In assist of the Nationwide Flood Insurance coverage Program (NFIP), the Federal Emergency Administration Company (FEMA) creates flood maps that point out areas with excessive flood threat, the place mortgage candidates should purchase flood insurance coverage. The results of flood insurance coverage mandates have been mentioned intimately in a prior weblog collection. In 2021 alone, greater than $200 billion value of mortgages have been originated in areas lined by a flood map. Nevertheless, these maps are discrete, whereas the underlying flood threat could also be steady, and they’re generally outdated. Consequently, official flood maps might not absolutely seize the true flood threat an space faces. On this publish, we make use of distinctive property-level mortgage knowledge and discover that in 2021, mortgages value over $600 billion have been originated in areas with excessive flood threat however no flood map. We look at what sorts of lenders are conscious of this “unmapped” flood threat and the way they modify their lending practices. We discover that—on common—lenders are extra reluctant to lend in these unmapped but dangerous areas. People who do, similar to nonbanks, are extra aggressive at securitizing and promoting off dangerous loans.

A Property-Degree Method

Previous work that has tried to investigate the affect of flood threat on mortgage lending has suffered from an absence of both property-level flood threat knowledge or property-level mortgage knowledge. This deficiency has compelled researchers to make assumptions about flood threat or mortgage lending over bigger areas with a number of properties, finally stopping clear identification. On this evaluation (and the related paper), we overcome these points by leveraging a novel knowledge set that matches property-level mortgage information from 2018 to 2021 within the Dwelling Mortgage Disclosure Act (HMDA) knowledge with property-level flood threat knowledge from CoreLogic and nationwide FEMA flood maps that we digitized for the workouts within the paper. The granularity permits us to review threat and lending in additional element than has beforehand been attainable.

We think about a property to be lacking a flood zone designation on a FEMA map (or to be “unmapped”) whether it is at a better threat than half of all properties with non-zero flood threat however it’s not lined by a FEMA flood map (both a 100-year flood, 500-year flood, or floodway map). We think about a property “probably unmapped” if it faces any non-zero flood threat with out flood map protection.

Many properties with flood threat are certainly lined by a flood map, together with many of the properties with the very best attainable threat. Nevertheless, a considerable variety of properties face flood threat however should not lined by a flood map. Of the properties within the prime percentile of the flood threat distribution, a 3rd (36 p.c) should not lined by a flood map; within the prime 5 p.c of the flood threat distribution, half of all properties (48 p.c) should not lined by a flood map; and within the prime ten p.c of the flood threat distribution, three-quarters (74 p.c) should not lined by a flood map.

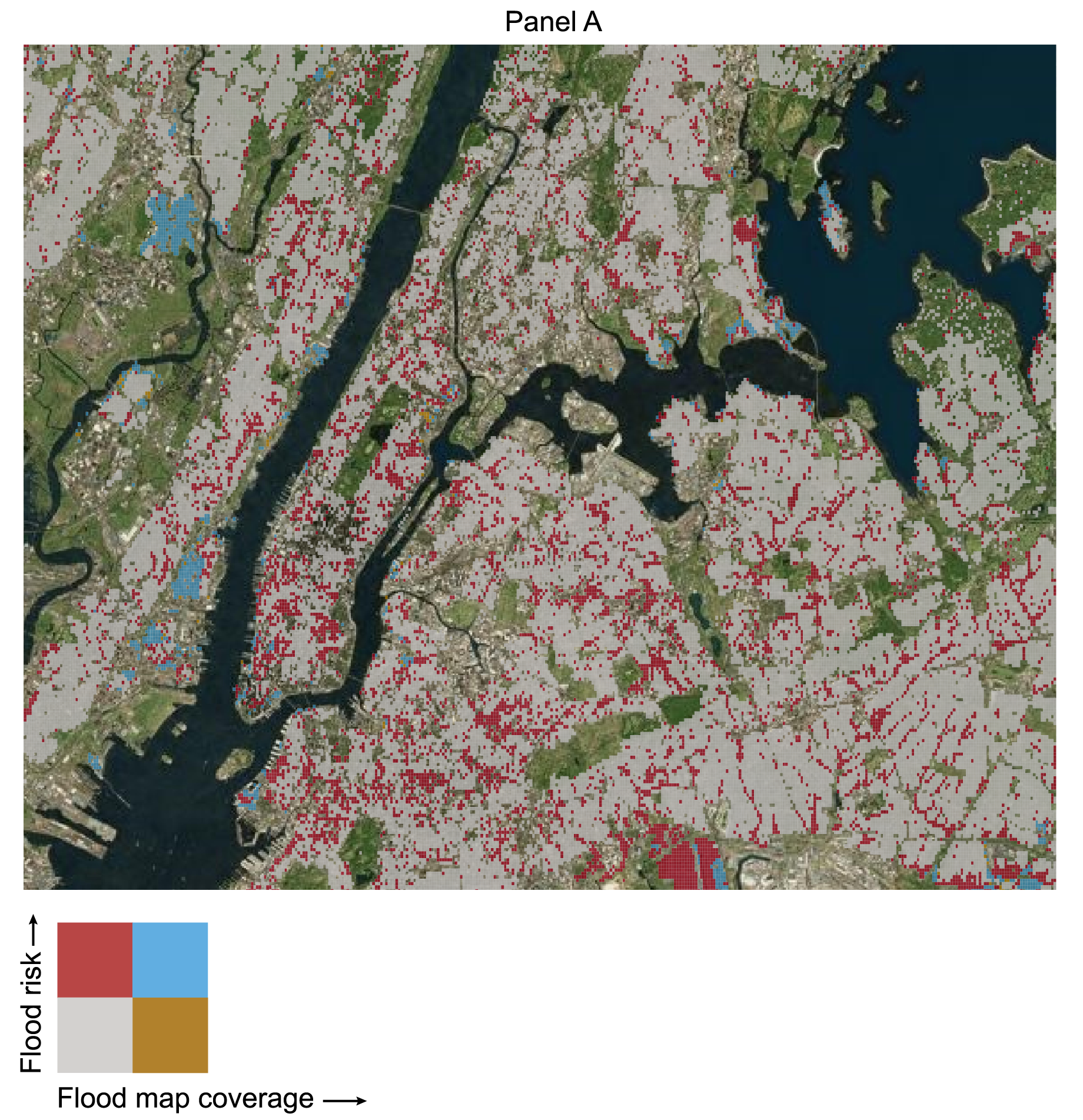

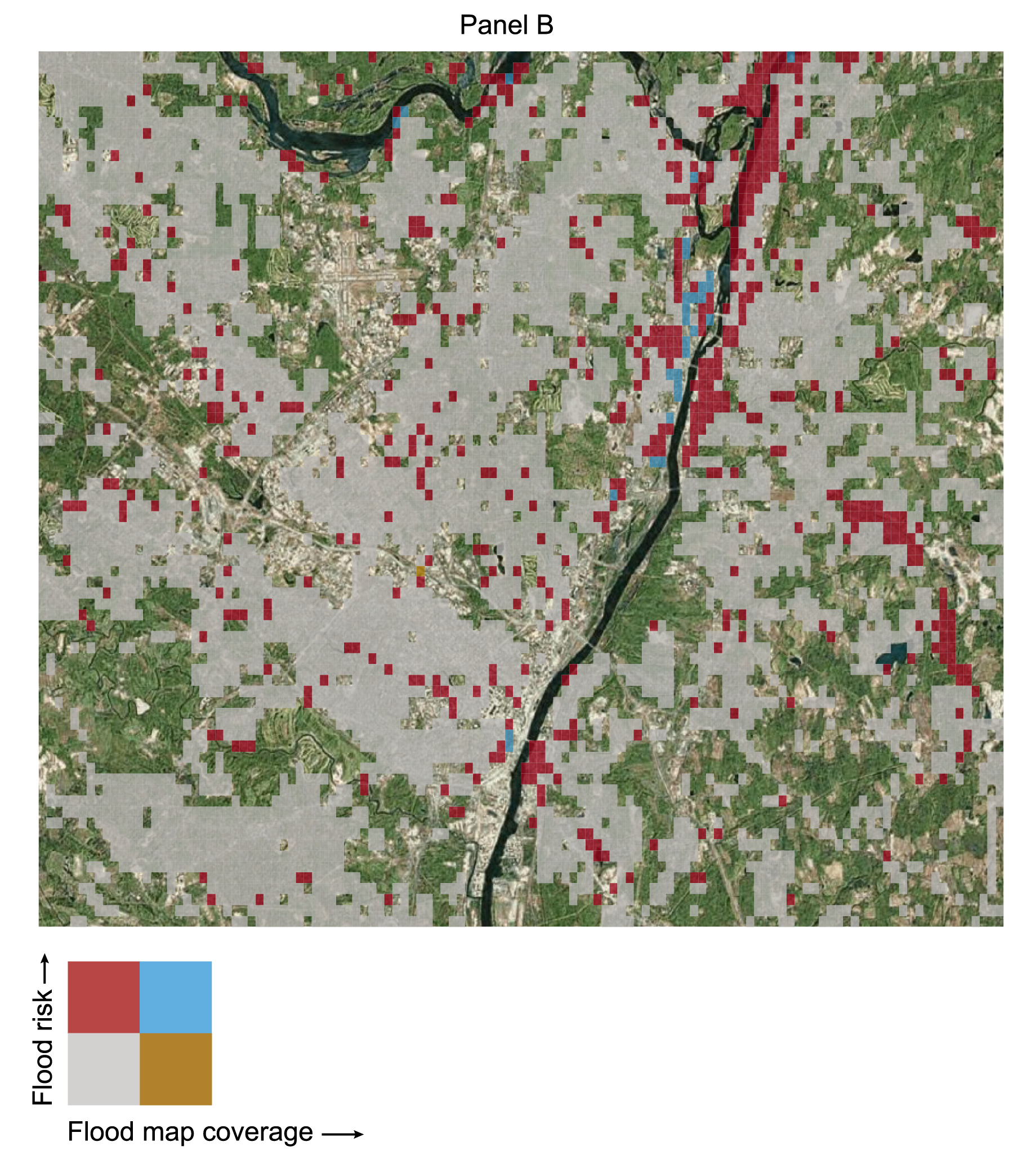

The maps under present an instance of those properties with unmapped flood threat in two areas throughout the Federal Reserve’s Second District. Panel A maps New York Metropolis and the encompassing metropolitan space, and Panel B maps a portion of the Hudson River because it passes via the cities of Albany and Troy, New York. For every map, we overlay a grid and shade the cells in response to flood map protection and the typical flood threat of properties within the cell. Unmapped areas, with flood threat however no flood map protection, seem in crimson. Our evaluation focuses on learning lending variations between these properties with excessive flood threat and no flood map (the crimson cells) and people properties with low flood threat and no flood map (the grey cells).

Unmapped Flood Danger within the Federal Reserve’s Second District

Sources: Authors’ calculations; FEMA; CoreLogic; Esri.

Notes: Panel A exhibits flood map protection and flood threat in a 0.001⁰ × 0.001⁰ grid over New York Metropolis. Panel B exhibits flood map protection and flood threat in a 0.0025⁰ × 0.0025⁰ grid over Albany and Troy, New York. Solely grid cells that cowl a minimum of three properties within the knowledge set used within the evaluation are coloured. The information set consists of solely residential properties. Grey areas have low flood threat and no flood map protection. Pink areas have flood threat however no flood map protection. Blue areas are precisely mapped. Within the evaluation, mortgage origination for properties in grey areas are in comparison with properties in crimson areas.

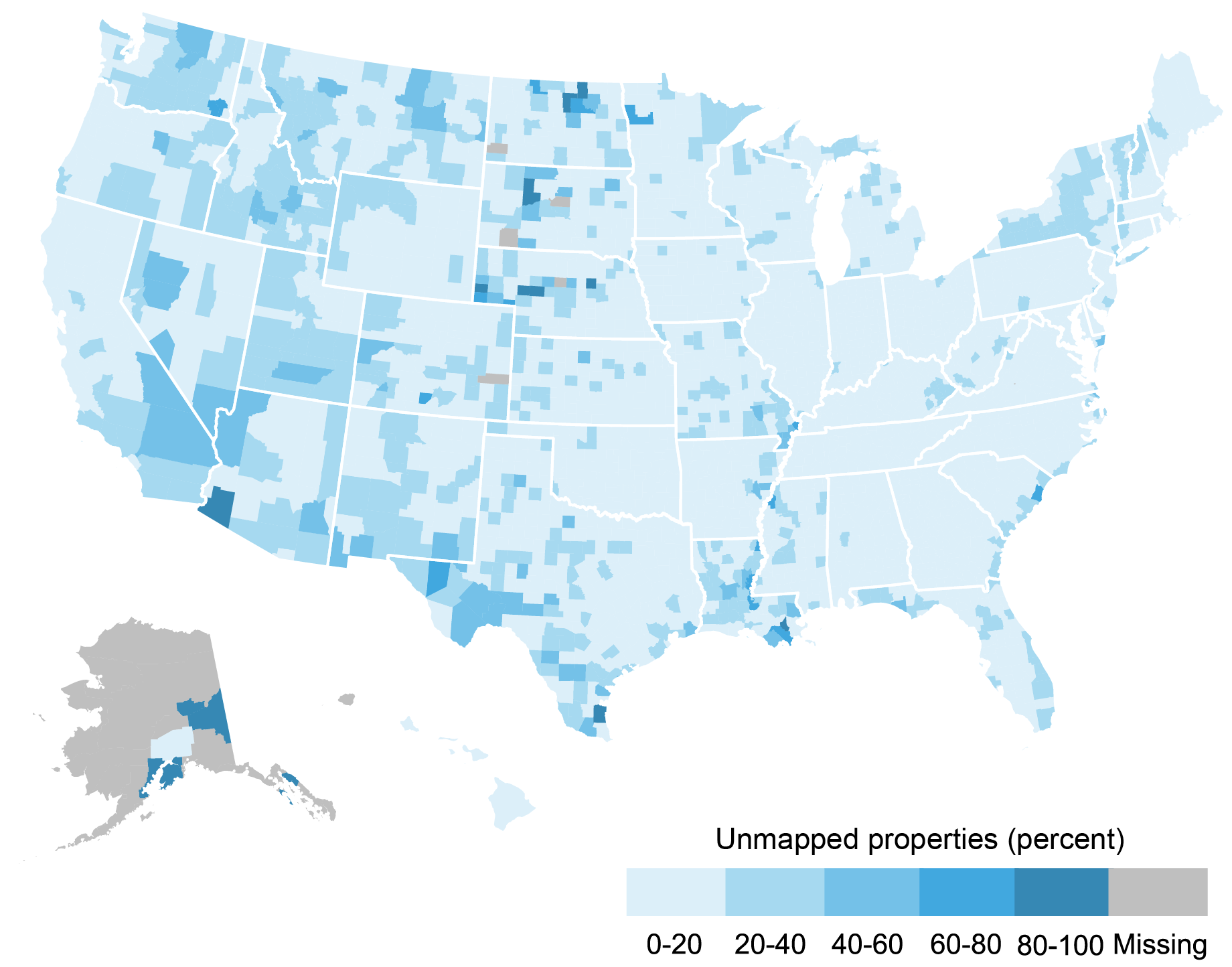

Within the map under, we plot the distribution of unmapped properties throughout the U.S. on the county degree. This exhibits the share of all properties in a county that we establish as having unmapped flood threat. As will be seen, unmapped properties will be discovered all through the nation—particularly alongside coasts, main rivers, and meltwater runoff paths.

Unmapped Flood Danger Nationwide

Sources: Authors’ calculations; FEMA; CoreLogic.

Notes: The map exhibits, on the county degree, the share of properties categorised as having unmapped flood threat.

In our analyses, we examine whether or not mortgage lenders are conscious of unmapped flood threat on the property degree and whether or not they reply to this threat accordingly. We prohibit our mortgage-property pattern to solely these main buildings on a parcel we will precisely match to geocoded HMDA knowledge, solely mortgage functions made with the aim of shopping for a house, and solely loans throughout the native conforming mortgage restrict. Additional, we exclude properties lined by a FEMA flood map to concentrate on evaluating related properties, purchased by related candidates, throughout the similar small census tract—differenced by whether or not the construction faces flood threat. Our remaining pattern accommodates greater than 13 million mortgage functions.

Much less Lending in Dangerous Areas

We first relate mortgage origination selections to a bunch of applicant, financial institution, and area traits. Our variable of curiosity is whether or not the property itself is unmapped. We take a look at the broader “probably unmapped” in addition to the extra sure “unmapped.” These classes are cumulative in that every one “unmapped” properties are routinely “probably unmapped” as nicely.

Impact of Unmapped Flood Danger on Mortgage Originations

Share level lower in originations

Notes: The above determine exhibits the important thing coefficients of our regression evaluation that relates mortgage and borrower traits as to if or not a mortgage is originated. It depicts the affect of households being absolutely or “probably” un-mapped. The impacts of being un-mapped or probably un-mapped are cumulative. As we go from specification 1 to specification 4, we embrace further controls. Specification 1 consists of primary lender controls and county traits; Specification 2 provides mortgage controls together with mortgage measurement. Specification 3 consists of all of the above and provides county × time fastened results, accounting for any time-varying traits on the county degree. Lastly, specification 4 consists of census tract and lender controls. Specification 4 subsumes all lending responses that happen on the tract-level.

We will see from the chart that mortgages are much less more likely to be originated if the property faces unmapped threat. In reality, all else equal, an unmapped property is about 1 proportion level much less more likely to have a mortgage originated than properties not in danger (specs 1 and a couple of). If we evaluate properties inside a census tract versus wider geographic areas, the impact is diminished (specification 4). It appears that evidently whereas banks handle flood threat, some banks take a census tract-level—versus a property-level—method to flood threat administration.

We will embrace interactions with bank-type or region-type dummies. First, we use native incomes as a measure to separate our pattern into three teams of census tracts (low, mid, and excessive revenue). We discover that high-income tracts endure a much less extreme discount in lending. This doubtless displays the truth that lenders count on rich debtors to higher (financially) climate a storm or a flooding catastrophe. The results are rather more pronounced in areas with decrease revenue (roughly twice as massive because the baseline impact). Second, we take a look at whether or not several types of entities are more likely to lend regardless of the chance. We discover that nonbanks and native banks are nonetheless originating loans even when properties face flood threat. Very massive banks are much less more likely to lend.

It’s attainable that giant banks have extra subtle threat administration approaches than smaller banks or nonbanks, which permits them to establish at-risk properties extra precisely. Subsequently, we moreover take a look at whether or not banks offered or securitized loans. We discover that lenders are typically extra more likely to securitize or promote properties that face unmapped flood threat. Whereas the typical lender is 1 proportion level extra more likely to securitize properties with unmapped threat, there are important variations between lender sorts. Usually, small native banks are greater than 2 proportion factors extra more likely to promote or securitize a mortgage with unmapped flood threat. Given the widely excessive propensity of those lenders to securitize conforming properties, even a small enhance represents important further effort on the a part of lenders to maneuver the loans off of their stability sheets.

Summing Up

We create a novel property-level flood threat and mortgage utility knowledge set to point out that lenders are conscious of flood threat outdoors of FEMA flood zones. Bigger lenders considerably lower lending whereas smaller native banks and nonbank entities don’t cut back lending however as an alternative usually tend to securitize or promote loans and transfer them off of their stability sheets.

Kristian Blickle is a monetary analysis economist in Local weather Danger Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Evan Perry is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

João A.C. Santos is the director of Monetary Intermediation Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Tips on how to cite this publish:

Kristian Blickle, Evan Perry, and João A.C. Santos, “Flood Danger Exterior Flood Zones — A Take a look at Mortgage Lending in Dangerous Areas,” Federal Reserve Financial institution of New York Liberty Road Economics, September 25, 2024, https://libertystreeteconomics.newyorkfed.org/2024/09/flood-risk-outside-flood-zones-a-look-at-mortgage-lending-in-risky-areas/.

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).