This morning, the Nationwide Affiliation of Realtors (NAR) reported that pending house gross sales dropped 6.3% in April from a month earlier.

They have been additionally 2.5% decrease than ranges seen on the identical time final yr, dampening any hope of 2025 being a comeback yr for house gross sales.

The wrongdoer? Excessive mortgage charges. You’ll be able to argue they aren’t that prime traditionally, however they continue to be a lot larger than a couple of years in the past.

They usually elevated from ranges seen in March, taking the wind out of the housing market’s sails through the important spring shopping for session.

As such, present house gross sales will seemingly see tender prints in future releases (although a bump larger may be anticipated for Could based mostly on the decrease charges seen in February and March).

It’s All About Mortgage Charges

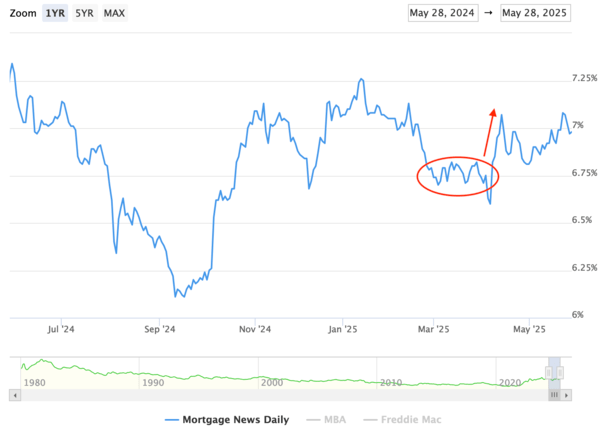

We are able to argue till the cows come house, that it’s excessive house costs not excessive mortgage charges, however the knowledge continues to make the argument it’s the latter (see chart above from MND)

Even NAR chief economist Lawrence Yun stated, “At this important stage of the housing market, it’s all about mortgage charges.”

He added that “decrease mortgage charges are important to deliver house patrons again into the housing market.”

I are likely to agree with him right here (although I don’t all the time agree with him). On the identical time, I’ve acknowledged that house costs are “excessive” too.

Downside is, house costs are sticky and even when they do ease considerably, which they most likely will, the influence isn’t as helpful.

For instance, a 1% drop in mortgage charges is the same as roughly an 11% drop in house costs. So you really want costs to dump to spice up buying energy.

Alternatively, you get a pleasant drop in mortgage charges and potential house patrons can afford much more house.

This additionally explains why house builders lean so closely on mortgage fee buydowns. They might decrease the worth, which some do, however reducing the rate of interest is rather more efficient.

So whether or not house costs are too excessive or not is moot right here. To herald extra patrons, we want decrease mortgage charges.

And near-7% charges merely received’t do. But if and when charges hover nearer to the 6% mark, it appears patrons perk up and dip their toes once more.

So we’re not really that far off right here, we simply want readability on the tariffs, commerce conflict, and authorities spending invoice so yields can come down and charges can ease.

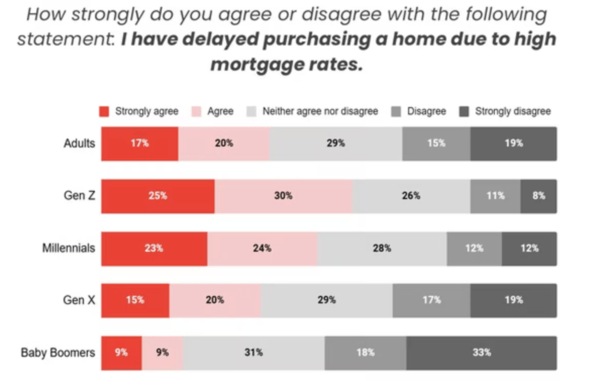

Gen-Z and Millennials Are Delaying Residence Purchases Due to Excessive Mortgage Charges

Now I current to you some knowledge to again up the concept that it’s mortgage charges, not house costs.

A brand new Could 2025 survey from Realtor.com discovered that “persistently excessive mortgage charges proceed to restrict purchaser exercise.”

Senior financial analysis analyst Hannah Jones famous that about one-third of respondents indicated that they’ve delayed a house buy due to “still-high charges.”

And it’s much more prevalent amongst key house shopping for cohorts, together with Millennials and Gen-Z generations.

Some 55% of Gen-Z respondents strongly agreed or just agreed that they’ve delayed a house buy as a consequence of excessive mortgage charges.

The identical was true for 47% of Millennials, which has been the largest cohort of house patrons for a lot of the previous decade.

This may additionally clarify why Boomers overtook them just lately as the most important share of house patrons.

Regardless of this, they nonetheless need to purchase a house, with 23% of Millennials saying so this yr, in contrast with solely 15% final September.

So maybe they’re additionally getting over the truth that mortgage charges are excessive, and/or changing into extra snug with the brand new regular for mortgage charges.

Nevertheless it does let you know that if and when charges come again down nearer to six%, we may see an enormous uptick in house purchases.

The one caveat is that if charges solely return to these ranges as a consequence of a wobbly financial system, that would offset any anticipated house purchaser demand.

In spite of everything, you want a job in order for you a mortgage, so if rising unemployment is the rationale for falling mortgage charges, we’d have an issue.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house patrons higher navigate the house mortgage course of. Comply with me on X for warm takes.