We closed yesterday’s submit with the statement that financial idea doesn’t actually have a great grip on the place rates of interest come from. Right now, I need to discover the place we expect charges come from and what that may imply.

Does the Fed Management Charges?

The primary, and easiest, means to take a look at rates of interest is to conclude that the central banks set them. This, in any case, is the underlying assumption behind the breathless protection of the newest coverage strikes by the Fed or the European Central Financial institution. A headline like “Fed cuts charges” means one thing provided that the Fed really controls charges.

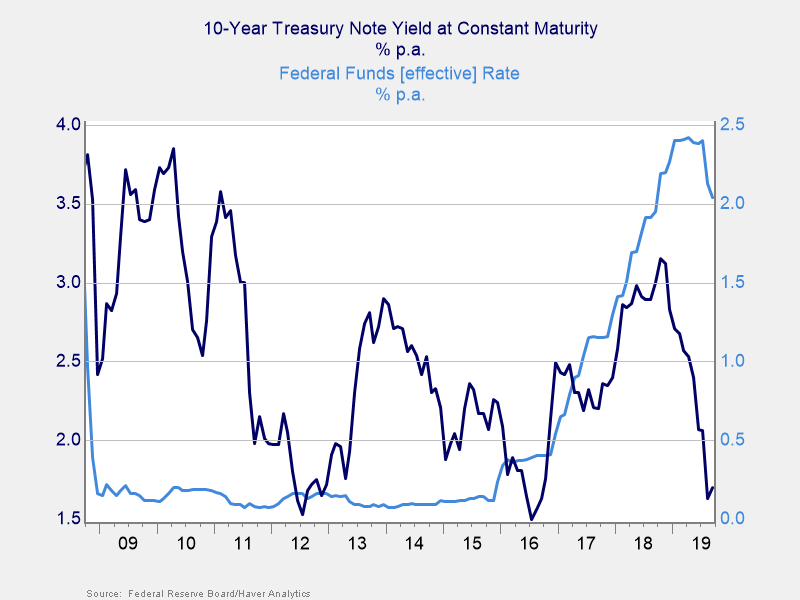

Wanting on the knowledge, although, it’s clear the Fed doesn’t have management right here. From 2009 by means of 2016, the Fed saved charges at all-time low, however longer-term charges bounced round significantly. The Fed little doubt had an affect, however it took years to work. And even when it gave the impression to be working (i.e., in 2016 by means of 2018, when longer charges lined up with Fed coverage charges)? We noticed that relationship blow up once more in late 2018 as longer charges dropped once more as Fed charges went up. In current months, the Fed has been following not main. The “Fed controls charges mannequin” merely doesn’t work over any time-frame shorter than a few years.

The Fed is conscious of this dynamic, after all. What it’s attempting to do is sign and to exert that affect over a interval of years. The Fed can’t—and doesn’t—set charges immediately.

It is a good factor. When you consider it, the notion that the Fed units charges is type of an odd assumption. Rates of interest are the muse of the monetary system. So the concept that they’re set by a central planning board—the “Supreme Soviet,” because it have been—is solely bizarre. If we’re good capitalists and good economists, we’d count on rates of interest, as the worth of cash, to be set within the capital markets, on the intersection of provide and demand.

The Intersection of Provide and Demand

Which brings us to the second main mannequin for the place rates of interest come from: the intersection of provide and demand of capital. Merely, if extra capital is accessible and if demand is fixed, then charges ought to decline. This concept offers a really affordable mannequin for why charges have been declining for many years (which, should you bear in mind, is what we are attempting to clarify right here).

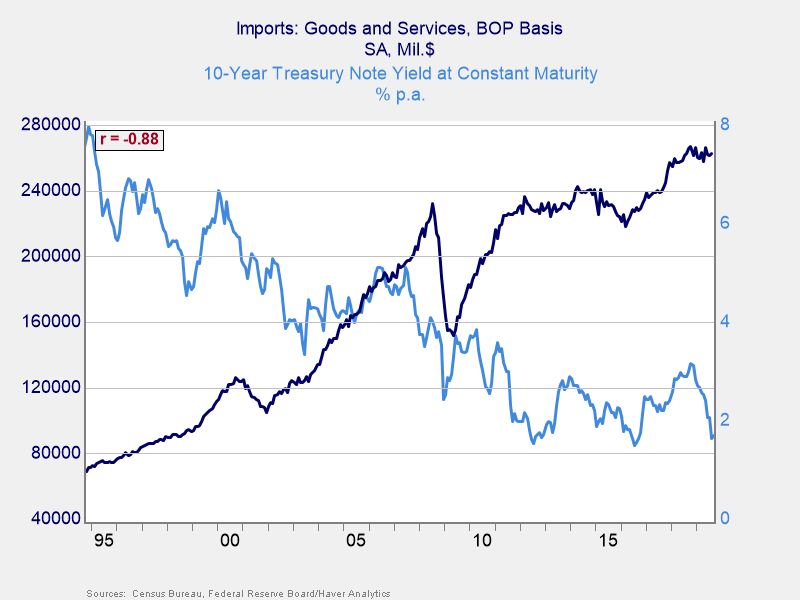

This mannequin makes a number of sense over that time-frame. Rising imports to the U.S. created a necessity for the exporters to recycle their capital in greenback belongings—U.S. Treasuries. Rising imports, subsequently, led to extra capital coming again to the U.S. You may see a close to 90 % correlation between charges and imports over that point interval, which is extremely excessive for financial knowledge. A bigger provide of capital led to decrease price of capital, simply as idea predicts. If you have a look at the numbers, you could have greater than $2 trillion in Treasuries between China and Japan, and extra held by different exporters. That’s capital the U.S. wouldn’t have had entry to, and it represents appreciable further provide.

This mannequin clearly has some explanatory energy, however it additionally has issues. It doesn’t, for instance, clarify the gaps between the U.S., Europe, and Japan. It additionally doesn’t clarify the current declines in charges. With international commerce rolling over and with the U.S. commerce warfare hitting imports (see the chart beneath), the provision of extra capital is declining, which ought to imply charges go up. As an alternative, we’re seeing them go down once more.

Clearly, there’s something else happening.

The Lacking Piece

Each of those fashions—central financial institution management and provide and demand—seize a part of the story. We’d like one other piece, nonetheless, to clarify the gaps between markets and the current declines. I believe that one thing else is non-economic, particularly, demographics. Tomorrow, we are going to have a look at how I received to that conclusion and what it may imply for the longer term.

Editor’s Notice: The authentic model of this text appeared on the Unbiased Market Observer.