We’ve had an excellent run with the amaze card, which was THE greatest abroad card to make use of for anybody desirous to earn miles however but unwilling to pay 3% – 3.5% of additional charges (on prime of awful financial institution trade charges). Regionally, the amaze card was additionally an effective way for us UOB cardholders to avoid UOB$ retailers (which provides reductions however with the trade-off being a horrible rewards earn price).

As of yesterday, 1 October, UOB has formally nerfed the amaze hack.

DBS first did this in 2022, and now UOB is the subsequent child on the block to comply with swimsuit.

However all will not be misplaced.

There stays a couple of choices that we are able to nonetheless use to pair with the amaze card, specifically:

- Citi Rewards

- OCBC Rewards / Titanium

Each playing cards will nonetheless yield you 4 miles per greenback (mpd) and right here’s how you should use them.

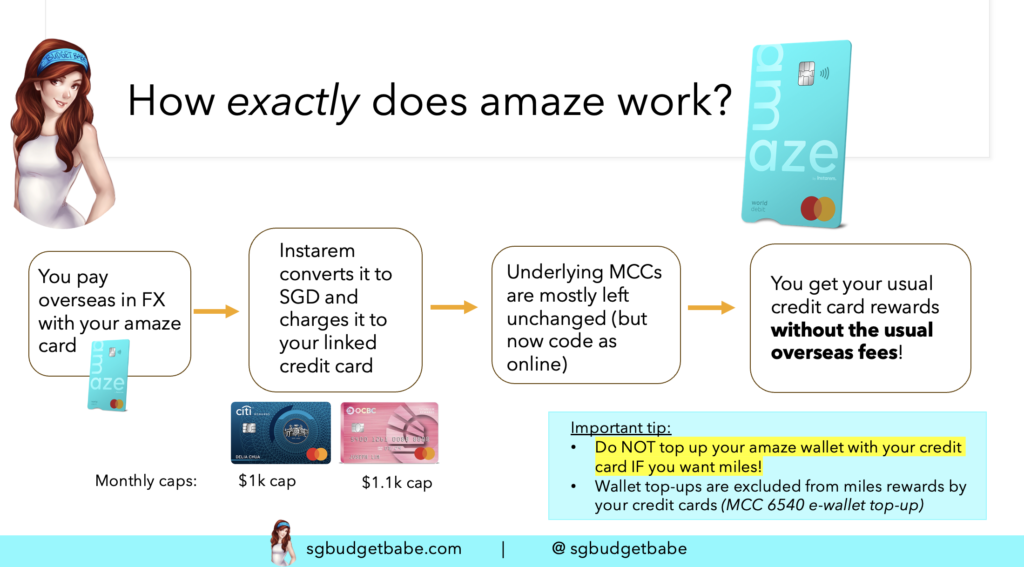

Notice that while you pair your bank cards with amaze, it allow you to save on the FCY transaction charges however since quantities are transformed into SGD, your rewards might be based mostly on the native SGD earn price as an alternative.

Between paying the ~2% markup on amaze and earn on the native mpd price, vs. paying ~3.5% in FCY conversion charges and a awful trade price for abroad mpd earn charges, the previous is mathematically a greater choice.

Click on right here to examine pesky FCY charges while you use your bank card to pay overseas.

Utilizing the bare Citi Rewards card by itself will solely offer you 4 mpd for on-line transactions. Sadly, this meant that tapping your bodily card and utilizing cell in-app funds (Apple Pay, Google Pay, Samsung Pay) wouldn’t qualify.

However there’s a loophole: you possibly can merely hyperlink your Citi Rewards card with amaze, and faucet your amaze card or use it to pay together with your cell in-app cost.

This allowed Citi Rewards cardholders to earn 4 mpd on even native spend, resembling in-person eating, groceries, procuring and transport (e.g. taxis and ride-hailing).

Amaze converts all transactions into on-line spend, which signifies that when paired with the Citi Rewards Card, you possibly can earn 4 mpd – capped to your first S$1,000 per 30 days.

The one exception is for travel-related transactions (resembling air tickets, accommodations or rental vehicles), that are particularly excluded from incomes the 4 mpd price by Citi.

OCBC Rewards x amaze

Notice: The previous identify is OCBC Titanium, in the event you’re a legacy cardholder like me.

OCBC Rewards provides 4 mpd for sure shopping-related transactions like department shops. Pairing it with the amaze card then makes it an ideal mixture for paying at abroad departmental shops – resembling Lotte Responsibility Free, and even procuring retailers resembling Lululemon or Louis Vuitton – every time we journey.

I’ve used this combo to earn loads of miles on my US and Korea journeys, as an example.

The one factor you gotta be careful for is to verify the procuring service provider you’re spending at falls underneath the whitelisted listing or classes to your OCBC Rewards playing cards. As an illustration, you is perhaps inclined to assume that you simply’ll earn 4 mpd with this card while you sohop at IKEA, Greatest Denki, Courts or Harvey Norman…however that’s not the case.

Don’t have the amaze app (or card) but? Join right here to get yours!

Workaround options for abroad spend

The only option to cope with this may be to make use of the next playing cards on this order:

- amaze x Citi Rewards: for nearly the whole lot besides travel-related transactions (so don’t use this to pay to your resort or prepare tickets!)

- amaze x OCBC Rewards: for all my procuring (be sure to test that the service provider will not be throughout the exclusion class first!)

- Your greatest common spending FCY card, such because the UOB PRVI Miles (2.4 mpd) or DBS Vantage (2.2 mpd).

If you wish to maximise your miles additional, you would additionally think about including these 2 playing cards into your stack:

- UOB Visa Signature Card: in the event you can hit no less than S$1,000 in FCY in that month. Notice that this card is just for the richer of us, attributable to its min. earnings requirement of $120k to use.

- Maybank World Mastercard: provided that you possibly can clock a min. of S$4,000 per 30 days, for an uncapped 3.2 mpd on FCY spend

I personally wouldn’t trouble, since I don’t journey typically sufficient or spend that a lot in FCY every year to justify the additional trouble of getting 1 – 2 extra new playing cards only for this workaround. Nonetheless, in the event you journey typically for work or holidays, and also you’re wealthy sufficient to satisfy the minimal earnings threshold or hit the minimal spend, then this is perhaps price contemplating.

Youtrip vs. amaze: which is best? Click on right here to learn! Spoiler: amaze for miles, Youtrip in the event you don’t care about incomes rewards otherwise you have a tendency to make use of money whereas abroad.

Is the amaze card nonetheless price maintaining?

For now, my reply continues to be a sure – I gained’t be cancelling my amaze card but. There isn’t a robust sufficient cause to take action, since you should use it with Citi Rewards and OCBC Rewards to nonetheless clock $2,100 and get 8,400 miles every month.

The difficulty is that I used to rely closely on the amaze x UOB Girl’s mixture to pay for all my abroad meals and drinks, in addition to the amaze x UOB Krisflyer pairing for any large ticket spending or my leftover bills as soon as my different spending caps have been hit. These will now not work from now.

We’ve had an excellent run with amaze, and it’s price maintaining an eye fixed out to see if any banks get impressed to comply with UOB and DBS of their therapy of amaze.

The worst nerf that would occur subsequent could be if Citibank decides to nerf amaze too. If that takes place, then it’d very properly kill off amaze, which is able to go away us shoppers worse off.

I actually hope not.

With love,

Daybreak