In search of mortgage fee aid?

It may come with none additional enchancment in bond yields.

As a substitute, Basel re-proposal, which boils right down to improved financial institution capital necessities, may push charges decrease as banks improve their urge for food for mortgages.

However not all debtors would profit equally. Those that may muster massive down funds would see the most important affect.

And below sure fashions, charges may fall as a lot as a half level, that means a borrower dealing with a 6.375% fee in the present day may quickly qualify for a fee beneath 6%.

Basel Rule Adjustments Will Improve Financial institution Urge for food for Mortgages

It’s no secret banks have lengthy been disinterested in mortgage lending.

Publish-GFC they by no means actually got here again. Some banks participated greater than others and Wells Fargo was #1 for a short spell.

However over the previous a few years, it’s been all in regards to the nonbanks, with Rocket Mortgage the highest mortgage lender in America earlier than United Wholesale Mortgage squeezed them out.

A part of the rationale needed to do with Basel III, through which banks have been required to carry extra capital for the loans they stored on their books.

With out getting too caught within the weeds right here, banks have been disincentivized from making mortgages and preserving them because of this.

However proposed modifications may get banks again within the mortgage recreation.

For instance, the danger weight for a typical mortgage with a 75% loan-to-value ratio (LTV) may fall from 50% to 30%-35%, per the City Institute.

And for a mortgage beneath 60% LTV, from 50% to twenty%-25%. These decrease danger weightings would entice banks to lend once more, particularly at decrease LTVs.

So debtors who have been capable of put a 20% down fee or extra on a house buy would be capable of snag higher pricing on their mortgage.

How A lot Decrease Would Mortgage Charges Be?

How a lot decrease?

Nicely, it relies upon, but it surely seems to be fairly sizable.

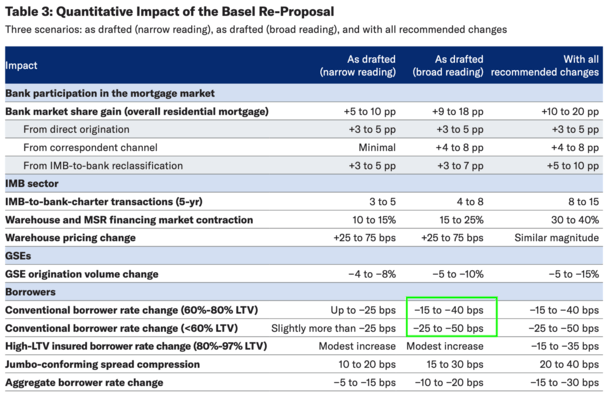

The City Institute laid out a chart with the Basel Re-Proposal as drafted with slim and broad readings, together with really helpful modifications.

Once more, with out getting too deep right here, the affect is sizable.

A standard mortgage borrower would see a 30-year mounted anyplace from 15 to 40 foundation factors decrease.

For instance, in case your quote was 6.375% in the present day, maybe it’s 5.99% thanks to those modifications.

Assuming mortgage charges finally drift again to these sub-6% ranges we noticed in February, perhaps you’re nearer to five.5%.

It’s even higher for the borrower with a number of dwelling fairness or a 40%+ down fee. For these of us, a fee enchancment of as much as .50% is feasible.

So once more, a fee of 6% drops to perhaps 5.5%.

These with jumbo loans would additionally profit because the jumbo-conforming unfold narrowed as a lot as 30 foundation factors.

In a nutshell, the City Institute notes that the modifications would invite “banks to compete extra aggressively for prime typical originations, significantly low-LTV refinances and jumbo buy mortgages.”

Notably, this wouldn’t have as a lot affect on high-LTV loans or government-backed ones, similar to FHA loans and VA loans.

As well as, debtors with low down funds may see increased mortgage charges as a result of Fannie and Freddie wouldn’t generate as many low-LTV loans to offset the danger of the previous.

That would cut back the cross-subsidy that makes high-LTV loans cheaper than they in any other case could be.

Nevertheless, City has proposed improved danger weightings for loans with personal mortgage insurance coverage (PMI) as nicely, which might enhance mortgage charges on such loans by 15 to 35 bps.

Throughout the complete mortgage universe, mortgage fee pricing may very well be as much as .30% decrease. That’d be a pleasant win for dwelling consumers scuffling with affordability in the present day.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 20 years in the past to assist potential (and present) dwelling consumers higher navigate the house mortgage course of. Comply with me on X for decent takes.