I do know we only in the near past acquired a 5-handle for the 30-year mounted after a number of years in a lot greater territory.

However is it too quickly to speak about 4% mortgage charges?

The rationale I ask is as a result of I’m seeing some aggressive price quotes which might be already practically there.

So if we get some extra favorable financial information and/or we hear extra on proposals just like the MBS shopping for, we may get the nudge wanted to get them.

If it had been to occur quickly, through the conventional spring house shopping for season, it could possibly be massive.

The Return to five% Mortgage Charges Took Years

Ultimately look, the 30-year mounted was averaging 6% on the nostril, per the newest learn from Mortgage Information Every day.

It loved two days at 5.99% earlier than ticking up a single foundation level, and chances are high it would tick again down to five.99% right this moment.

Certain, it’s not a very a 5% mortgage price, however a 5-handle mortgage price.

In different phrases, it begins with a 5, nevertheless it’s far cry from 5%.

If it had been 5%, there’d seemingly be a mad rush to purchase houses once more, although anecdotally I’m already listening to of bidding wars heating up once more.

However right here’s an essential level. The speed indexes like MND’s merely symbolize composite mortgage charges for the market.

Put one other means, a snapshot of the lender universe on any given day, principally helpful to trace day-to-day motion versus actual charges.

That is to say that if their index says 5.99%, there are debtors on the market securing even decrease charges (or in some circumstances greater charges).

One Massive Financial institution Is Almost within the 4% Vary for a 30-Yr Fastened

That brings me to a giant financial institution I examine in on now and again, which simply so occurred to offer charges tremendous shut the 4s.

Once more, we’re speaking a 4-handle, aka 4.99%, not a 4% mortgage price. And once more, if charges had been 4%, it’d seemingly be a madhouse on the market between surging refinance purposes and bidding wars.

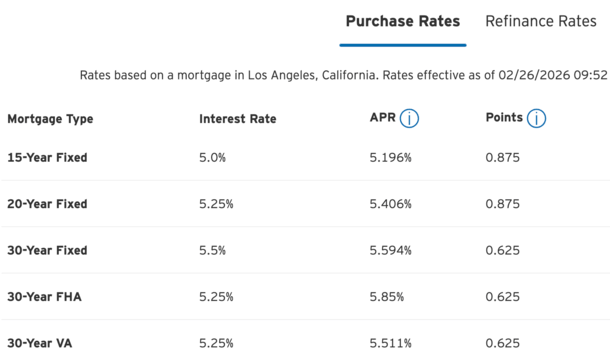

As a substitute, I’m seeing price quotes of 5.25% for each FHA loans and VA loans (that are all the time the most cost effective mortgage choices), and 5.5% for a conforming mortgage (Fannie/Freddie) 30-year mounted.

They’re additionally promoting a 15-year mounted at 5% even, that means only one foundation level above the 4s. And a 20-year mounted at 5.25%, not far both.

In different phrases, virtually into the 4s throughout quite a few completely different mortgage packages.

So in actuality, there are lots of decrease mortgage price quotes swirling round, properly beneath the nationwide averages we see within the headlines.

Notably, none of those charges even require a large buydown (low cost factors) to get the deal.

These days, lenders have tried to lure in debtors with closely bought-down charges that always require 1.5% to 2% in factors.

That may be tremendous costly since one level prices $1,000 for each $100,000 in mortgage quantity.

However these charges principally require a fraction of low cost factors, whether or not it’s 0.625% or 0.875%.

Certain, it’s nonetheless not free, nevertheless it’s fairly affordable, particularly for those who can get vendor concessions and use these for these closing prices.

4-Deal with Mortgage Charges Would Be Massive for the Housing Market Restoration

Whereas we’re not fairly there but, the truth that some banks and lenders are already providing charges within the low-to-mid 5s is promising.

It means precise price quotes and eventual price locks will are available in considerably decrease than the nationwide averages we see within the information.

It will make housing that rather more inexpensive for potential house patrons, whereas additionally giving extra current owners the chance to make the most of a price and time period refinance.

If we proceed to obtain favorable financial information, similar to decrease inflation, or see extra flights to security (in bonds) because the inventory market corrects, mortgage charges may transfer decrease.

There are additionally pending initiatives like Fannie and Freddie’s $200 billion MBS shopping for program that would give charges slightly push down as properly.

And that would imply that a few of these quotes which might be already close to the 4s may ultimately get there.

So whereas everybody talks about 5% mortgage charges, it may not be unparalleled to listen to about debtors snagging charges within the 4s once more!

Simply know that you simply’ll seemingly want a vanilla mortgage situation, that means an owner-occupied property, wonderful credit score rating, low loan-to-value ratio (LTV), and many others.

Learn on: 2026 Mortgage Price Predictions

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) house patrons higher navigate the house mortgage course of. Observe me on X for decent takes.