One of many main amendments carried out as per the Finance Invoice 2023 is to curtail LTCG (Lengthy Time period Capital Acquire) advantages by deeming the beneficial properties arising from ‘specified mutual funds’ as short-term capital beneficial properties (STCG).

What are these Specified Mutual Fund Schemes as per the Revenue Tax Act? What’s the main modification with respect to the taxation of the beneficial properties arising out a specified mutual fund for Monetary Yr 2023-24 (AY 2024-25)?

What are Specified Mutual Fund Schemes as per the Revenue Tax Act?

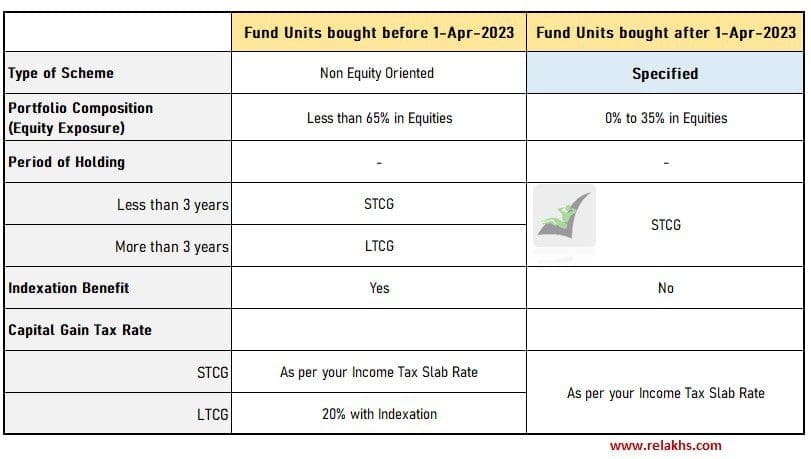

A mutual fund by no matter identify known as, the place no more than 35% of its complete proceeds is invested within the fairness shares of home firms. Examples are : Liquid Funds, Quick Period Debt Funds, Gold Mutual Funds, Fund of Funds and many others.,

For the needs of part 50AA of the Revenue Tax Act, “specified mutual fund” means a mutual fund by no matter identify known as, the place no more than 35% of its complete proceeds is invested within the fairness shares of home firms. Accordingly, an “equity-oriented fund” which invests in models of one other fund as a substitute of investing straight in fairness shares of home firm could also be considered “specified mutual fund”. – AMFI

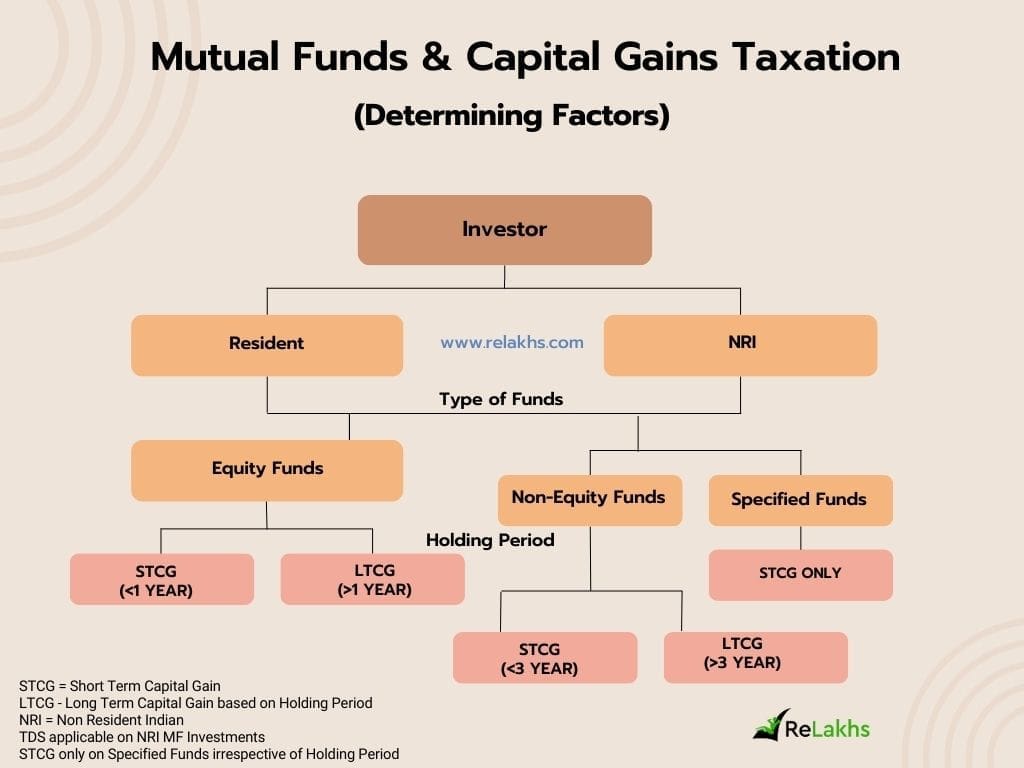

With this new modification, we now have three broad kind of funds – Fairness, Non-Fairness & Specified Funds.

| Proportion of Fairness Publicity | 0% to 35% | 36% to 64% | 65% & extra |

| Sort of Fund | Specified Fund | Non-Fairness oriented Fund (Hybrid Funds) |

Fairness Mutual Fund |

What’s the new Tax modification w.r.t Specified Mutual Funds?

Let’s first perceive how the capital beneficial properties of a mutual fund scheme are categorized as Quick-term or Lengthy-term?

Interval of Holding & Capital Good points on Mutual Funds

Capital beneficial properties on Mutual funds might be both long run capital beneficial properties or short-term capital beneficial properties, relying in your funding horizon.

- Lengthy Time period Capital Good points

- In case you make a achieve / revenue in your funding in a Fairness Mutual Fund scheme that you’ve held for over 1 12 months, it is going to be categorized as Lengthy-Time period Capital Acquire.

- In case you make a achieve / revenue in your funding in a Non-Fairness Mutual Fund scheme (or in a Debt Fund) that you’ve held for over 3 years, it is going to be categorized as Lengthy Time period Capital Acquire.

- Quick Time period Capital Good points

- In case your holding in a Fairness mutual fund scheme is lower than 1 12 months i.e. in the event you withdraw your mutual fund models earlier than 1 12 months, after making a revenue, then the revenue might be thought-about as Quick Time period Capital Acquire.

- In case you make a achieve / revenue in your Non-Fairness (or aside from fairness oriented schemes) that you’ve held for lower than 36 months (3 years), it is going to be handled as Quick Time period Capital Acquire.

The brand new modification that we’re discussing is expounded to non-equity oriented funds.

The Capital beneficial properties from switch or redemption of models of “specified mutual fund schemes” acquired on or after 1st April 2023 are handled as quick time period capital beneficial properties taxable at relevant earnings tax slab charges as supplied above irrespective of the interval of holding of such mutual fund models.

So, the indexation profit can also be not out there whereas calculating long-term capital beneficial properties on Specified Mutual Funds. Pursuant to the above change, advantages within the type of decrease tax charges and indexation out there to LTCG on the sale of non-equity mutual funds might be changed by taxation on the most marginal charge, as relevant to STCG.

Nonetheless, because the beneficial properties are nonetheless characterised as capital beneficial properties, traders are allowed to set off every other short-term capital losses which can be incurred by them towards capital beneficial properties of specified mutual fund.

Associated Article : What’s Indexaton? How is it useful?

You probably have purchased models of a non-equity oriented fund previous to 1st April 2023 then this new tax rule isn’t relevant.

Proceed studying:

(Publish revealed on : 25-Sep-2023)