In some way mortgage charges went from being one of the best since 2022 to the worst this 12 months, all within the span of a couple of week and alter.

Speak about a tough stretch for mortgage charges, pushed by the continuing (and unsure) battle within the Center East.

The lengthy and the in need of it’s that oil costs have skyrocketed in response, resulting in renewed inflation issues.

When inflation is anticipated to worsen, the worth of bonds (and mortgage-backed securities) erodes.

Because of this, the yield (or rate of interest) will increase to offset the drop in value. And that’s why mortgage charges are the very best they’ve been all 12 months.

Mortgage Charges Hit Highest Level of the 12 months

Issues had been trying actually good for mortgage charges by way of the primary two months of the 12 months.

The 30-year mounted hit its lowest level since round late summer time of 2022.

Two weeks in the past, Freddie Mac reported that the favored mortgage hit its lowest level in 3.5 years, averaging 5.98% based on their lender survey.

Every week later it had climbed again into the sixes, however to six.00% precisely, which was nonetheless a beautiful fee.

Tomorrow they’ll launch their subsequent weekly survey, but it surely in all probability received’t seize all of the upward motion seen previously 24 hours.

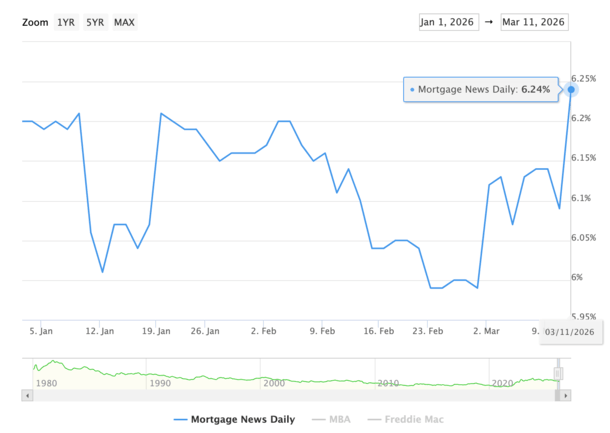

The every day up to date fee index from Mortgage Information Day by day initially rose to six.19% this morning, then acquired an unfavorable noon re-price to six.24%.

That places it 4 foundation factors above the prior 2026 excessive of 6.21%, per MND.

The excellent news is we’re nonetheless speaking a couple of handful of foundation factors, which aren’t quite a bit.

In actual fact, the rate of interest could be the identical however merely value a bit of extra at closing.

And the month-to-month cost in all probability isn’t a lot totally different at 6.25% versus 6%.

On a $500,000 mortgage, it’s truly solely a distinction of $80 per 30 days in principal and curiosity.

However to the potential residence purchaser, it would feel and look quite a bit worse.

I preserve speaking about this and it’s massively vital. It’s all about purchaser psychology.

Should you go purchase an enormous display screen TV and the worth was $999 however is now $1,075, you’re going to really feel such as you acquired a uncooked deal.

You may nonetheless undergo with it, but it surely’s going to rub you the improper manner.

Now think about a mortgage, the place that larger fee stares at you every month for doubtlessly the subsequent decade or longer.

Not an important feeling and clearly it prices you more cash too!

How Unhealthy Can Mortgage Charges Get, Once more?

As I’m penning this, I’m considering of these annoying 7% mortgage charges once more that stored re-emerging time and time once more these previous few years.

We appeared to lastly shake these final spring and hopefully they don’t return anytime quickly.

I don’t assume it will get fairly that unhealthy as a result of at a sure level persistently costly oil costs would possible usher in a recession. Woo hoo!

And also you’d assume we’d get decrease bond yields if that had been the case, because the 10-year tends to fall throughout downturns.

Nevertheless, we may see 30-year mounted mortgage charges proceed to rise if the present scenario deteriorates and there’s not the standard flight to security due to oil costs.

In different phrases, within the close to time period we may see the 30-year mortgage soar again towards 6.50%, whereas sustaining upward stress and a resistance to fall again to latest ranges.

Keep in mind, charges take longer to fall than they do to rise. So as soon as they go up, they will get caught there for some time.

Crucially, that is taking place throughout peak residence shopping for season, which means they won’t have the ability to return to these tasty 5-handle ranges till maybe after summer time at this level.

(picture: Topher McCulloch)

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Comply with me on X for decent takes.