Housing affordability stays a essential challenge, with 74.9% of U.S. households unable to afford a median-priced new house in 2025, based on NAHB’s newest evaluation. With a median value of $459,826 and a 30-year mortgage fee of 6.5%, this interprets to round 100.6 million households priced out of the market, even earlier than accounting for additional will increase in house costs or rates of interest. A $1,000 improve within the median value of latest properties would value a further 115,593 households out of the market.

The 2024 priced-out estimates for all states and the District of Columbia and over 300 metropolitan statistical areas are proven within the interactive map beneath. It highlights the rising housing affordability challenges throughout the US. In 23 states and the District of Columbia, over 80% of households are priced out of the median-priced new house market. This means a major disconnect between rising house costs and family incomes.

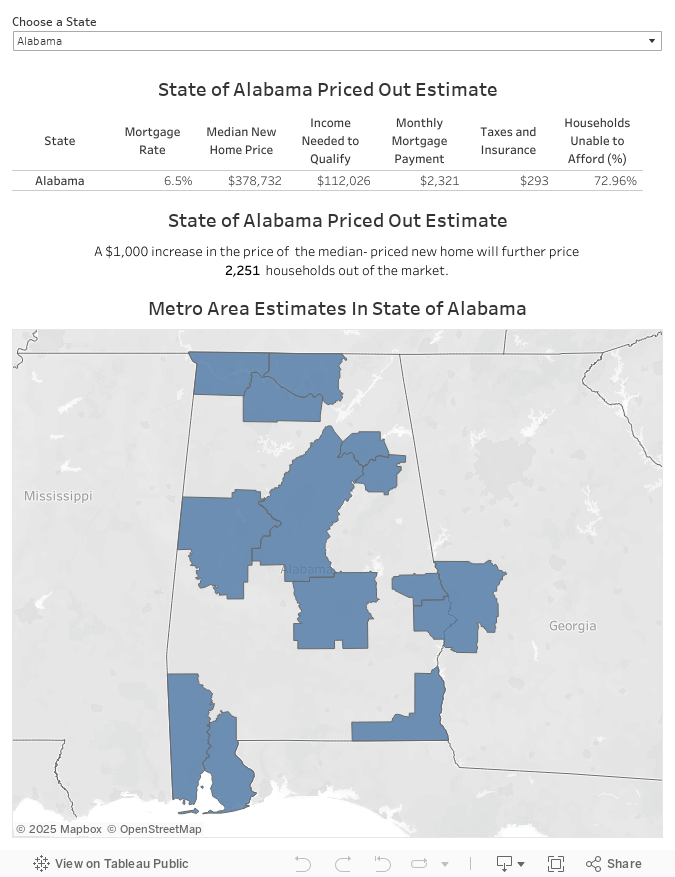

Maine stands out because the state with the best share of households (91.2%) unable to afford the state’s median new house value of $682,223. Excessive-cost states equivalent to Connecticut and Rhode Island observe intently, with 88.3% and 87.8% of households, respectively, struggling to afford new properties. Even in states with comparatively decrease median new house costs, affordability stays a serious concern. For instance, in Mississippi, the place the median house value is $275,333, 70.2% of households nonetheless discover these new properties out of attain. In the meantime, Delaware, the state with higher affordability within the evaluation, has a median new house value of $373,666. Nevertheless, round 58.2% of households in Delaware nonetheless battle to afford a brand new house. Even modest value will increase, equivalent to a further $1,000, might push hundreds extra households from affording these median priced new properties. For example, in Texas, such a rise might value out over 11,000 households.

It additionally exhibits the 2025 priced-out estimates for over 300 metropolitan statistical areas. The evaluation estimates what number of households in every metro space earn sufficient earnings to qualify for mortgages on median-priced new properties. In high-cost areas just like the San Jose-Sunnyvale-Santa Clara, CA metro space, the place new properties largely goal high-income Silicon Valley residents, solely 10% of all households meet the minimal earnings threshold of $437,963 required to qualify for a mortgage on a median priced new house. In distinction, in additional reasonably priced metro areas like Sierra Vista-Douglas, AZ, the place the median new house value is $150,893, practically two-thirds of households can afford a median priced new house. Whereas greater house costs typically end in greater month-to-month mortgage funds and better earnings thresholds, the connection between house costs and affordability just isn’t at all times linear. Components like property taxes and insurance coverage funds may considerably influence month-to-month housing prices, including complexity to affordability calculations.

The affordability of latest properties along with the inhabitants dimension of a metro space, considerably affect the priced-out influence of a $1,000 improve in new house costs. In metro areas the place new properties are already unaffordable to most households, the impact of such a rise tends to be small. For example, within the San Jose-Sunnyvale-Santa Clara, CA metro space, a further $1,000 improve to the house value impacts solely 259 households, as solely 10% of all households might afford such costly new properties within the first place. Right here, the extra value improve solely impacts a slim share of high-income households on the higher finish of the earnings distribution, the place affordability is already stretched.

In distinction, metro areas, the place new properties are extra broadly reasonably priced, expertise a bigger priced-out impact. A $1,000 improve within the median new house value impacts a bigger share of households within the “thicker half” of the earnings distribution. For instance, within the Dallas-Fort Price-Arlington, TX metro space, a $1,000 improve in new house value would disqualify 2,882 households from affording a median-priced new house. That is the biggest priced-out impact amongst all metro areas, pushed by the mixture of comparatively average house costs and a considerable inhabitants base.

Extra particulars, together with priced-out estimates for each state and over 300 metropolitan areas, and an outline of the underlying methodology, can be found within the full examine.

Uncover extra from Eye On Housing

Subscribe to get the most recent posts despatched to your e mail.