Credit score Karma has simply introduced a brand new enterprise generally known as “Credit score Karma House Loans” that can current mortgage refinance provides to its thousands and thousands of members.

The brand new rollout can be powered by Higher Mortgage and its Tinman AI Platform.

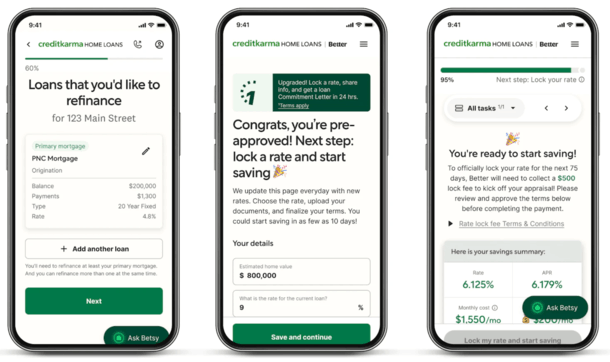

When you go surfing to Credit score Karma, you’re sometimes offered with numerous credit score provides associated to your present credit score traces, whether or not it’s a brand new bank card or stability switch supply.

Now these with an present mortgage may even see customized provides on their account dashboard if there’s a chance to economize there too.

In keeping with Credit score Karma, thousands and thousands of its members presently have mortgages and “many are paying rates of interest over 6%.”

Credit score Karma House Loans Will Be Powered by Higher Mortgage

Some time again, Higher Mortgage mentioned it had some main offers within the works, together with one unnamed monetary platform.

Now we all know who it’s and it’s a biggie as a result of Credit score Karma has roughly 140 million customers (by the way in which that is who I guessed it will be).

As famous, the brand new Credit score Karma House Loans division can be powered by third-party lender Higher Mortgage.

Nevertheless, it’s going to act as a mortgage dealer, which means your refinance software could not essentially go to that firm.

As a substitute, the Credit score Karma platform will scan for money-saving alternatives for its mortgage members “across the clock” amongst over 40 monetary establishments.

And if one thing favorable is discovered, you’ll be notified once you go to the positioning to examine your credit score scores and/or credit score report.

Much like these bank card provides you already see when you go surfing, you may be offered with a fee and time period refinance to avoid wasting you X quantity monthly.

For instance, if Credit score Karma is aware of you may have a $400,000 mortgage with an rate of interest of 6.875%, they could current a refinance supply at present charges from one in every of their companions.

If they’ll get you a brand new fee of 5.875% as an alternative, you’ll see the supply and related financial savings, at which level you’ll be capable of apply by way of the app.

In addition they help you evaluate your credit score profile for any points which may have an effect on your mortgage software.

How Are Credit score Karma’s Mortgage Charges?

It’s necessary to level out that Credit score Karma is just appearing as a dealer right here, just like how they current provides from third-party bank card issuers, auto lenders, and so on.

So that you’ll be offered with the “greatest provides” from their mortgage lender companions, which probably consists of Higher since they’re a consumer-direct lender themselves.

Whereas we don’t know the way aggressive the collaborating lenders can be, Credit score Karma says by way of using expertise they’ll be “in a position to scale back prices and move these financial savings on to our members within the type of higher charges and decrease month-to-month funds.”

Higher has made this declare many instances as nicely, arguing that it could actually lower the bloat and supply below-market charges consequently.

That mentioned, this partnership will lean closely on AI, with so-called “clever automation” streamlining mortgage eligibility, doc retrieval, and mortgage underwriting.

Credit score Karma members will apparently be capable of get pre-approved for a mortgage in as a bit as 5 clicks whereas interacting with Betsy, the primary AI voice-based mortgage mortgage agent.

And thru the Tinman AI Platform, your credit score and property information can be shopped (I assume anonymously) throughout 40+ monetary establishments and 1,500 mortgage merchandise.

Their “data-driven method ensures members are proven this system they’re truly permitted for and the bottom fee and charge combos obtainable.”

The corporate believes it could actually take away friction that usually prevents present householders from even beginning the refinance journey to start with.

The tip consequence will ideally be saving extra householders cash on mortgages they’re presently overpaying for.

Whether or not they finally supply dwelling buy loans as nicely stays to be seen.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) dwelling consumers higher navigate the house mortgage course of. Observe me on X for warm takes.