Speedy GDP development, due partly to excessive charges of funding and capital accumulation, has raised China out of poverty and into middle-income standing. However progress in elevating residing requirements has lagged, as a side-effect of insurance policies favoring funding over consumption. At current, consumption per capita stands some 40 p.c under what may be anticipated given China’s revenue degree. We quantify China’s consumption prospects through the lens of the neoclassical development mannequin. We discover that shifting the nation’s manufacturing combine towards consumption would increase each present and future residing requirements, with the latter consequence owing to diminishing returns to capital accumulation. Chinese language coverage, nonetheless, seems to be transferring in the other way, to reemphasize investment-led development.

Chinese language Dwelling Requirements Lag Behind Earnings

China’s development efficiency has been outstanding because the introduction of financial reforms within the late Nineteen Seventies. In accordance with the official knowledge, actual GDP development has averaged 8.9 p.c since 1978. That makes China the quickest rising financial system over the interval in a pattern of 124 nations. (The pattern contains all nations with GDP above $1 billion and populations above a million as of 2019.) To make certain, development has slowed extra just lately, averaging 4.9 p.c over the previous 5 years. Even so, China’s efficiency stays distinctive, at slightly below the 90th percentile of our group.

Speedy financial development has led to an analogous improve in per capita revenue, lifting China into middle-income standing. (Except for web overseas funding revenue, GDP and economy-wide revenue are the identical.) In accordance with official figures, actual per capita revenue has risen by an element of greater than thirty since 1978. Annual per capita revenue now stands at about $22,100 measured at buying energy parity, in “2021 worldwide {dollars}.” (Until in any other case famous, actual revenue figures depend on this measure all through this submit.) This locations China at roughly the sixtieth percentile of the worldwide revenue distribution.

But progress in elevating residing requirements has lagged. Annual per capita family consumption now stands at about $8,300 measured at buying energy parity, putting China at roughly the 45th percentile of the worldwide distribution. Though the distinction between the 60th and the 45th percentiles might not appear massive, it interprets into to a significant shortfall in Chinese language residing requirements. On the 60th percentile of the worldwide distribution, consumption per capita would come to roughly $13,700, two-thirds greater than at current.

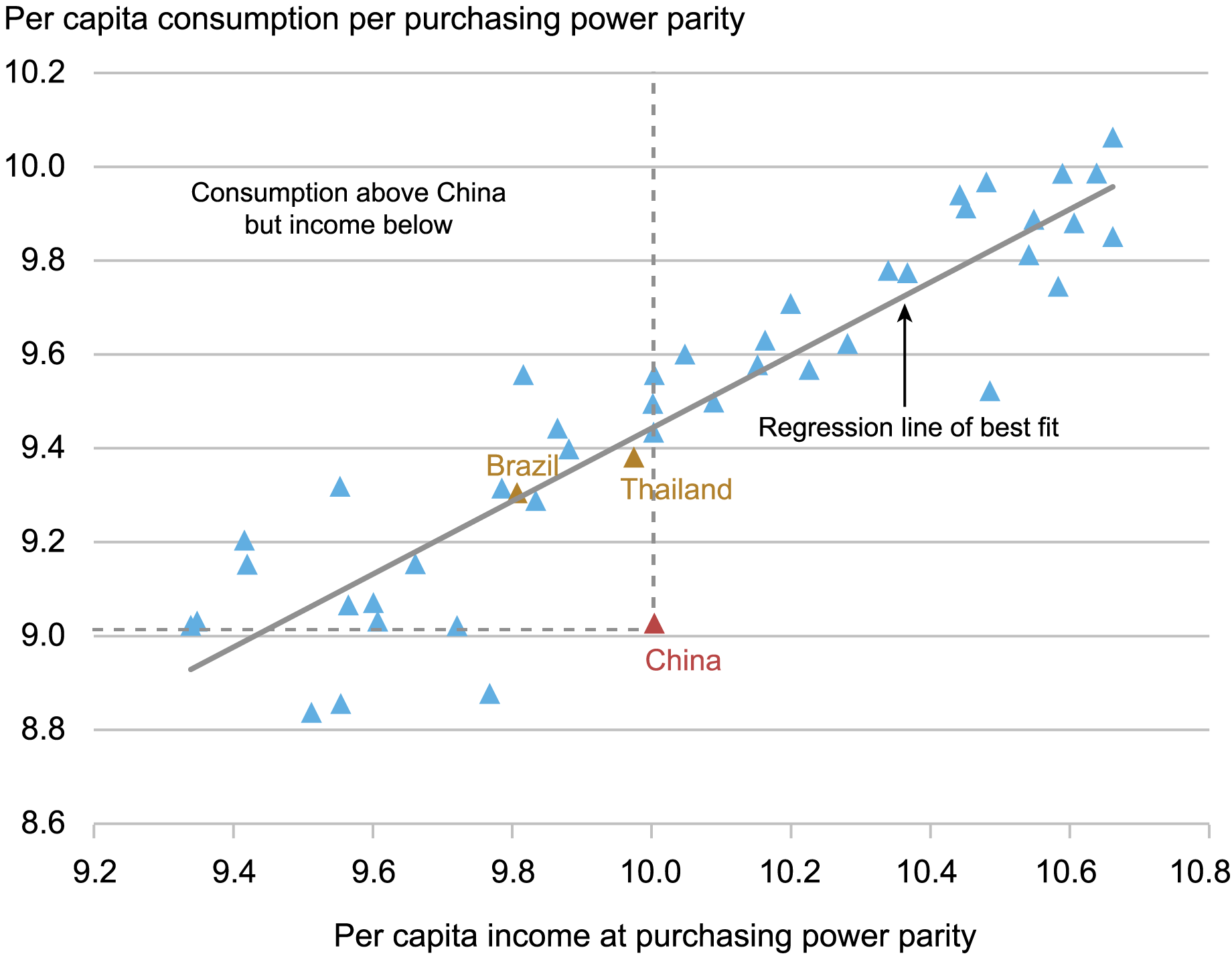

Specializing in consumption reasonably than revenue casts a brand new mild on China’s growth accomplishments. The purpose of financial development, in any case, is to boost folks’s residing requirements, to not produce for manufacturing’s sake. However as proven within the chart under, eighteen of the forty-five center revenue nations in our pattern have greater common residing requirements than China however decrease revenue ranges. (Be aware that revenue and consumption figures are in pure logs, in order that variations between nations translate roughly into percentages.) To take two notable examples, per capita consumption in Brazil is nearly a 3rd greater than in China with per capita revenue virtually 20 p.c decrease; consumption in Thailand is 40 p.c greater with incomes about 3 p.c decrease.

Chinese language Consumption Spending is Unusually Low Given Earnings

Notes: Earnings and consumption figures are for 2023 and measured at 2021 buying energy parities, with ICP knowledge for 2021 are up to date to 2023 utilizing nationwide actual GDP, actual consumption, and inhabitants development charges. Center revenue nations are outlined as these with per capita incomes between one half and twice China’s degree. Figures are in pure logarithms, giving variations a proportion interpretation: A distinction of 0.1 (for instance, between 9.4 and 9.5) is equal to 10 log proportion factors and roughly 10 p.c in arithmetic phrases.

Our chart exhibits solely personal (or “family”) consumption, and items and providers supplied by the federal government additionally contribute to residing requirements. However China doesn’t rank any greater on broader measures of consumption that embrace authorities spending.

The supply of China’s income-consumption mismatch is straightforward to find. China devotes an awfully excessive fraction of nationwide revenue to funding reasonably than consumption. Funding as a share of GDP has been constantly above 40 p.c because the mid-2000s and constantly above 35 p.c because the mid-Nineteen Eighties. With the median international funding charge hovering within the mid to low 20s, China’s funding charges place it among the many prime 5 p.c of nations worldwide yearly since 1992.

Sustaining excessive funding to advertise capital deepening is one key to growth success. That entails sacrificing present consumption. However China’s lagging progress in elevating residing requirements raises the query of whether or not it’s on the mistaken facet of this trade-off. Would a shift to a decrease funding path result in greater residing requirements in future a long time?

Classes From the Neoclassical Progress Mannequin

The usual neoclassical development mannequin offers a helpful framework for analyzing the sources of Chinese language development. Below the mannequin, financial development comes from three fundamental sources: will increase in capital inputs, will increase in labor inputs, and enhancements in know-how. The expansion contributions from capital and labor are equal to the expansion charges of those inputs, weighted by their shares within the worth of manufacturing. The expansion contribution from know-how (termed “whole issue productiveness” or TFP) is calculated as a residual, as the rise in output not defined by greater inputs.

China’s excessive funding share has supported a speedy buildup within the nation’s capital inventory. In reality, China’s capital-output ratio is now among the many highest on this planet in PPP phrases. However capital accumulation is topic to diminishing returns: A given increment makes a smaller contribution to development when capital is considerable than it does when capital is scarce. Furthermore, because the capital inventory rises relative to output, a better fraction of latest funding should go to offset ongoing depreciation.

The impression of diminishing returns is already in proof. In accordance with our estimates, will increase in capital inputs now contribute lower than 3 proportion factors to annual GDP development, down from a excessive of practically 6 ppt. early within the final decade (see the chart under).

Excessive Funding Spending is Delivering a Declining Progress Payoff

Contribution to Actual GDP Progress from Capital Inventory Progress

Notes: Actual capital inventory knowledge by 2019 are taken from the Penn World Desk. Thes PWT 2019 worth is up to date to 2023 utilizing NBS actual fastened funding knowledge, through the perpetual stock technique. The expansion contribution from capital accumulation is measured because the log development charge of the capital inventory multiplied by the capital share in nationwide revenue.

Projection Outcomes

We depend on the neoclassical mannequin to check China’s revenue and consumption trajectory beneath two eventualities. The important thing projection assumptions are as follows.

- Within the Excessive Capex state of affairs, funding spending as a share of GDP stays at its present worth by the projection horizon.

- Within the Reasonable Capex state of affairs, the funding share enters a gradual decline, stabilizing at 25 p.c of GDP by 2040. The output now not going to funding beneath the Reasonable Capex state of affairs goes as a substitute to help present consumption.

- Different components affecting development are stored the identical throughout the 2 eventualities, together with the paths of labor inputs, TFP development, and relative costs.

Though these assumptions are debatable, the outcomes ought to present a helpful benchmark as as to whether excessive funding has turned self-defeating in welfare phrases. This evaluation builds on our earlier work: See Higgins (2020) and Clark and Higgins (2023) for implementation particulars.

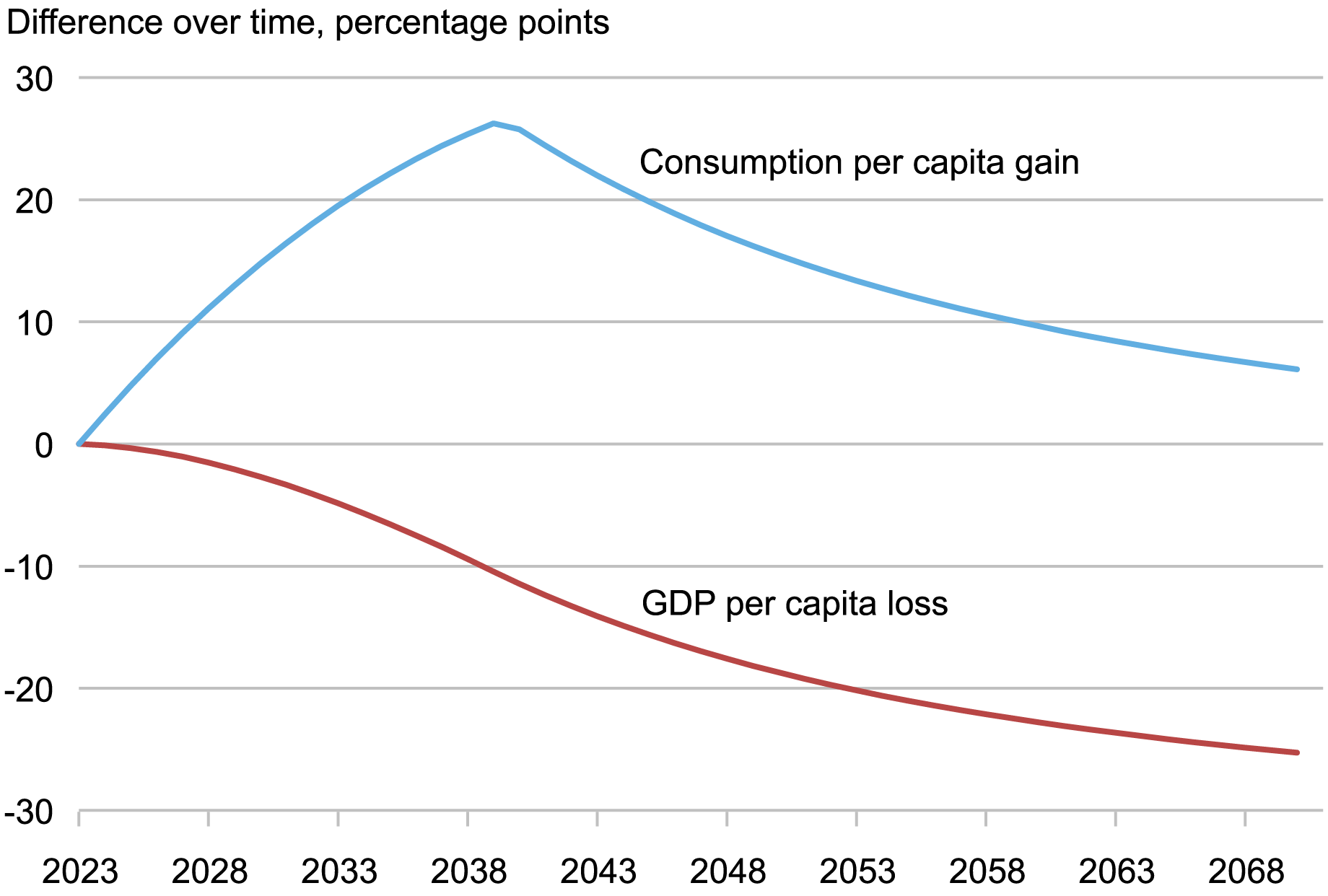

The projection outcomes are summarized within the chart under. To focus on the impression of decreasing capital expenditure as a share of GDP, the chart is expressed in p.c variations. The purple line exhibits the p.c distinction in actual per capita GDP within the Reasonable Capex vs. the Excessive Capex state of affairs. The blue line exhibits the p.c distinction in actual per capita consumption between these eventualities.

Decrease Funding Would Imply Greater Chinese language Dwelling Requirements

GDP and Consumption in Reasonable vs. Excessive Capex Situation

Supply: Creator’s calculations. See Higgins (2020) and Higgins and Clark (2023) for implantation particulars.

Notes: Traces present the projected p.c variations in actual per capita GDP and actual per capita consumption within the Reasonable Capex vs. Excessive Capex eventualities.

As could be seen from the purple line, the Reasonable Capex state of affairs places GDP on a markedly decrease development path. By 2035, GDP is about 6½ p.c decrease than beneath the Excessive Capex state of affairs. The GDP hole swells to fifteen p.c by 2045 and to about 25 p.c by 2065. The supply of this development underperformance is easy. A decrease funding share interprets into slower development within the capital inventory, a smaller capital contribution to GDP development, and a mounting GDP and revenue hole.

As evident from the blue line, nonetheless, the Reasonable Capex state of affairs places per capita consumption on a markedly greater development path. By 2035, per capita consumption is nearly 25 p.c greater than beneath the Excessive Capex state of affairs. This consumption benefit ultimately fades given slower GDP and revenue development. But consumption stays some 20 p.c greater than beneath the Excessive Capex state of affairs in 2045 and a few 6 p.c greater in 2070. Declining returns to capital accumulation imply that the MI consumption benefit would erode fairly slowly over the extra distant future. Certainly, prolonged projections don’t level to consumption convergence till after 2120.

Easy arithmetic helps clarify why the Reasonable Capex consumption benefit is so persistent. Below the state of affairs, the share of consumption in GDP rises to 55 p.c of GDP from the present 39 p.c—the flipside of the decrease capex share. This boosts the extent of consumption, given GDP, by an element of roughly 1.4. GDP beneath a high-investment trajectory must be larger by an element of greater than 1.4 to offset this benefit. Given the neoclassical development arithmetic, that’s not one thing that might occur anytime quickly.

The exact numerical outcomes of this projection train are much less essential than its central message. China is investing an excessive amount of, buying and selling massive consumption beneficial properties over the following a number of a long time for smaller beneficial properties within the distant future.

Notably, our evaluation has centered on relative consumption ranges, not on extra summary measures of social welfare. Formal welfare analyses sometimes apply a reduction issue to future outcomes (for instance, the risk-free rate of interest). Such an strategy would strengthen our outcomes, attaching a low weight to consumption payoffs that materialize solely within the 22nd century.

Again to the Future for Financial Coverage

The notion that China ought to rebalance its financial system away from funding spending and towards consumption quantities to acquainted acquired knowledge in worldwide coverage circles. It is usually the standard official place of the Chinese language authorities, adopted as a aim as way back because the 2004 Central Financial Work Convention and reaffirmed in lots of subsequent paperwork. However, the information point out that little rebalancing has occurred within the twenty years since.

As for the prospects for future rebalancing, President Xi’s public focus has been on industrial goals, notably, the necessity to promote “new high quality productive forces” in high-tech industries whereas sustaining a powerful presence in conventional industries. The coverage assertion issued after the Communist Celebration’s July management assembly took an analogous tack, that includes intensive dialogue of funding and industrial coverage however solely a single passing reference to client spending. The shift in official rhetoric has been matched by a surge in financial institution lending to the commercial sector, a growth highlighted in a Liberty Avenue Economics submit a couple of months in the past. To make certain, the authorities have launched a wide range of extra stimulus measures in current weeks. However these appear extra centered on stabilizing the investment-heavy actual property sector and native governments than on supporting consumption.

In brief, China’s development technique seems to be reverting to the manufacturing- and investment-focused posture that prevailed in prior a long time. Time will inform whether or not this “again to future” technique can help sustained development. However it would certainly depart Chinese language residing requirements decrease than they could possibly be.

Matthew Higgins is an financial analysis advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The way to cite this submit:

Matthew Higgins, “Why Funding‑Led Progress Lowers Chinese language Dwelling Requirements,” Federal Reserve Financial institution of New York Liberty Avenue Economics, November 14, 2024, https://libertystreeteconomics.newyorkfed.org/2024/11/why-investment-led-growth-lowers-chinese-living-standards/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).