For those who’re hoping for decrease mortgage charges, you is perhaps thrilled to listen to what Treasury Secretary Scott Bessent has to say.

Throughout a tv interview right this moment, he stated “a sequence of price cuts” could possibly be on the desk, together with a giant 50-basis level lower in September.

That might mirror the lower seen final September when mortgage charges occurred to go up. In fact, the Fed and mortgage charges have a sophisticated relationship.

So those that assume Fed lower = decrease 30-year mounted is perhaps in for a shock.

Nonetheless, Bessent added that the September lower could possibly be the primary of many…

Bessent Says Charges Ought to Be 150 to 175 Foundation Factors Decrease

Talking right this moment on Bloomberg, Treasury Secretary Bessent argued for larger price cuts than what’s at present forecast.

For starters, he believes the September Fed price lower, at present a lock at 99.9% on CME, needs to be not 25 foundation factors however as an alternative 50 foundation factors.

The backdrop there’s that he suspects we might (ought to) have reduce in June and July, however didn’t. So in essence enjoying a bit little bit of catch up.

In fact, that is all predicated on that actually ugly jobs report we acquired for July, which included huge downward revisions for June and Could.

Had that not come, it’d be onerous to fathom anybody speaking a few 50-bp price lower, or maybe even a 25-bp price lower.

In actual fact, CME had odds of a quarter-point price lower at simply 57.4% one month in the past, simply as an instance how fluid this all is.

Now there’s phrase of eradicating the month-to-month jobs report till it may be confirmed to be correct.

This was a suggestion from E.J. Antoni, who changed fired Bureau of Labor Statistics (BLS) commissioner Erika McEntarfer after that mess of a report.

However Bessent believes that’s simply the beginning, and that “we must always in all probability be 150, 175 foundation factors decrease.” Whoa!

The Fed Funds Price Isn’t Mortgage Charges

I’ve stated this one million instances, however it bears repeating. The Fed doesn’t set client mortgage charges.

Once they lower, mortgage charges might go up, sideways, or down. Identical in the event that they hike. The correlation isn’t all that sturdy.

The one actual argument you may make is Fed price expectations correlate considerably with mortgage charges.

So in the event that they’re planning to chop, long-term mortgage charges can drift decrease too. However, and it’s an necessary however, you want the financial knowledge to assist the transfer decrease.

Whereas the Fed might feasibly lower its personal fed funds price, it’s unclear how bond yields would react, particularly and not using a month-to-month jobs report leaving them at the hours of darkness.

Bonds are purported to be a secure haven, and with a lot uncertainty within the air, it’d be onerous to think about any main actions there till there’s extra readability.

Nonetheless, the 10-year bond yield did slip practically six foundation factors right this moment, which is perhaps a mirrored image of lowered inflationary fears associated to tariffs.

That might put all eyes on the labor market, which is what acquired this newest mortgage price rally going within the first place.

And could possibly be the underlying purpose why people like Bessent are calling for these sizable price cuts.

Is Bessent signaling that not all is nicely within the economic system, even when the administration argues that the economic system is scorching?

In the end, continued job losses and better unemployment is what would get mortgage charges even decrease.

It’s clearly a double-edged sword, as you’d have extra households underneath stress, which type of takes away from the anticipated windfall of decrease charges.

However that’s type of the factor with charges. They have a tendency to return down with unhealthy financial instances and vice versa.

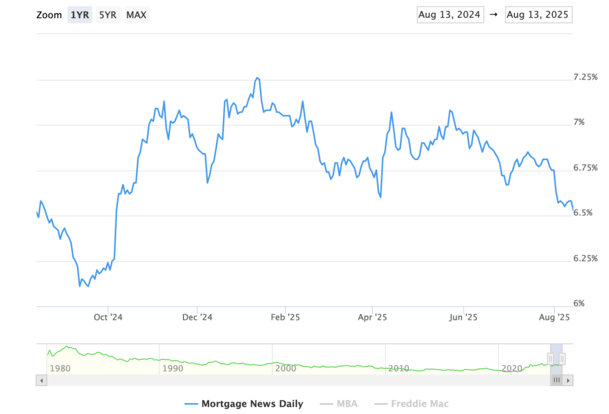

Mortgage Charges Already Lowest Since Early October

Because it stands now, 30-year mounted mortgage charges are the bottom they’ve been since early October. They’re practically again to September ranges, per MND.

So Fed price expectations and weak financial knowledge may already be principally baked in. Charges can go decrease, however want a purpose (much more financial weak spot).

Perhaps they’ll get again there this September, when the 30-year mounted was hovering nearer to six% than 6.5%.

That would definitely result in a decide up in mortgage refinancing, and doubtlessly residence shopping for as nicely.

We noticed a mini refi increase again then, which solely acquired lower quick as a consequence of a scorching jobs report, sarcastically.

Maybe we’re unwinding that transfer a yr in the past and getting again to the narrative that the labor market is cracking and the economic system is cooling.

All this regardless of fears of inflation rising once more as a consequence of tariffs, or just extra companies elevating costs as they handle rising prices.

That is the place that stagflation concept is available in. Slowing progress, greater unemployment. It’s actually potential.

But it surely seems this administration, who can also be seeking to make the Fed much more accommodative as soon as Powell’s time period is over, is fixated on chopping charges.

If nothing else, this implies HELOC charges will come down, as they’re straight tied to the prime price, which is dictated by the federal funds price.

It might additionally make adjustable-rate mortgages cheaper, as they’re short-term loans in contrast to the 30-year mounted.

The large query is that if this coverage route places us at better threat of inflation reigniting. Or if the administration sees the writing on the wall, that the economic system is in dire want of assist.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Observe me on X for warm takes.