At this time we’ll take a short have a look at some mortgage fee historical past to achieve a bit context for the place we stand as we speak. It’s all the time useful to know what got here earlier than so you possibly can higher guess what would possibly come after.

Nearly everybody is aware of that mortgage charges hit all-time report lows in 2021. However are you aware what mortgage charges had been like within the early 1900s?

The 30-year mounted averaged 2.65% throughout the week ending January seventh, 2021, its lowest level in historical past.

Later that 12 months, the 15-year mounted hit the bottom level ever, sinking to 2.10% throughout the week ending July twenty ninth, 2021.

Some fortunate householders had been in a position to snag mounted rates of interest under 2% for the following 15 to 30 years!

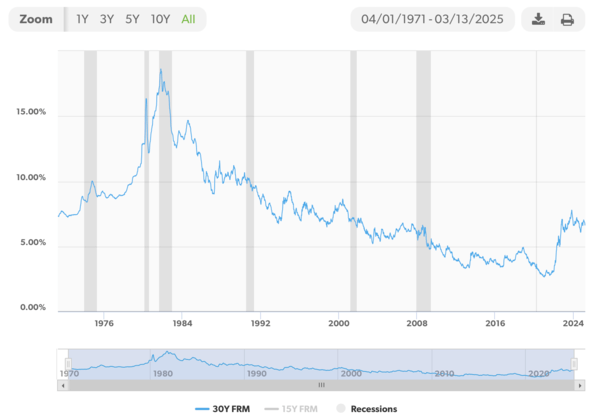

Freddie Mac’s Mortgage Charge Statistics Began in 1971

- Most mortgage fee statistics are tied to Freddie Mac’s archive

- Sadly, it solely goes again to the 12 months 1971 which isn’t a lot to go on

- I wished to drill down a bit deeper to see what issues had been like previous to the 70s

- And see if I might discover knowledge from earlier on within the twentieth century to achieve extra perspective

The determine above come from Freddie Mac’s Major Mortgage Market Survey, which solely dates again to 1971.

For the report, again in April of 1971, the primary month they started monitoring 30-year mounted mortgage charges, the nationwide common was 7.31%.

It went as excessive as 18.45% in October 1981 and as little as 2.65% in January 2021. That’s fairly a spread, clearly.

As you possibly can see within the chart, these 18% mortgage charges had been fairly short-lived, as had been the sub-3% mortgage charges. So finally they are often thought-about outliers within the grand scheme of issues.

The 15-year mounted has solely been tracked by Freddie Mac since September 1991, when charges averaged 8.69%. In that very same month the 30-year mounted averaged 9.01%.

Anyway, I bear in mind some time again when mounted charges had been within the low 4% vary that the media was occurring about how charges hadn’t been this low because the Fifties.

Which made me surprise; the place had been they even pulling that historic mortgage fee knowledge from?

I by no means actually took the time to see how low charges had been again then, however I lastly determined to do some digging to get a bit extra info.

A Little Little bit of Mortgage Charge Historical past

- Mortgage fee historical past stretches again practically a century

- However one of the best information solely return to the early Seventies

- The 30-year mounted gained in recognition across the Fifties

- And charges reached a low round 1945 earlier than hitting new lows in 2021

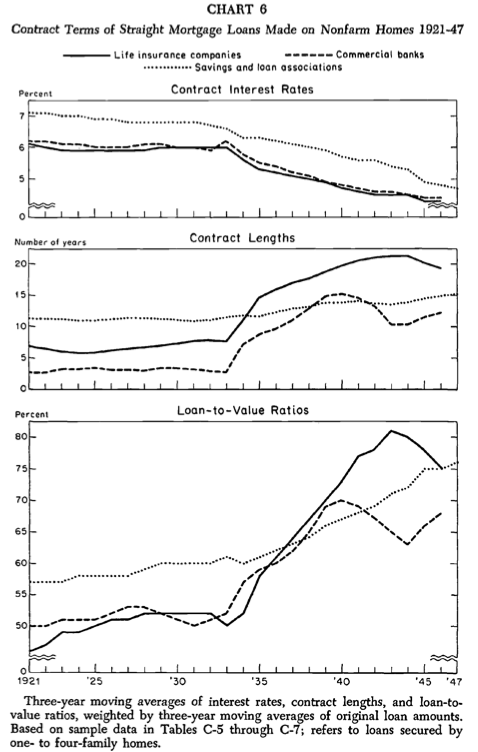

My quest to search out deeper mortgage fee historical past introduced me to a number of out-of-print volumes from the Nationwide Bureau of Financial Analysis, which appears to have one of the best information on the market.

Sadly, the main points are nonetheless fairly murky at greatest. You see, again then there have been various kinds of mortgages, not like those we use as we speak.

Whereas I don’t know when the very first 30-year mounted mortgage was created and issued (somebody please inform me), they had been believed to grow to be widespread within the Fifties, which is why media references that decade.

Earlier than that point, it was widespread for entities like industrial banks and life insurance coverage firms to situation short-term balloon mortgages, .

These mortgages usually featured loans phrases as brief as three to 5 years, which might be regularly refinanced and by no means paid off.

These loans had been additionally underwritten at LTV ratios round 50%, that means it was fairly troublesome to get a house mortgage with out a sizable down cost. In different phrases, homeownership was reserved for the rich!

Later, as soon as the Nice Melancholy struck, residence costs nosedived and scores of foreclosures flooded the housing market as a result of nobody might afford to make giant funds on their mortgages, particularly in the event that they didn’t have jobs.

Then got here FDR’s New Deal, which included the Residence Homeowners’ Mortgage Company (HOLC) and the Nationwide Housing Act of 1934, each of which aimed to make housing extra reasonably priced.

The HOLC, established in 1933, might clarify why long-term fixed-rate mortgages are in existence as we speak.

The aim of the HOLC was to refinance these previous balloon mortgages into long-term, totally amortized loans, with phrases sometimes starting from 20 to 25 years. Not far off from the 30-year mounted we take pleasure in as we speak.

In a way, it jogs my memory of the Residence Inexpensive Refinance Program (HARP), which decrease mortgage charges for hundreds of thousands of householders throughout the Nice Monetary Disaster (GFC).

Appears some issues by no means change, regardless of us considering it’s totally different this time…

Mortgage Charges Got here Down as Mortgage Phrases and LTVs Elevated

- Homeownership grew to become extra reasonably priced over time thanks to a few principal issues:

- Decrease rates of interest

- Longer mortgage phrases

- And better LTVs (decrease down funds)

In 1934, the FHA and the Federal Financial savings and Mortgage Insurance coverage Company (FSLIC) had been created, and in 1938, Fannie Mae was born.

All of those entities primarily expanded credit score availability and led to extra liberal lending requirements for residence patrons.

Over time, mortgage rates of interest got here down whereas LTV ratios and mortgage phrases elevated, as you possibly can see from the charts under.

This made homeownership extra accessible for everybody, not simply these with the power to carry a large down cost to the desk.

Historic Mortgage Charges within the Early twentieth Century

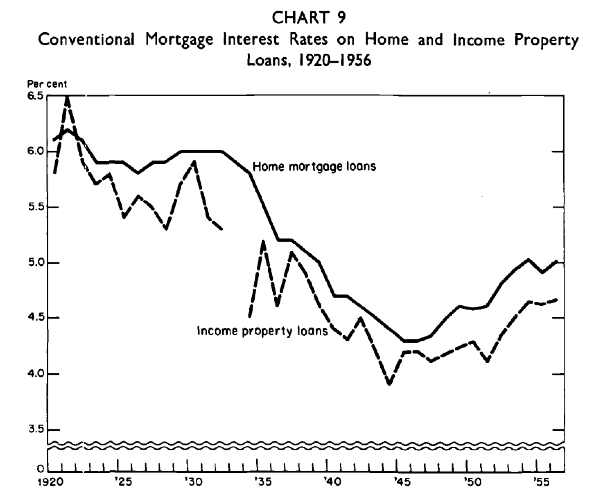

Whereas it’s laborious to get an apples-to-apples comparability of mortgage charges earlier than the arrival of the 30-year mounted, the Nationwide Bureau of Financial Analysis does have a chart detailing charges from 1920 to 1956.

From about 1920 till 1934, standard mortgage charges averaged shut to six%, after which started to say no to a low level of slightly below 4.5%.

That is most likely the reference level the media used after they stated charges hadn’t been this low in 60 years (again after they dropped within the early 2010s).

Mortgage Charges within the Twenties to Fifties

- We see a gentle drop in rates of interest from round 1935 to 1945

- Then a bottoming out for a couple of years earlier than charges started their ascent to as excessive as 18% within the early Eighties

- Maybe as the results of World Conflict II ending and all of the related authorities debt and inflation that got here with it

- Exacerbated by a second spherical of inflation associated to the oil embargo that elevated enter prices for companies

Nonetheless, it’s unclear what forms of mortgages these had been over this intensive time interval, and when the 30-year mounted truly grew to become the usual. However it does present for a bit little bit of context.

The excellent news is as a result of mortgage charges went sub-3% within the early 2020s, we are able to most likely think about these to be the bottom on report, regardless of what occurred within the early twentieth century.

If we solely think about Freddie Mac’s knowledge since 1971, the 30-year mounted has averaged about 7.75% over that interval.

However that features some very high-rate years within the Seventies and Eighties and a few very low years within the 2010s and 2020s.

Many wish to consult with charges as we speak as regular mortgage charges, however that doesn’t imply they aren’t loads greater than they was once.

In actual fact, they practically tripled from 2021 to 2023, from 2.75% to eight%, so regular is a relative time period at greatest.

Since 1990, the 30-year mounted has averaged nearer to six%, thanks partially to the report low charges seen over the previous decade.

So maybe mortgage charges are nearer to their long-term common as we speak within the high-6s. However with out residence value reduction and/or greater wages, affordability will stay traditionally low, which is why residence gross sales have plummeted.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on X for decent takes.