Disclaimer: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!!!

DCC is an funding I made again in December 2022. The funding thesis again then was that it was a profitable compounder/serial acquirer that had the chance to develop additional by way of its 3 platforms (Power, Healthcare, Know-how).

Within the meantime, a number of sudden issues occurred. After points within the non-Power segments, DCC is at the moment remodeling itself again into the unique Power distributor and offered already a major a part of its non.Power companies. The transformation has progressed nicely together with a share purchase again tender however isn’t completed but.

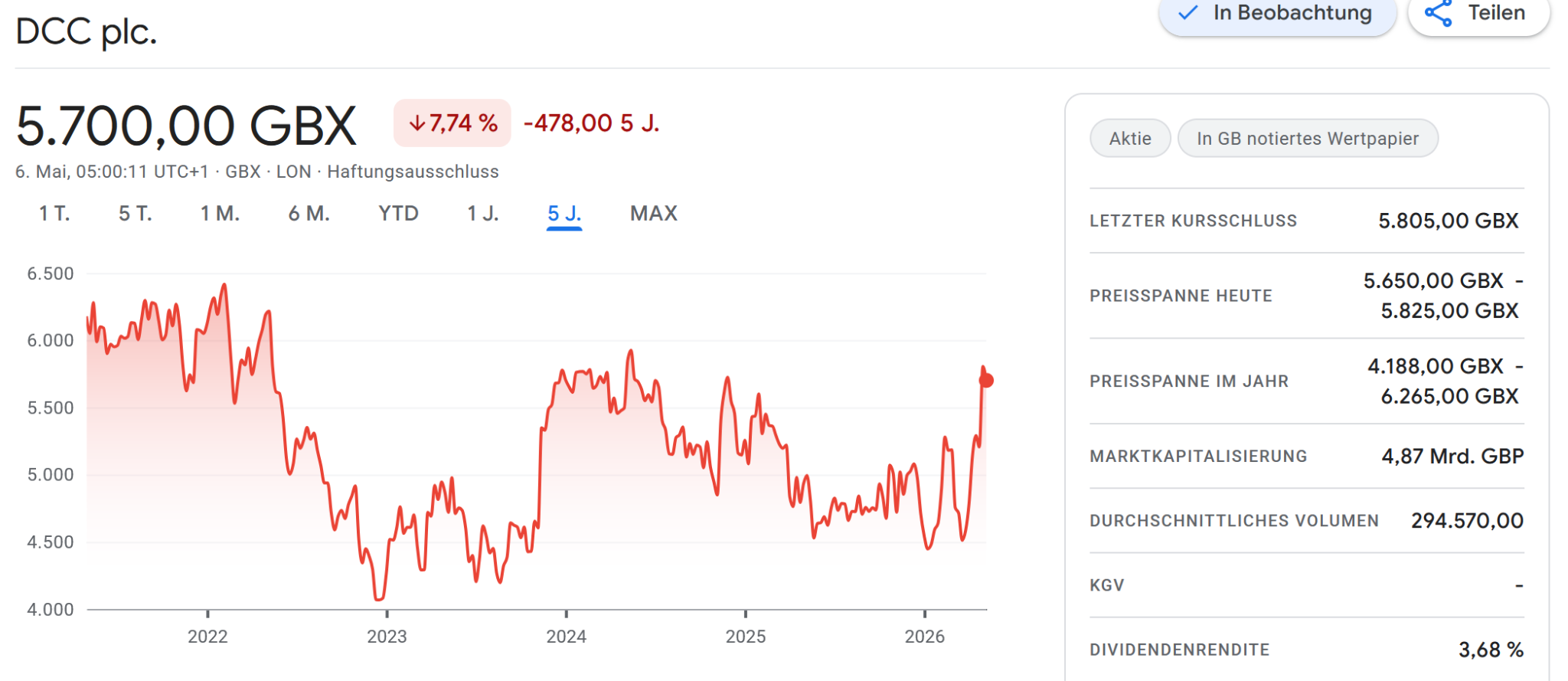

Trying on the share worth, we will see that not a lot occurred over the past 5 years however that the timing for getting into DCC in Dec 2022 retrospect was fairly fortunate:

After the latest bounce to 58 GBP, I’m up 42% in complete (in EUR, together with dividends) which isn’t spectacular and reasonably on the decrease finish of my anticipated final result. Nevertheless, given the “Pivot” it’s nonetheless an honest end result and largely attributable to the low entry level and the related dividends.

Now quick ahead to final week:

Personal Fairness behemoth KKR and one other vitality centered PE known as Power Capital Companions approached DCC and appear to have informally provided to take over DCC at 58 GPB per share which solely represents a 15% premium over the common share worth for the previous few months.

DCC instantly declined the provide as “too low”.

Power Capital Companions is a fairly large Power centered US PE/Infrastructure investor that owns a number of “Power Transition” companies. AuM appears to be north of 40 bn USD.

Though KKR didn’t disclose which fund is bidding, it appears that each KKR and ECP see this as an infrastructure play which makes a number of sense.

58 GBP per share is clearly a low ball provide and no formal provide has but been made. Beneath the relevant Irish legal guidelines, KKR has time till June tenth to both submit a proper provide or stroll away.

From a shareholder perspective, I assume that possibly a number of traders have been pissed off that the inventory solely went sideways for the final 5 years or so and are possibly pleased to exit at that stage.

The “asset heavy” Infrastructure PE playbook

DCC to date has operated as a comparatively capital gentle distributor, however I feel it’s comparatively simple to pivot them into an Infrastructure like enterprise that normally enjoys considerably decrease value of capital.

In distinction to “regular” Personal Fairness, Infrastructure Personal Fairness nonetheless enjoys a fairly good time. Many gamers have raised giant funds and are desperate to deploy cash. Infrastructure is commonly thought of “AI protected” nowadays.

So I suppose there could be an opportunity that another gamers would possibly look very intently at this case. DCC is a really apparent goal and the timing is sort of good from a PE perspective. The refocusising on Power at DCC remains to be underway and the outcomes don’t look so “clear” in the intervening time,

DCCs enterprise mannequin, particularly the LPG distribution enterprise has a number of potential to get easy accessibility to many SME corporations and promote them options.

Particularly the present volatility in fossil vitality costs opens up a singular promoting alternative for options that supply much less publicity like rooftop photo voltaic and so on.

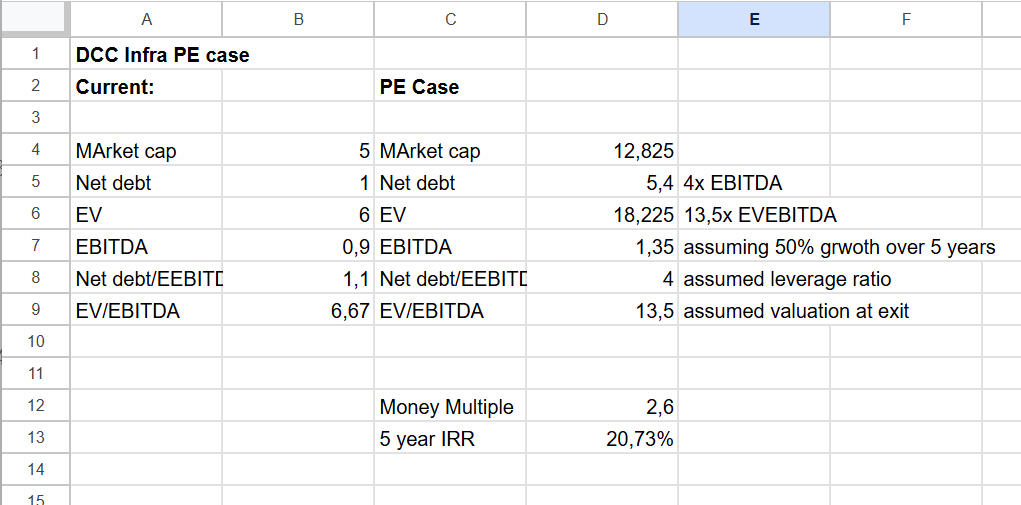

Based on TIKR, DCC’s Web debt to EBITDA ratio is simply round 1,2x. The corporate is valued at round 7xEV/EBITDA. The everyday infrastructure playbook can be to make the corporate extra “asset heavy”. As a result of low gearing, this might be financed by extra leverage. A typical “asset proudly owning” infrastructure firm with long term contracts might be simply levered 4-5x Web debt/EBITDA,

In DCC’s case, with round 900 mn in EBITDA, growing the leverage ratio to 4x would enable them to challenge virtually 3 bn in debt which might finance a number of property. These property then will mechanically improve EBITDA,

A stabilized infrastructure like firm can then be offered at a lot increased multiples, normally at 12-15x EV/EBITDA. So the worth creation potential for a great Infrastructure PE store is critical.

Only for enjoyable I did a excessive stage calculation how that train would look from this angle (I simply took the present numbers from TIKR, earlier than additional disposals):

A possible IRR of above 20% p.a. is very engaging for an Infrastructure fund and as I’ve written earlier than, PE’s have some extra levers to “juice up” the IRR and earn even increased efficiency charges.

Is DCC now an attention-grabbing particular scenario play ?

There’s clearly the danger that DCC would possibly reject even increased affords, however I do suppose the 58 GBP low ball provide offers an honest “flooring” for the inventory (“Anchoring impact”).

For one, DCC ought to count on some optimistic operational tailwinds. Risky and excessive vitality costs up to now have been good for DCC’s vitality enterprise. As we will see daily “on the pump”, distributors like regular Petrol stations instantly improve costs though they typically have inventories for some weeks/months and infrequently drop costs a lot slower.

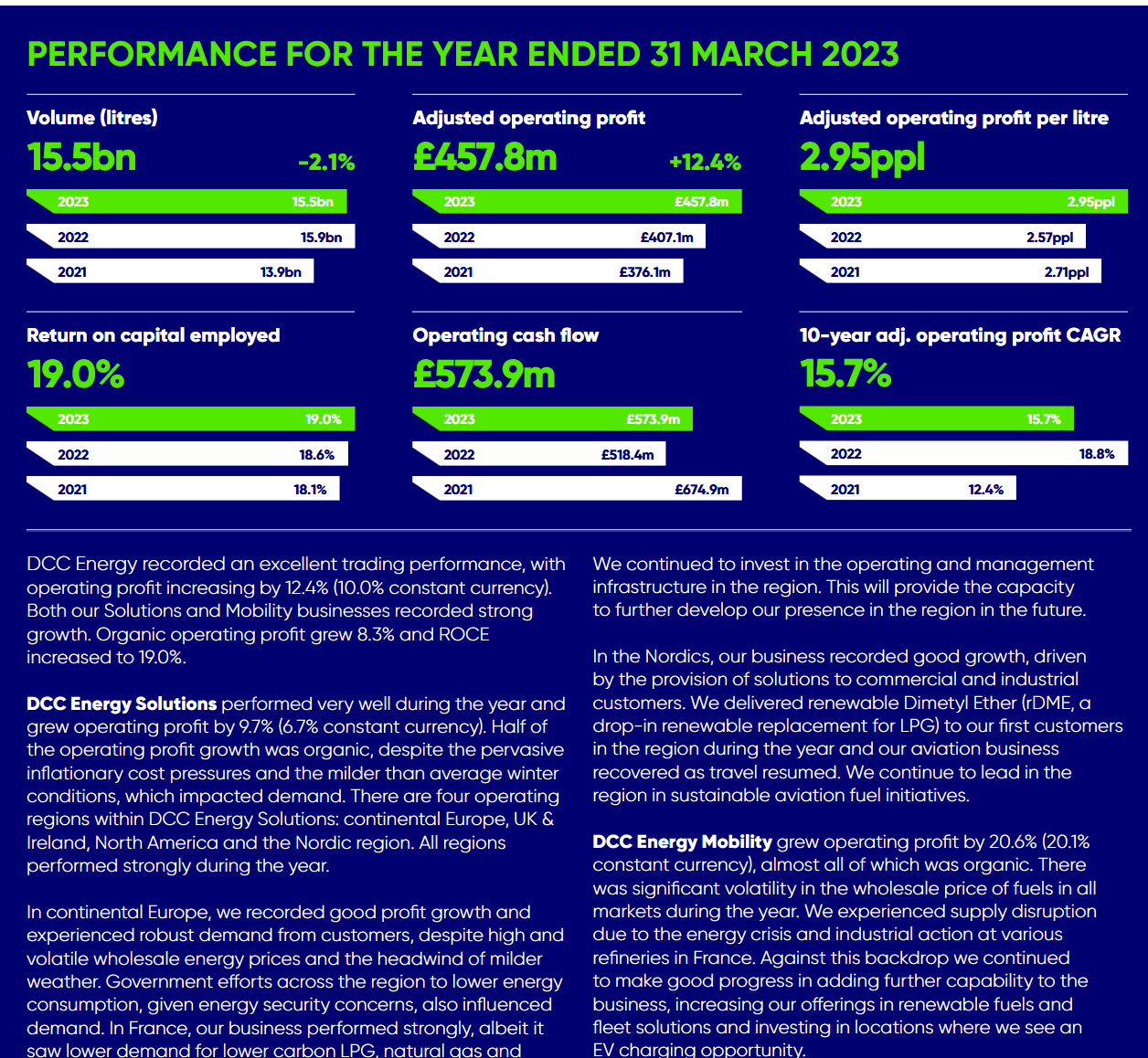

Trying again to the final vitality worth shock in 2022, we will see that this was DCC’s finest yr, particularly for the vitality enterprise:

Though there isn’t a assure that the identical will apply to 2026, there’s a excessive probability that 2026 will look good for DCC from an operational perspective.

As well as, I do count on that the transformation might be roughly accomplished within the 2026 calendar yr.

So all in all, 2026 appears to look fairly good for DCC. I feel this additionally explains the timing of KKR and ECP, as they don’t need to wait till this enchancment exhibits within the outcomes of DCC.

Even in case, DCC will get offered comparatively rapidly at 58 GBP per share, one would nonetheless get the Dividend that might be recorded finish of could.

Fast handicapping train:

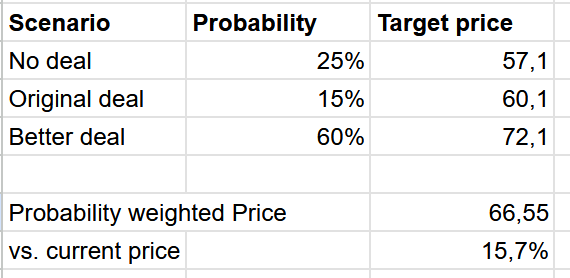

General, I might see the possibilities as follows till the tip of the yr::

25% likelihood of no take care of 55 GBP as the result (plus dividend, at the moment estimated at 2,10 GBP/share)

15% of a deal at 58 GBP (plus dividend)

60% likelihood of a greater deal. My guess right here can be 70 GBP plus Dividend

That is the fast and soiled calculation:

So primarily based on my assumptions, my likelihood weighted anticipated return is round 16% till yr finish. This appears engaging to me, as in my view, the draw back may be very restricted.

In fact, all of the assumptions might be challenged and adjusted.

Abstract:

So in complete I see the next scenario right here:

- The bid of 58 GBP is clearly too low

- DCC’s brief time period operational outcomes are supported by growing vitality costs

- as well as, the complete impact of the transformation “again to vitality” will materialize within the following quarter

- Different Infrastructure funds may additionally be keen on DCC

So even when the bid from KKR wouldn’t achieve success, I do suppose that the share worth has way more upside than draw back potential in the intervening time.

From that perspective, I made a decision to not promote any DCC shares however reasonably improve my place by ~1,5 % of complete portfolio worth at round 57,50 GBP per share.