Recently, I’ve seen numerous posts on social media from householders complaining that their escrow account is brief.

And that their month-to-month housing funds might want to go up X {dollars} per 30 days to cowl the shortfall.

It’s both being pushed by rising property taxes or increased insurance coverage premiums. Or in some unlucky instances, each!

To keep away from this variation in month-to-month mortgage cost, you possibly can handle taxes and insurance coverage by yourself as an alternative.

However how do you eliminate an current escrow account?

Get Rid of Escrow on a Mortgage

- Escrow accounts guarantee well timed cost of taxes and insurance coverage

- Usually required while you take out a brand new house mortgage

- However will be eliminated if strong cost historical past and low LTV

- Price is usually charged (both flat payment or % of mortgage steadiness)

Many lenders require debtors to open an escrow account after they take out a mortgage.

That is particularly pertinent for these placing little down because it ensures the well timed cost of property taxes and householders insurance coverage.

Since each of those prices will be fairly costly, an escrow account ensures funds are collected month-to-month and distributed when the funds are due.

It’s all executed robotically through the escrow account so the mortgage servicer doesn’t want to fret a few home-owner forgetting to pay.

In case you’ve ever heard the acronym PITI, it stands for principal, curiosity, taxes, and insurance coverage.

When you may have an escrow account, you pay all 4 elements every month, after which the T&I are disbursed when due.

In case you don’t have an escrow account, you merely pay the P&I every month to your mortgage servicer, and self-manage the T&I portion.

However what if you wish to eliminate your escrow account and self-manage? Effectively, it is dependent upon your servicer and in addition your mortgage sort.

You May Should Pay a Price to Take away an Escrow Account

Some mortgage servicers will cost you a payment to take away an escrow account.

This might be a flat payment, corresponding to $250, or alternatively a share of the excellent mortgage steadiness.

Both manner, it’s typically not free. And in case you attempt to waive impounds (completely different title for escrow) when acquiring a house mortgage, you may additionally should pay a small payment as nicely.

This might be one thing like .125% of the mortgage quantity, or $625 on a $500,000 mortgage.

The explanation there may be typically a payment is as a result of it’s decrease threat to have an escrow account in place.

As famous, it ensures well timed cost of taxes and insurance coverage. Think about if somebody didn’t put aside the mandatory funds, or forgot to pay, and so on.

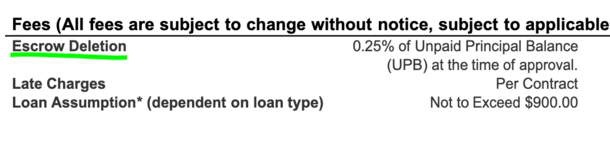

To find out how a lot it would price you to take away escrows after you may have your mortgage, discover your newest mortgage assertion and scroll down into the high-quality print space.

You must see one thing about “Escrow Deletion” or comparable. Certainly one of my explicit lenders costs 0.25% of the unpaid principal steadiness (see above).

So in case you’ve acquired $200,000 remaining in your mortgage, that’d be $500! At that time, you’d in all probability say it’s not price it.

In any case, what’s the upside to self-managing these funds? You may have the ability to earn a bit of additional curiosity in a high-yield financial savings account?

However this may range by mortgage servicer and even by state. Additionally observe that you have to have a strong cost historical past and sometimes a low loan-to-value ratio (LTV) corresponding to sub-80% or higher.

The corporate could then assessment your mortgage and decide in case you’re eligible to shut the escrow account.

Tip: An escrow account is required on FHA loans for the lifetime of the mortgage and may’t be eliminated. Similar goes for USDA loans and whereas not a mandate for VA loans, most lenders nonetheless require it.

Why a Mortgage Escrow Account Is a Good Factor

Now earlier than you get upset that it’s a must to pay a payment to take away escrows, or discover out they will’t be eliminated in any respect, think about this.

The well timed cost of property taxes and householders insurance coverage is clearly factor.

And taking a bit of out every month and paying it in your behalf ensures you received’t miss these essential funds.

It additionally acts as a self-budgeting instrument the place you don’t have to fret about these huge funds yearly or semi-annually.

As a substitute, the mortgage servicer won’t solely price range for you, but in addition maintain the remittance.

Everyone knows it may be onerous to price range, so whereas it is likely to be “annoying” to should pay into your escrow account month-to-month, it could truly enable you keep away from larger issues.

I personally don’t thoughts paying into an escrow account because it helps me keep away from the shock of a giant property tax invoice or insurance coverage premium.

As well as, the mortgage servicer will carry out an escrow evaluation every year and earmark further funds if essential to cowl any anticipated improve (escrow scarcity).

Positive, your mortgage cost will go up in consequence, nevertheless it might be higher than getting a shock proper earlier than these funds are due!

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) house patrons higher navigate the house mortgage course of. Observe me on X for warm takes.