When you’re hoping for a fast launch of Fannie Mae and Freddie Mac, you would possibly wish to train some persistence.

Whereas the percentages of the pair exiting conservatorship elevated sharply as soon as Trump’s second time period started, it nonetheless faces an uphill battle.

One of many main sticking factors is mortgage charges, which many count on to extend in the event that they’re launched.

Having a near-explicit assure that Fannie and Freddie will purchase and securitize mortgages makes them cheaper for shoppers.

The expectation is that if/after they go public, mortgage charges would should be larger to compensate for elevated danger.

Fannie and Freddie Have Been in Conservatorship Since 2008

First some fast background. After the worst housing disaster in latest historical past, Fannie Mae and Freddie Mac, often called the government-sponsored enterprises (GSEs) have been positioned in conservatorship.

This was primarily a authorities bailout because the pair have been “severely broken” on account of the early 2000s mortgage meltdown and “unable to satisfy their missions with out authorities intervention.”

The association allowed them to proceed to assist the very fragile housing market because it recovered over the previous decade.

However maybe no one anticipated the pair to stay in authorities palms so long as they’ve.

Ultimately look, it has now been practically 20 years! In fact, this isn’t the primary time efforts have been made to launch them again into the wild.

Throughout Trump’s first time period that started again in 2017, there was quite a lot of discuss of a launch. And the shares of each firms responded accordingly.

They have been buying and selling within the $1 vary in late 2016 and shortly elevated to greater than $4 per share in early 2017 earlier than fading once more.

As soon as the privatization of Fannie Mae and Freddie Mac misplaced steam, they ultimately grew to become penny shares.

Numerous Investor Hypothesis Surrounds Their Launch

Like eight years in the past, there’s been quite a lot of investor hypothesis surrounding their launch, which arguably is a part of the issue.

It appears of us are extra attention-grabbing in making a buck on a commerce than contemplating the precise implication of their launch. Go determine…

The most recent speculator to get in on the obvious gold rush was investor Invoice Ackman, whose Pershing Sq. Capital Administration agency “might personal about 180 million widespread shares of the 2 firms.”

And he might reportedly see a $1 billion achieve on the funding, with the shares probably climbing to round $34 post-IPO.

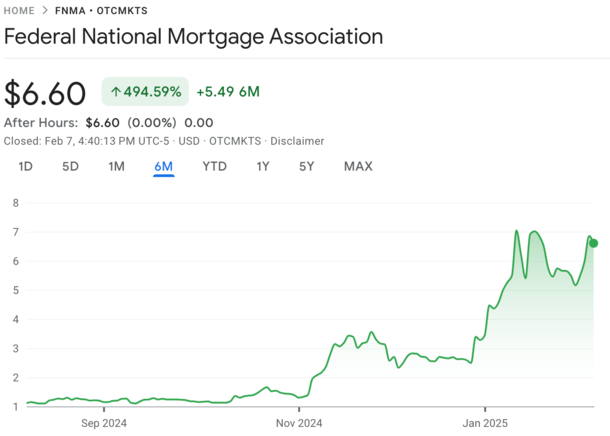

For reference, they at the moment commerce at round $6 every, so it could symbolize fairly the achieve.

Much like situations previous to Trump’s first presidential victory, the pair have been buying and selling within the $1 vary.

However they’ve since skyrocketed, with each FNMA and FMCC up roughly 500% since Trump gained a second time period and hypothesis about their launch reached euphoric ranges.

As famous, that is the battle of curiosity at the moment in play. And the identical problem we noticed eight years in the past. It’s a inventory commerce as an alternative of a “Hey, is that this good for our nation?”

Fannie and Freddie’s Launch Will Hinge on Influence to Mortgage Charges

Whereas traders are hoping the pair get launched and make them untold riches, we should always solely launch them when it’s protected and applicable to take action.

If newly-appointed Treasury Secretary Scott Bessent, who’s by the way additionally the brand new appearing director of the Client Monetary Safety Bureau (CFPB) does the correct factor, that may not be for a while.

In an interview with Bloomberg this week, when requested about their launch, Bessent mentioned, “Proper now the precedence is tax coverage. As soon as we get by that, then we are going to take into consideration that.”

He added that “The precedence for a Fannie and Freddie launch, crucial metric that I’m taking a look at is any research or trace that mortgage charges would go up.”

“So something that’s accomplished round a protected and sound launch goes to hinge on the impact of long-term mortgage charges.”

Merely put, he and people round him are conscious that mortgage charges will doubtless rise if Fannie and Freddie are pressured to face on their very own.

And since mortgage charges have surged from round 3% to begin 2022 to roughly 7% right this moment, the very last thing the Trump administration desires is larger charges.

So actually it boils all the way down to serving to traders get wealthy or serving to on a regular basis People purchase houses with decrease mortgage charges.

Can be an attention-grabbing choice…

The Pair Ought to Be Launched, However Maybe Slowly After They Cut back Their Footprint

My ideas on the matter are that the pair aren’t able to be launched. Not a lot has modified since they went beneath conservatorship, aside from mortgage high quality vastly bettering.

Certain, they don’t have practically as many worries about mortgage defaults and foreclosures, however in addition they proceed to again the overwhelming majority of house loans in america.

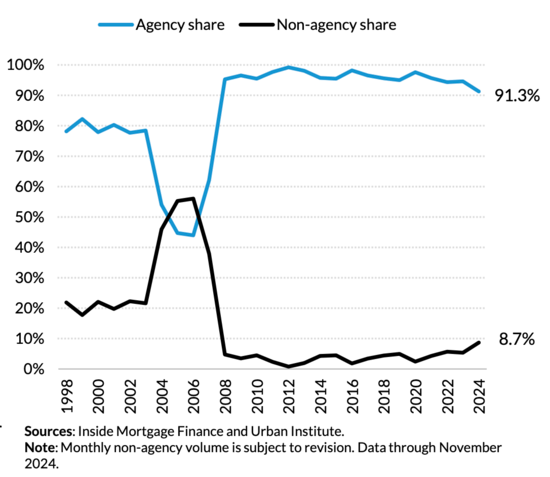

Look a the chart above from the City Institute. Greater than 91% of MBA issuance is agency-backed, which does embody FHA and VA too. However about 40% of first-lien originations are GSE, whereas simply 4.1% is private-label.

With out them, there could be chaos within the mortgage market. Even when launched, there would doubtless be chaos.

Nonetheless, they need to be launched sooner or later if they’re really public firms, and never authorities entities.

A greater method about going about it could be drastically decreasing their footprint earlier than that occurs (sorry traders).

To take action, they will pull again or fully cease shopping for and securitizing mortgages tied to second houses and funding properties.

In different phrases, restrict their choices to main residences for on a regular basis owners versus those that are shopping for a second, third, fourth, and even fifth house.

There may very well be further adjustments to their product menu, which might make it smaller, with the implied function of ushering in additional personal capital to the mortgage market.

As Fannie and Freddie obtained smaller, personal gamers might develop bigger and play extra of a job.

This would scale back our reliance on the pair, and reduce the impression of their eventual launch.

(picture: Virginia State Parks)

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house consumers higher navigate the house mortgage course of. Observe me on Twitter for decent takes.