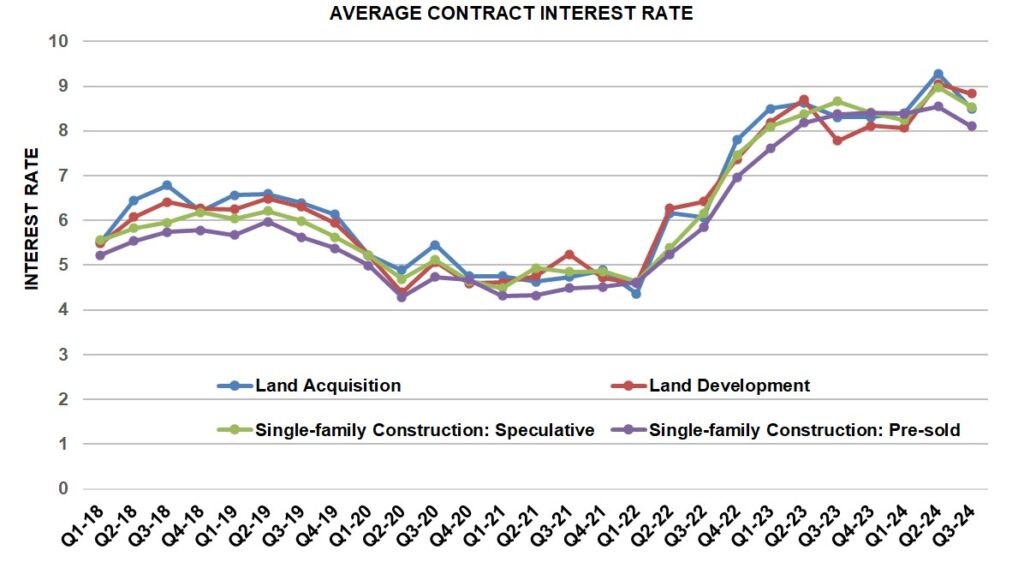

Though the supply of credit score for residential AD&C was tighter within the third quarter, builders and builders lastly received some reduction from the elevated value of credit score that has prevailed just lately. Within the third quarter, the contract rate of interest decreased on all 4 classes of AD&C loans tracked within the NAHB survey. The common price declined from 9.28% in 2024 Q2 to eight.50% on loans for land acquisition, from 9.05% to eight.83% on loans for land growth, from 8.98% to eight.54% on loans for speculative single-family development, and from 8.55% to eight.11% on loans for pre-sold single-family development.

Extra element on credit score circumstances for builders and builders is accessible on NAHB’s AD&C Financing Survey internet web page.

Uncover extra from Eye On Housing

Subscribe to get the most recent posts despatched to your e mail.