If you’re constructing a tech startup, accounting most likely doesn’t really feel very thrilling. Who needs to consider spreadsheets if you’re busy constructing or scaling?

However, as a Y Combinator funded firm and referral accomplice, we’ve seen a sample: promising startups commonly fail due to poor monetary administration.

On this article, we’ll discover the necessities of tech startup accounting, together with greatest practices, frequent errors, and the accounting software program we predict will make your life simpler.

Is Your Enterprise Financially Able to Elevate Funding?

Obtain your Collection A guidelines:

The Significance of Accounting for Tech Startups

Accounting is about greater than compliance. Startups that hope to draw enterprise capital want to have the ability to present high-level monetary statements to buyers. Not solely does it velocity up their due diligence, however founders who observe good monetary hygiene are higher outfitted to make knowledgeable selections, handle money circulate, and show the self-discipline that builds confidence amongst buyers.

Good accounting additionally helps keep away from expensive errors: misfiled taxes, underreported fairness, or mismanaged money circulate can snowball into main issues.

|

Necessary: Startup funding offers crumble on a regular basis due to this oversight. Don’t make this error.

Presumably, the worth of shares will enhance over time. With out an 83(b) election, the IRS will deal with that enhance as taxable earnings. Consequently, founders who don’t make 83(b) elections are much less engaging to buyers or collaborators.

|

What’s Distinctive About Tech Startup Accounting?

Typical corporations and startups are completely different sufficient, however tech startups include an added layer of complexity that’s necessary to think about. Let’s discover what makes tech startup accounting distinctive.

Income Recognition Timing: Money vs. Accrual

This is among the extra frequent causes startups come to us for assist. In the event you run a SaaS enterprise mannequin, income recognition is trickier than simply recording cash when it lands in your account. Since clients usually pay upfront for long-term subscriptions, that you must defer income throughout the size of the service.

The secret’s the distinction between money and accrual accounting.

You’re already acquainted with money accounting; it’s how folks handle family budgets, the place transactions depend when cash bodily adjustments arms. Accrual accounting is a bit trickier. This methodology acknowledges income and bills on the time the service is supplied, no matter when cash adjustments arms.

Accrual accounting is best suited to tech startups. It requires extra refined accounting however is extra correct and, if utilized strategically, may even save an organization cash on taxes.

Learn how to Worth Mental Property?

Mental property is commonly the crown jewel of a tech startup. Whether or not it’s software program, a proprietary algorithm, or a patent, your IP could be a key driver of investor valuation. However accounting for IP isn’t so simple as itemizing it as an asset.

There are a number of valuation strategies to think about, and also you’ll must resolve whether or not the prices related to growth must be capitalized (unfold over time) or expensed instantly. Every strategy has tradeoffs, however regardless, there are additionally regulatory necessities to be cautious of when itemizing IP as an asset.

Fairness

Fairness is among the most important sources of accounting complexity for tech startups. Monitoring cap tables, understanding inventory choices, convertible notes, SAFE agreements, and compliance with tax legal guidelines isn’t simple. When it’s time to allocate fairness, make sure you get assist from an skilled.

Y Combinator CFO Kirsty Nathoo, in a lecture at Stanford, shared the next recommendation to aspiring founders questioning about methods to navigate fairness allocation:

- If fairness allocation amongst founders may be very disproportionate, that’s a crimson flag. In YC corporations with the best valuations, there are zero cases the place the founders have a considerably disproportionate fairness cut up.

- Founders usually give appreciable credit score, and fairness, to the one who had the concept for the corporate. However execution is far extra useful. The trouble and teamwork it takes to execute a imaginative and prescient is what drives success.

- The usual vesting interval in Silicon Valley is 4 years with a one yr cliff.

- Fairness for founders must be topic to vesting schedules. Individuals want pores and skin within the sport to incentivize them to proceed working. It’s additionally a useful solution to construct tradition and set an instance for workers.

- Even if you happen to’re a founder, creating and signing a inventory buy settlement is necessary. Simply as an worker receiving inventory as compensation would count on to signal a doc, it is best to too.

Distinctive Value Constructions

Not like conventional companies, tech startups spend closely on R&D, software program growth, and IT infrastructure. Many of those prices may be deducted or depreciated, which might cut back tax legal responsibility, however doing so requires cautious accounting and reporting.

Speedy Development and Scaling

If all goes effectively, your startup might go from a small crew to a worldwide operation in only a few brief years. That sort of change brings distinctive accounting challenges, from managing elevated transaction volumes to navigating multi-state and worldwide tax guidelines.

For example, if you happen to increase internationally, you might have to navigate “switch pricing” legal guidelines, which govern how income is allotted and taxed amongst enterprise entities you personal throughout completely different international locations. With out correct experience, this complexity might shortly turn into overwhelming.

Accounting Metrics Each Startup Ought to Monitor

There are an awesome variety of variables you might hold observe of. It’s simple to lose the forest for the timber. However if you’re brief on time, there are a handful of variables it is best to all the time monitor commonly:

Cash In (Accounts Receivable): What income is coming in, and when.

Cash Out (Accounts Payable): What bills are due, and when.

Burn Fee: How far more you’re spending than incomes.

Financial institution Steadiness: How a lot money and different liquid belongings can be found.

Runway: How lengthy earlier than money runs out; calculated by dividing financial institution stability by burn fee. Typical knowledge suggests sustaining a minimum of six financial savings within the financial institution.

Whereas these 5 metrics gained’t exchange a complete monetary technique, they may provide help to deal with what issues most: preserving observe of money circulate and guaranteeing you stay financially secure.

For extra info, we cowl detailed KPIs in our monetary planning for SaaS startups article.

| Professional tip: Be careful for “lumpy” bills. Authorized charges, workplace deposits, and different massive one-time purchases can distort your burn fee and runway calculations. To keep away from getting off observe, finances for each conservative and optimistic situations. |

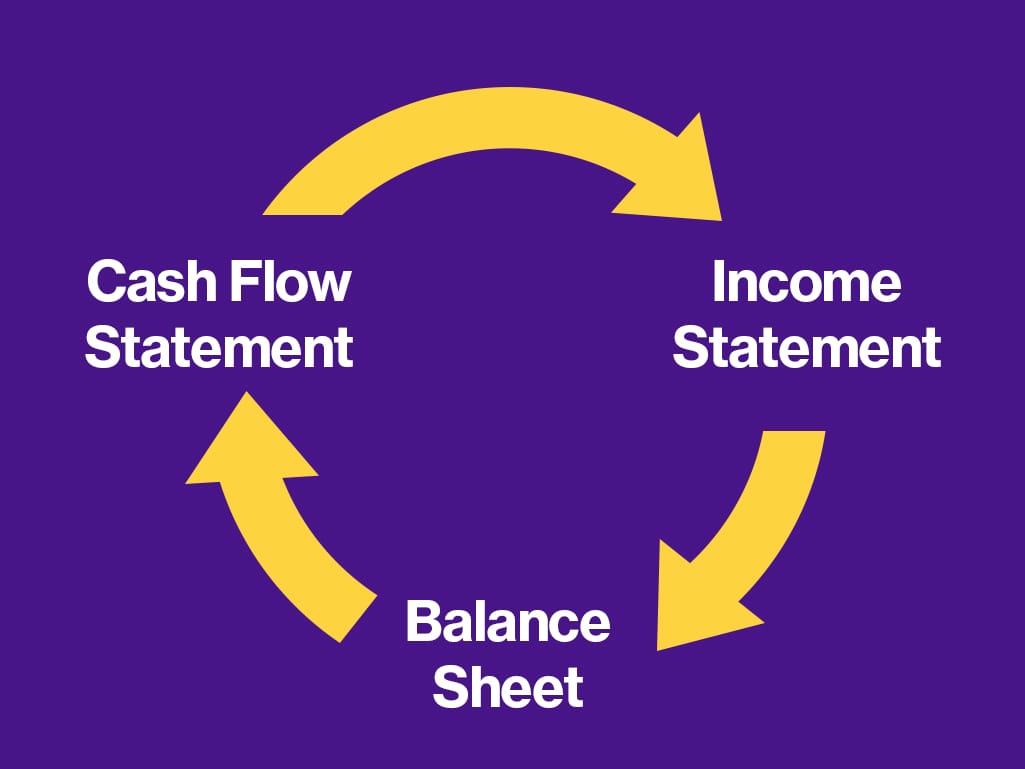

The Three-Assertion Monetary Mannequin

As a founder, you perceive your enterprise inside and outside. You’ll know your runway, your enterprise mannequin, and the probably impression completely different tweaks or investments might need on your enterprise. However when it comes time to speak your imaginative and prescient to stakeholders or pitch buyers, you’ll want these three elementary monetary statements.

One of many first issues indinero does with early-stage corporations is present fundraising help with a three-statement [cash flow, income, balance sheet] monetary mannequin. The purpose is to know the drivers of a enterprise in order that we may also help with investor relations, board decks, displays, and liaise with banks or institutional buyers.” – Brian Johnson, indinero fractional CFO

Money Movement Assertion

This assertion seems at an organization’s potential to satisfy short-term obligations by monitoring money coming out and in over time. It’s divided into three sections:

- Operational: Funds from core enterprise actions.

- Investing: Lengthy-term asset purchases that can repay over the long run.

- Financing: Capital earned by promoting fairness or soliciting loans from lenders.

The trick to understanding a money circulate assertion is that solely cash that adjustments arms is counted. Invoices that haven’t been paid, loans that haven’t been dispersed, and fairness offers that haven’t been closed aren’t mirrored right here.

For a deeper dive, learn our article on money circulate administration for startups.

Revenue Assertion:

Additionally referred to as the revenue and loss (P&L) assertion, this report summarizes income, bills, and internet revenue over time. At first look, it most likely sounds much like the money circulate assertion, however differs in necessary methods.

The aim of the earnings assertion is to measure profitability, whereas the money circulate assertion is simply considering whether or not an organization can meet short-term bills. For comparability, one assertion treats loans as an inflow of money, whereas the opposite data curiosity as an expense towards profitability. Moreover, earnings statements function on an accrual foundation, whereas the money circulate assertion solely registers flows solely when cash adjustments arms.

Steadiness Sheet

Steadiness sheets present a snapshot of an organization’s monetary place at a selected time limit. It lists an organization’s belongings (what it owns), liabilities (what it owes) and fairness. The basic stability sheet equation is:

Fairness = Belongings – Liabilities

Accounting vs Bookkeeping

Most tech startup founders have backgrounds in coding somewhat than finance, so if you happen to’re new to this world, you may surprise about the distinction between an accountant and a bookkeeper.

In brief, bookkeepers are report keepers. They deal with day-to-day transactions equivalent to accounts receivable and accounts payable. Their work retains the home so as and serves as the idea of accounting.

Accountants function on a better stage. They put together monetary statements, deal with tax submitting, and assist companies strategize for the long run. They’re well-versed in GAAP (Typically Accepted Accounting Ideas), assist navigate variations between money and accrual accounting, and assist startups design fairness buildings.

All startups want a bookkeeper; that might be a DIY founder or one thing you outsource. Whether or not you want an accountant is dependent upon your development stage, however on the very least, take into account hiring assist for end-of-year taxes. There are extra essential issues for founders to do than IRS compliance.

Accounting Greatest Practices

Accounting isn’t probably the most glamorous a part of operating a enterprise, however following some greatest practices will prevent time, cash, and complications down the street.

- Preserve private and enterprise financial institution accounts separate.

That is a straightforward mistake to make if you’re getting began, however essential to keep away from. Mixing bills creates confusion, eliminates the private legal responsibility safety an LLC supplies, and makes fundraising significantly tougher. - Examine your financials regularly.

You’d be stunned what number of founders don’t do that commonly. Common opinions provide the perception to make knowledgeable selections, catch issues early, and hold objectives on observe. - Search for damaging numbers in your projections and strange variances in bills.

These points can elevate crimson flags, however as a rule, they’re simply easy knowledge entry errors. It’s simple to by accident report an expense twice, particularly if you happen to’re doing DIY bookkeeping. - Use devoted financial institution accounts and bank cards for expense and exercise classes.

Utilizing separate accounts for various duties – equivalent to payroll, advertising, or operations – makes managing budgets simpler. When accounts are intentionally organized, it’s simple to catch a spiking expense or dipping income supply. - Present invoicing protocols to suppliers, contractors, and purchasers.

Tips on when and methods to submit invoices, what particulars to incorporate, and anticipated timelines for fee assist keep away from disputes and guarantee everyone seems to be paid promptly. The lowered back-and-forth streamlines your accounts payable and receivable processes and strengthens relationships with key companions. - Create course of paperwork for coaching.

As your startup grows, you’ll delegate many duties you’ve been accustomed to doing your self. Documenting the processes you’ve developed makes it simpler to onboard new crew members whereas guaranteeing accuracy and consistency. Plus, having a written report minimizes the chance of information gaps if you happen to or another person leaves the crew.

Do Startups Want Accountants?

The brief reply is: It is dependent upon the stage of your startup and your particular wants.

All startups ought to deal with their funds responsibly, particularly in the event that they’re spending investor {dollars} somewhat than their very own, however the determination to rent assist comes right down to complexity and the way you need to spend your time.

Tax returns aren’t price a founder’s time. They must be filed yearly, so even within the first yr of an organization’s life, some service will must be engaged. There are alternatives out there, equivalent to indinero, which attempt to make issues as easy as attainable from the founder’s viewpoint.” – Y Combinator CFO, Kirsty Nathoo

When Startups Don’t Want Assist

Within the very early days, you may handle with out skilled accounting or bookkeeping assist. When funds are easy, it’s easy sufficient to evaluate cash coming out and in of your checking account and make do with DIY options equivalent to Quickbooks.

Nonetheless, it’s essential to take care of copies of each digital and paper receipts. Sooner or later, you’ll file taxes or rent assist and want these data to categorize enterprise bills.

When Startups Do Want Assist

Annual tax submitting is a motive to get accounting assist, no matter what stage your startup is in. Hiring year-round help begins making sense as you develop and complexity will increase. Including workers, managing complicated fairness distributions, or elevating cash from buyers are all worthwhile causes to rent a CPA or CFO.

Bookkeeping Guidelines

Properly-kept books are the muse of an accountant’s work; the higher your data, the simpler the accounting.

As your startup grows, you’ll increase to utilizing a number of financial institution accounts, bank cards, and fee processors. These entities will hold lists of economic transactions, however you may’t depend on them as you’d a bookkeeper. Start by consolidating this info right into a single inside spreadsheet or accounting software program device.

Subsequent, you’ll must make a number of key selections and set up common processes for sustaining the books. Right here’s a quick guidelines:

- Select an accounting methodology: money or accrual.

- Combine software program together with your monetary accounts for simple record-keeping.

- Set up an expense coverage that dictates who is allowed and answerable for varied bills.

- Usually evaluate checking account and credit score transactions for discrepancies.

- Replace accounts receivable, noting funds and following up on overdue invoices.

- Double-check accounts payable, log bills, and guarantee you’ve got sufficient money to cowl deliberate bills.

- Categorize bills for simpler monitoring, reporting, and year-end tax prep.

- Monitor burn fee and runway based mostly on latest bills and financial institution balances.

Software program Suggestions

Indinero has spent years offering accounting and bookkeeping companies to companies small and huge. Over time, we’ve recognized a number of the greatest off-the-shelf software program in the marketplace. Right here’s a breakdown of a number of the hottest choices.

| Software program | Recognized For | Ideally suited For |

| Invoice.com | Automating accounts payable and accounts receivable workflows | Startups managing a excessive quantity of invoices |

| Expensify | Monitoring and reporting worker bills | Groups with frequent journey or reimbursement wants |

| Receipt Financial institution (Dext) | Organizing and managing receipts and invoices | Streamlining doc administration |

| Fathom | Monetary evaluation and forecasting | Investor displays and strategic administration |

| NetSuite | Enterprise-level monetary administration | Scaling startups or international operations |

| Stripe | On-line fee processing and subscriptions | SaaS, e-commerce, and tech startups |

| Gusto | Payroll, HR, and advantages administration | Startups constructing or managing a workforce |

Widespread Errors

If you’re launching a startup, it’s simple to get caught up in constructing a product or discovering your first clients. Accounting may naturally take a backseat. Nonetheless, overlooking funds can result in expensive errors.

Probably the most frequent errors is failing to trace bills and hold receipts. It’s simple to lose observe of small purchases, however these small oversights add up, particularly when it’s time to file taxes or share the way you’ve been spending investor cash. Take into account proactively implementing Expensify or Dext to keep away from this drawback.

Failing to file an 83(b) election is one other mistake that may have important long-term penalties, and there’s a motive Y Combinator startup advisors harp on this with their new founders. As shares vest and enhance in worth, so do the earnings tax penalties of receiving them as compensation. By submitting the 83(b) election, you may lock within the decrease fairness valuation for tax functions, saving you and would-be buyers significantly.

Tax compliance and deadlines additionally journey up some founders. Submitting taxes late or misclassifying bills can carry penalties and even set off audits. For startups increasing into a number of states or international locations, it’s simple to unintentionally run afoul of native tax legal guidelines. It is a case the place educated CPAs are price consulting with.

Some startups select money accounting when accrual accounting is a greater match. Money could also be easier, but it surely doesn’t account for income or bills as precisely as accounting. Plus, accrual accounting can decrease tax burdens through strategically timed investments.

Lastly, a mistake many founders remorse is ready too lengthy to hunt skilled assist. DIY accounting and bookkeeping can work within the earliest levels, however as monetary administration turns into extra complicated, the chance price of specializing in one thing that isn’t your space of experience can outweigh the cash saved by avoiding outsourcing.

Conclusion

From guaranteeing compliance, managing money circulate, making ready for funding rounds, and scaling operations, strong accounting is necessary to your startup’s success.

Indinero has simplified accounting, bookkeeping, and monetary administration for startups of all sizes. Whether or not you’re beginning out or making ready to boost your subsequent funding spherical, we’re right here to assist take management of your funds. Attain out for a complimentary session immediately.