TVS Motor Firm Ltd – Shaping Tomorrow’s Mobility As we speak

Included in 1992 and headquartered in Chennai, TVS Motor Firm Ltd (TVSM) is a globally acknowledged producer of two and three wheelers (2 & 3W). The corporate has presence in 80+ international locations throughout Center East, Africa, SE Asia, Indian Subcontinent, Latin and Central America. Backed by 5 manufacturing amenities in India (positioned in Hosur, Mysuru and Nalagarh) and one every in Indonesia & UK, the corporate is at the moment the third largest 2W producer in India and fourth largest on the earth. The corporate can also be within the enterprise of financing of two wheelers, used vehicles, used and new tractors, used industrial automobiles, shopper durables, digital finance merchandise, rising and company enterprise loans and private loans through its retail finance arm TVS Credit score Providers.

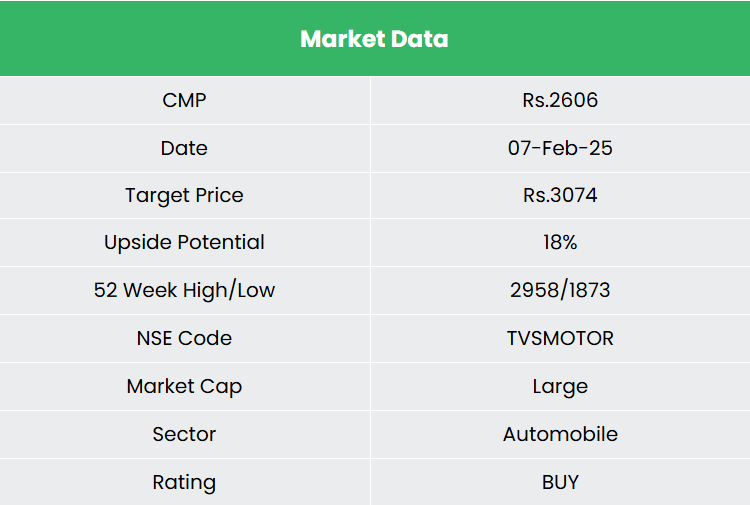

We fee TVSMOTOR a ‘BUY’ because it has robust development prospects as a 2-wheeler producer and fundamentals to be thought-about as FundsIndia’s Alpha Inventory Choose.

Merchandise and Providers

Merchandise provided by the corporate consists of bikes & scooters (together with electrical 2W), 3 wheelers (together with electrical 3W), mopeds. It’s also within the enterprise of offering finance through its retail finance arm TVS Credit score Providers.

Subsidiaries: As of FY24, the corporate has 16 subsidiaries and 11 affiliate corporations.

Funding Rationale

- New product launches – The corporate continues to broaden its portfolio with new merchandise and variants. In Q3FY25, it launched the quickest 125cc motorbike within the section, the TVS Raider iGO Variant, together with the TVS Apache RTR 160 4V that includes upside-down suspension (USD). A major milestone was the launch of the corporate’s first electrical 3W, the TVS King EV MAX, throughout the identical quarter. Initially obtainable at choose dealerships, the corporate plans to broaden gross sales within the subsequent two quarters. The TVS Jupiter 110, launched in Q2FY25, has been well-received available in the market. Moreover, the corporate launched a number of new merchandise in FY24, together with the TVS X, TVS Raider SS Version, TVS iQUBE, TVS Apache RTR 310, TVS HLX 150F, TVS Ronin, and TVS NEO AMI 125. This well timed growth of product portfolio is predicted to learn the corporate when it comes to market differentiation and aggressive edge in addition to constructing buyer loyalty and retention.

- Diversified operations – The corporate affords all kinds of merchandise, starting from 2W to 3W fashions in each ICE (Inner Combustion Engine) and EV variants. The corporate’s choices span throughout reasonably priced 2W & 3W to racing-inspired bikes. Within the newest quarter, home gross sales of 2W ICE grew by 5% year-over-year, outperforming the business’s 1% development. Worldwide gross sales of 2W ICE noticed a notable 26% enhance. Moreover, EV 2W gross sales surged by 57% throughout the interval. TVS Credit score added over 3 million new prospects this 12 months, bringing its whole buyer base to over 17.7 million. The e-book measurement expanded by 7%, reaching Rs.27,190 crore, whereas revenue earlier than tax rose by 40%, reaching Rs.321 crore.

- Q3FY25 – The corporate generated standalone income of Rs.9,097 crore, which is a rise of 10% in comparison with Q3FY24. EBITDA grew by 17% YoY to Rs.1,081 crore. The corporate reported web revenue of Rs.618 crore which is a rise of 4% in comparison with the corresponding quarter of the earlier 12 months.

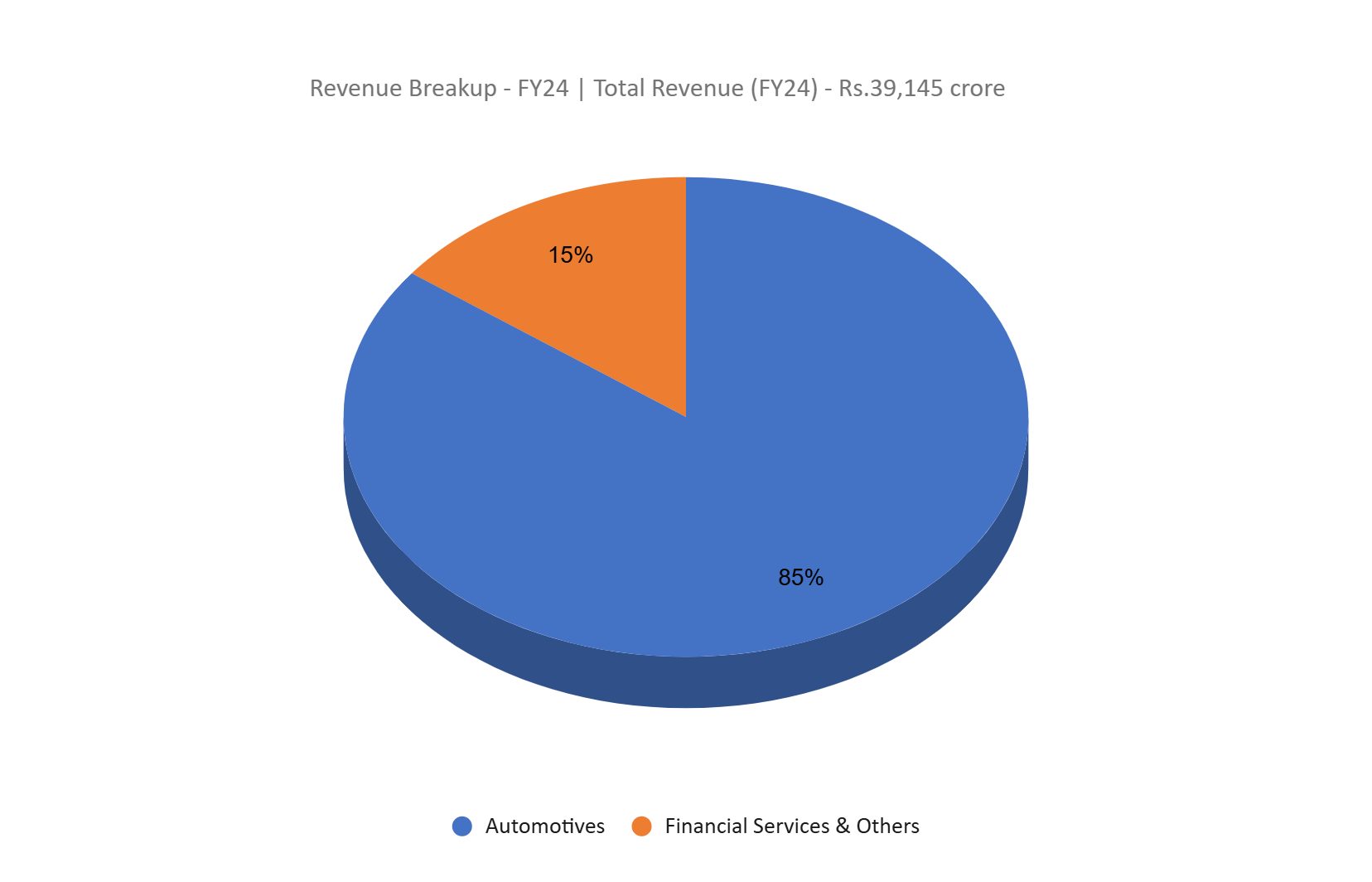

- FY24 – The corporate generated income of Rs.39,145 crore, a rise of twenty-two% in comparison with FY23 income. Working revenue is at Rs.5,500 crore, up by 37% YoY. The corporate posted web revenue of Rs.1,779 crore, a soar of 36% YoY. Through the interval the corporate surpassed 4 million two-wheeler gross sales for the primary time. The corporate’s home ICE 2W quantity elevated by 19% towards the business development of 13%. EV quantity doubled from 97,000 of final 12 months to 194,000. Within the worldwide markets, 2W gross sales grew by 47% to 2.36 lakhs.

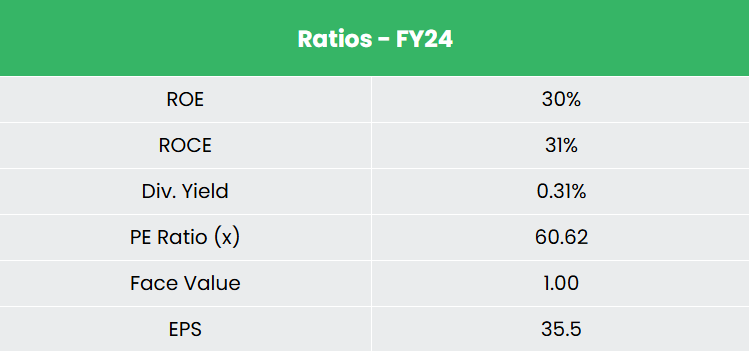

- Monetary Efficiency – The corporate has generated a income and PAT CAGR of 26% and 39% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 24% and 13% for FY21-24 interval.

Business

The Indian car business has historically been a powerful indicator of the nation’s financial well being, because it performs a pivotal function in driving each macroeconomic development and technological progress. The 2-wheeler section leads the market when it comes to quantity, fuelled by a rising center class and a big, youthful inhabitants. Moreover, the rising curiosity of corporations in tapping into rural markets has additional supported the sector’s development. On a world scale, the electrical car (EV) market was valued at round US$ 250 billion in 2021 and is predicted to broaden fivefold to US$ 1,318 billion by 2028. By 2030, the Indian authorities has set a goal for 30% of latest car gross sales within the nation to be electrical.

Development Drivers

- The Centre has launched the PM E-DRIVE scheme with a finances of US$ 1.30 billion (Rs. 10,900 crore), efficient from October 1, 2024, to March 31, 2026. The initiative goals to speed up the adoption of Electrical Autos (EVs), set up charging infrastructure, and develop an EV manufacturing ecosystem in India.

- The Authorities of India encourages overseas funding within the car sector and has allowed 100% FDI beneath the automated route.

- The discount within the tax burden within the 2025-26 Union Finances is predicted to spice up spending among the many increasing center class inhabitants.

Peer Evaluation

Rivals: Hero MotoCorp Ltd, Bajaj Auto Ltd, and so on.

The corporate is producing secure return ratios in keeping with the expansion within the gross sales. This means the corporate’s capacity to generate higher income for the capital invested.

Outlook

The corporate boasts a powerful R&D staff that’s essential in understanding evolving buyer wants and market traits. This permits the corporate to proactively introduce profitable merchandise and seize market share. For FY25, the corporate has set a capital expenditure steering of Rs.1,700 crore, with a good portion devoted to product growth. It stays dedicated to rising its presence in worldwide markets, specializing in areas like Africa and Latin America, and has not too long ago entered Morocco. This technique of steady innovation, numerous product choices, and market adaptability ensures the corporate stays aggressive, expands its buyer base, and retains tempo with market shifts. It’s also anticipating the beginning of Manufacturing Linked Incentive (PLI) advantages from Q4FY25, which ought to help margin development.

Valuation

We anticipate the corporate to maintain its market share good points led by aggressive product pipeline and robust execution capabilities. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs. 3,074, 49x FY26E EPS.

Danger

- Credit score threat – The corporate has excessive proportion of debt in its capital construction, which can affect its profitability, money reserves, and capability to lift additional capital.

- Macro-economic situations – Modifications in macro-economic situations resembling excessive inflation, financial slowdown, excessive rates of interest and so on. may have an opposed affect on the corporate turnover.

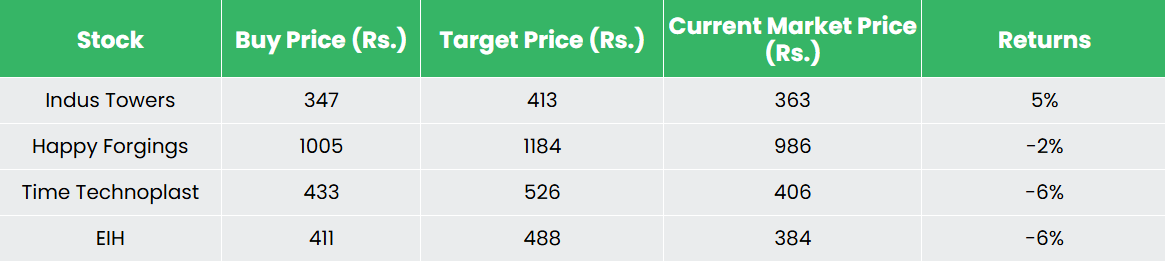

Recap of our earlier suggestions (As on 07 February 2025)

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Submit Views:

30