THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

Once you first hear concerning the Trump Account, it’s straightforward to dismiss it as simply one other authorities program, and even tune it out due to the identify.

That might be a mistake.

Politics apart, this new funding account might grow to be one of the highly effective wealth-building instruments accessible for youngsters.

Think about giving a new child a small funding that has almost twenty years to develop earlier than they’ll contact it.

Then think about that, at age 18, when many younger adults have little or no taxable earnings, they could have a possibility to transform these financial savings right into a Roth IRA, permitting a long time of future funding progress to doubtlessly grow to be tax free.

Used strategically, that single choice may very well be value tens and even a whole bunch of 1000’s of {dollars} over a lifetime, relying on how a lot the account grows and future tax guidelines.

After all, Trump Accounts aren’t good.

They arrive with contribution limits, withdrawal guidelines, and restrictions that make them very completely different from a Roth IRA, a 529 faculty financial savings plan, or a UGMA/UTMA account.

On this information, you’ll be taught precisely how Trump Accounts work, who qualifies, how the cash is invested, what occurs when your baby turns 18, and why many monetary specialists imagine the most important alternative isn’t the $1,000 authorities contribution.

We’ll additionally evaluate Trump Accounts to different widespread financial savings choices so you may resolve whether or not they deserve a spot in your loved ones’s monetary plan.

What Is a Trump Account?

A Trump Account is a long-term funding account created for youngsters beneath the One Huge Stunning Invoice tax laws signed into legislation in 2026.

Trump Accounts give eligible newborns a $1,000 government-funded funding to assist jump-start their monetary future, and oldsters, grandparents, and others can contribute further cash every year.

Consider it as planting a tree on your baby on the day they’re born.

The earlier it’s planted, the extra time it has to develop.

Over the subsequent 18 years, the cash can doubtlessly develop by way of investments, and as soon as your baby turns into an grownup, they could have a number of choices for utilizing the account.

This features a technique that would permit a long time of future funding progress to grow to be tax free.

Not like a financial savings account that earns a small quantity of curiosity, a Trump Account is designed to be invested within the inventory market.

Whereas investments can go up and down over brief durations, historical past has proven that long-term investing has typically rewarded affected person buyers.

The largest takeaway is that this: the $1,000 authorities contribution is sweet, however the true worth comes from giving your baby’s investments as a lot time as potential to develop.

How Does a Trump Account Work?

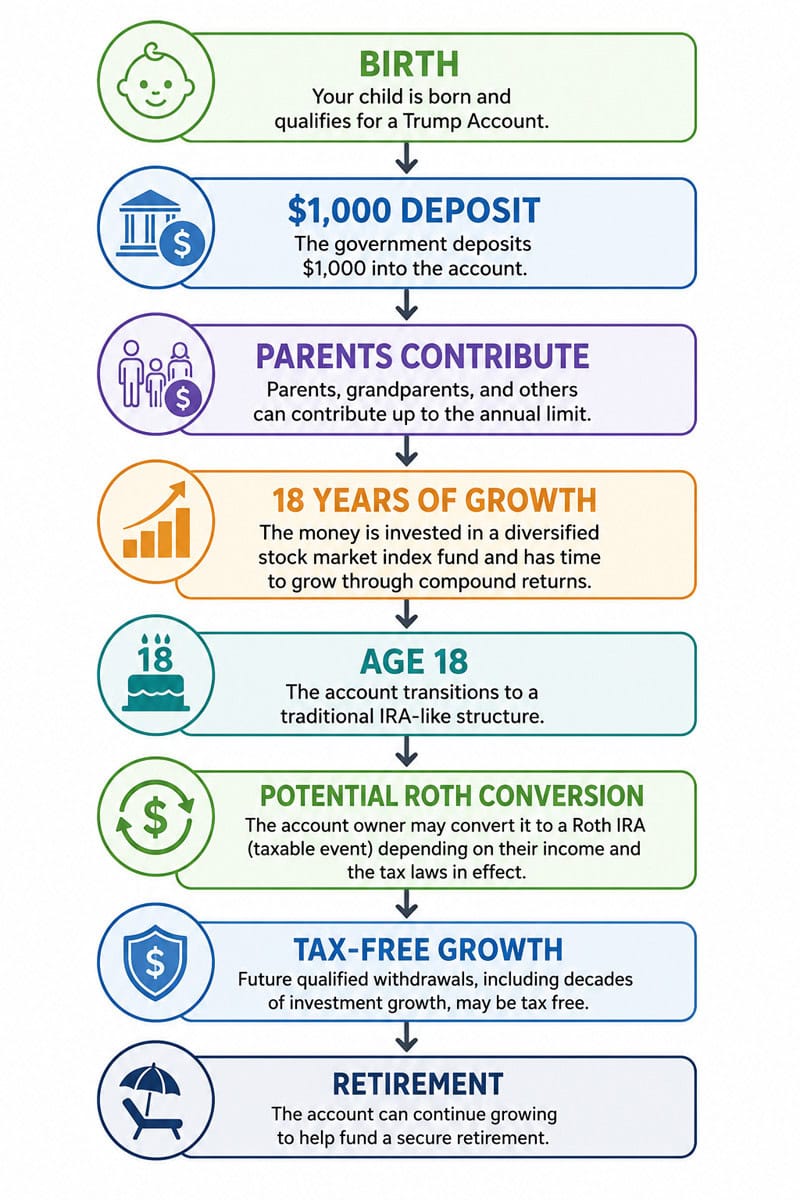

The simplest approach to perceive a Trump Account is to observe it from delivery by way of maturity.

Step 1: Your Youngster Receives the Account

In case your baby qualifies beneath this system guidelines, the federal authorities contributes $1,000 to open the account.

To qualify for the $1,000 they have to be born between 2026-2028.

Nonetheless, any baby beneath 18 years previous can open the account.

They only received’t be eligible for the $1,000.

However, Michael Dell, the founding father of Dell Computer systems, made a charitable donation of $6.25 billion.

This implies the primary 25 million American kids age 10 and beneath residing in ZIP codes with median incomes beneath $150,000 will obtain a further $250.

Step 2: Household Members can Add Cash

Dad and mom, grandparents, kinfolk, and even household mates can contribute further cash, as much as the annual contribution restrict established by legislation.

As an alternative of shopping for one other toy for each birthday, think about grandparents contributing $100 every year.

These small presents might doubtlessly develop into 1000’s of {dollars} by the point your baby turns into an grownup.

The utmost annual contribution is $5,000.

Step 3: The Cash is Invested

The funds aren’t meant to take a seat in money.

They’re invested in a diversified inventory market index fund, permitting the account to profit from long-term market progress.

Whereas no funding is assured, historical past has proven that the longer cash stays invested, the better its potential to develop by way of the facility of compound returns.

Step 4: The Account Grows Over Time

For the subsequent 18 years, contributions and funding earnings stay within the account.

You don’t should continuously monitor it or make difficult funding choices.

In some ways, it’s designed to be a “set it and overlook it” funding on your baby’s future.

Step 5: All the things Adjustments at Age 18

That is the half most articles barely point out, however it’s arguably essentially the most helpful characteristic of all the program.

As soon as your baby turns 18, the account is mostly handled very similar to a standard IRA.

That opens the door to a possible Roth IRA conversion technique that would dramatically cut back, and even eradicate, taxes on a long time of future funding progress.

We’ll cowl precisely how that works later as a result of it could be the one largest purpose dad and mom select to fund a Trump Account past the preliminary $1,000.

At a Look: How a Trump Account Works

| Age | What Occurs |

|---|---|

| Beginning | Eligible baby receives a $1,000 authorities contribution. |

| Childhood | Dad and mom, grandparents, and others can contribute further cash (topic to annual limits). |

| Beginning to 18 | The cash stays invested and has the chance to develop by way of compound returns. |

| Age 18 | The account transitions to a standard IRA-like construction, creating the potential for a Roth IRA conversion technique. |

| Maturity | The account can proceed rising for retirement or be used in response to this system’s guidelines. |

Why Dad and mom Are Paying Consideration to Trump Accounts

The largest benefit of a Trump Account isn’t the $1,000 authorities contribution, though that’s actually a pleasant bonus.

It’s the period of time the cash has to develop.

Most individuals don’t start investing till they’re of their 20s or 30s.

Many don’t even begin till later than that.

A Trump Account offers a baby an 18-year head begin earlier than they even grow to be an grownup.

That’s vital as a result of the sooner you make investments, the extra highly effective compound progress turns into.

Think about rolling a snowball down a hill.

At first, it barely grows.

However because it retains rolling, it picks up extra snow, will get greater, and begins rising quicker and quicker.

Investing works a lot the identical manner.

Your funding earns returns.

Then these returns start incomes returns of their very own. Over time, that compounding impact can grow to be extremely highly effective.

That’s why even comparatively small contributions made persistently over a few years can develop into surprisingly giant balances.

The opposite purpose many monetary planners are enthusiastic about Trump Accounts is what occurs when the kid turns 18.

As a result of many younger adults have little or no taxable earnings, they could have a possibility to transform the account to a Roth IRA whereas paying little or no federal earnings tax on the conversion.

If finished strategically, a long time of future funding progress might doubtlessly be withdrawn tax free throughout retirement.

We’ll clarify precisely how that technique works later on this information.

Who Ought to Think about Opening a Trump Account?

A Trump Account received’t be the suitable alternative for each household.

Nonetheless, it could be value contemplating should you:

- Have a new child or younger baby and wish to begin investing early.

- Need members of the family like grandparents to assist construct your baby’s future.

- Are already saving on your baby’s long-term monetary targets.

- Need one other tax-advantaged account along with a 529 plan or custodial account.

- Like the thought of giving your baby a monetary head begin earlier than maturity.

However, in case your main objective is paying for school, a 529 plan should still be a greater match.

Likewise, in case your baby already has earned earnings from a part-time job, a custodial Roth IRA affords advantages {that a} Trump Account can’t match.

The excellent news is that these accounts don’t essentially compete with each other.

Many households could discover that utilizing a number of account sorts collectively offers the best flexibility.

How A lot May a Trump Account Be Value?

Right here’s the place issues get thrilling.

Many individuals hear concerning the $1,000 authorities contribution and assume that’s all there may be to it.

In actuality, the account’s long-term worth relies upon way more on how a lot is contributed over time and the way lengthy the cash stays invested than on the preliminary deposit.

To place that into perspective, let’s have a look at a number of hypothetical examples.

We’ll assume:

- The account earns a median annual return of 8% (precise returns will differ).

- Contributions are made on the finish of every 12 months.

- The cash stays invested till age 18.

Within the subsequent part, we’ll see how completely different contribution quantities can dramatically change the account’s worth, and why even an additional $25 or $50 monthly could make a significant distinction over time.

How A lot May a Trump Account Develop?

The worth of a Trump Account depends upon how a lot is contributed and the way lengthy the cash stays invested.

The examples beneath assume:

- A $1,000 authorities contribution at delivery

- Contributions made month-to-month

- An 8% common annual funding return

- No withdrawals earlier than age 18

- After age 18, the cash stays invested with none further contributions

| Month-to-month Contribution | Estimated Worth at 18 | Estimated Worth at 30 | Estimated Worth at 65 |

|---|---|---|---|

| Authorities $1,000 solely | $4,000 | $10,100 | $148,800 |

| $25/month | $15,600 | $39,400 | $582,200 |

| $50/month | $27,300 | $68,700 | $1.02 million |

| $100/month | $50,600 | $127,300 | $1.88 million |

| $250/month | $120,400 | $303,200 | $4.48 million |

Observe: These examples assume a median annual return of 8%, which isn’t assured. Precise funding returns will differ, and account values might be greater or decrease relying on market efficiency.

Some extent value emphasizing

This desk illustrates one of many largest classes in investing: time is usually extra highly effective than the quantity you make investments.

For instance, contributing simply $50 a month (about the price of one household dinner out) might doubtlessly develop to greater than $1 million by age 65 if the cash stays invested.

The preliminary $1,000 authorities deposit is a pleasant head begin, however the true wealth comes from making common contributions, permitting compound progress to work for many years, and avoiding the temptation to withdraw the cash early.

Why Age 18 May Be the Greatest Alternative

Probably the most talked-about characteristic of a Trump Account is the $1,000 authorities contribution.

Paradoxically, which will find yourself being one in all its least helpful advantages.

The actual alternative comes when your baby turns 18 years previous.

At that time, the account is mostly handled very similar to a standard IRA.

Which means the account proprietor could have the choice to convert it to a Roth IRA by paying earnings tax on the transformed quantity.

At first, paying taxes may sound like a nasty thought.

In actuality, it may very well be one of many smartest monetary choices your baby ever makes.

The rationale comes down to 1 easy reality: Most 18-year-olds have little or no taxable earnings.

Many are nonetheless in highschool, beginning faculty, or working part-time jobs.

As a result of their earnings is usually a lot decrease than it will likely be later in life, they could qualify for one of many lowest federal earnings tax brackets they’ll ever see.

That creates a novel window of alternative.

As an alternative of ready till they’re of their 30s or 40s and incomes a a lot greater wage, they can pay taxes on the account whereas their tax invoice is comparatively small.

As soon as the cash is inside a Roth IRA, future certified withdrawals, together with a long time of funding progress, can typically be taken tax free.

After all, whether or not changing all the account directly is the perfect technique depends upon the kid’s earnings, tax state of affairs, and the tax legal guidelines in impact on the time.

That’s why it’s vital to guage the numbers earlier than making a call.

A Easy Instance

Let’s see how this may work.

Think about Emma turns 18 with $50,000 in her Trump Account.

She plans to attend faculty and works a part-time job that earns $8,000 through the 12 months.

As a result of her taxable earnings is comparatively low, changing some or the entire account to a Roth IRA might end in a a lot smaller tax invoice than if she waited till she had a full-time profession.

Now think about she leaves that cash invested till age 65.

If her investments common an 8% annual return, that $50,000 might doubtlessly develop to almost $1.9 million.

If the conversion was accomplished beneath the Roth IRA guidelines and all necessities have been met, that future progress might doubtlessly be withdrawn tax free.

Right here’s what makes this instance so exceptional.

Emma by no means contributed one other greenback to this account after turning 18.

She merely left the cash invested and allowed compound progress to do the heavy lifting.

By retirement, that unique $50,000 had the potential to develop to almost $1.9 million, all with out including one other penny to the account.

Take into consideration how that would change her monetary future.

As an alternative of worrying about whether or not she’s saving sufficient for retirement, Emma already has a considerable nest egg working for her earlier than she’s even began her profession.

Each greenback she saves in her 20s, 30s, and past might grow to be further retirement financial savings as an alternative of making an attempt to catch up.

She has extra flexibility to purchase a house, begin a enterprise, increase a household, change careers, and even retire earlier as a result of she started investing a long time earlier than most individuals ever do.

That’s the true energy of time.

The federal government’s preliminary contribution could have opened the door, however permitting these investments to develop for many years is what has the potential to create life-changing wealth.

That’s why many monetary professionals imagine the conversion, not the preliminary $1,000 deposit, could finally grow to be essentially the most helpful characteristic of all the program.

Why Changing Earlier Can Save 1000’s in Taxes

Take into consideration two completely different folks.

Emma converts at age 18.

- Earnings: $8,000

- Trump Account: $50,000

- Pays taxes whereas her earnings may be very low.

- Future progress has a long time to compound inside a Roth IRA.

Alex waits till age 35.

- Earnings: $95,000

- Trump Account: $120,000

- A lot greater tax bracket.

- Bigger tax invoice on the conversion.

- Fewer years of tax-free progress remaining.

Neither technique is mechanically proper or fallacious.

However this instance highlights why many households are already speaking concerning the age 18 conversion technique.

Paying taxes when your earnings is low can generally be less expensive than paying them later whenever you’re incomes considerably extra.

Necessary Issues to Know Earlier than Changing

Earlier than changing a Trump Account to a Roth IRA, hold these factors in thoughts:

- A Roth conversion is mostly a taxable occasion.

- The quantity you change is added to your taxable earnings for the 12 months.

- Changing an excessive amount of directly might push you into a better tax bracket.

- Some folks could profit from spreading conversions over a number of years quite than changing every part directly.

- Tax legal guidelines can change, so it’s vital to know the principles that apply when your baby reaches age 18.

As a result of each household’s state of affairs is completely different, it’s typically value talking with a professional tax skilled earlier than deciding how a lot to transform.

Ought to You Convert All at As soon as or Over A number of Years?

We might evaluate eventualities like:

| Technique | Professionals | Cons |

|---|---|---|

| Convert every part at 18 | Maximizes tax-free progress; could reap the benefits of very low earnings | May create a bigger tax invoice in a single 12 months |

| Convert over 4 years (18–21) | Helps handle tax brackets; spreads out the tax price | Much less cash begins compounding tax-free instantly |

| Wait till after faculty | Should still have low earnings | Threat of coming into a better tax bracket if earnings rises shortly |

Trump Account vs. Roth IRA

At first look, a Trump Account and a Roth IRA may appear related as a result of each are designed to assist construct long-term wealth.

Nonetheless, they serve completely different functions and have completely different guidelines.

The largest distinction is who can open the account and when.

A toddler can obtain a Trump Account at delivery (in the event that they qualify), giving their investments as much as 18 further years to develop earlier than they grow to be an grownup.

A Roth IRA, then again, requires earned earnings.

In different phrases, your baby should have earnings from a job or self-employment earlier than they’ll contribute.

That’s why many monetary planners don’t view these accounts as opponents.

As an alternative, they’ll complement each other at completely different phases of life.

| Characteristic | Trump Account | Roth IRA |

|---|---|---|

| Who can open one? | Eligible newborns and youngsters | Anybody with earned earnings who meets IRS guidelines |

| Authorities contribution | Sure, for eligible kids | No |

| Dad and mom can contribute | Sure, topic to annual limits | No, until the kid has earned earnings and contributions don’t exceed that earnings |

| Funding progress | Tax deferred | Tax free (if certified withdrawal guidelines are met) |

| Age requirement | Begins at delivery | Requires earned earnings |

| Greatest For | Giving kids an investing head begin | Lengthy-term retirement financial savings |

Which One Is Higher?

In case your baby has earned earnings, a Roth IRA remains to be probably the greatest retirement accounts accessible as a result of certified withdrawals are tax free.

However newborns and younger kids don’t have jobs.

That’s the place a Trump Account fills an vital hole.

As an alternative of ready till your baby will get their first summer season job at 16 or 17, they’ll start investing from delivery.

These further years of compound progress might make an amazing distinction over the long run.

In truth, one potential technique is to make use of each accounts.

A toddler may benefit from a Trump Account whereas they’re younger after which start contributing to a Roth IRA as soon as they begin incomes earnings.

If the Trump Account is ultimately transformed to a Roth IRA at age 18, they might find yourself with a long time of tax-free progress and proceed including to that Roth all through their working years.

The important thing takeaway is that this: you don’t have to decide on one or the opposite.

Relying in your baby’s state of affairs, these accounts can work collectively to construct long-term wealth.

Trump Account vs. 529 Plan

In case your objective is saving on your baby’s future, you’ve most likely heard of a 529 plan.

Like a Trump Account, it’s designed to assist households make investments over a few years.

However whereas these accounts have some similarities, they’re constructed for very completely different functions.

A 529 plan is primarily a school financial savings account.

It affords helpful tax benefits when the cash is used for certified training bills, akin to tuition, books, charges, and sure housing prices.

A Trump Account, then again, is targeted on long-term wealth constructing.

Whereas there are guidelines governing when and the way the cash can be utilized, many households are most enthusiastic about the potential of changing the account to a Roth IRA at age 18 and permitting the investments to proceed rising tax free for retirement.

In easy phrases:

- A 529 plan helps pay for school.

- A Trump Account could assist construct lifelong wealth.

Neither account is mechanically higher. It relies upon totally on your loved ones’s targets.

| Characteristic | Characteristic | 529 Plan |

|---|---|---|

| Main Goal | Lengthy-term investing and wealth constructing | Saving for training |

| Authorities Contribution | Sure, for eligible kids | No |

| Tax Advantages | Tax-deferred progress with potential Roth conversion technique | Tax-free progress when used for certified training bills |

| Greatest For | Retirement and long-term investing | Faculty and training prices |

| Funding Choices | Restricted by program guidelines | Large number of funding portfolios |

| Can Dad and mom Contribute? | Sure | Sure |

Which One Ought to Dad and mom Select?

If paying for school is your highest precedence, a 529 plan remains to be troublesome to beat as a result of certified withdrawals are typically tax free.

Nonetheless, in case your objective is giving your baby the best potential head begin towards monetary independence, a Trump Account deserves severe consideration.

Many households could uncover they don’t want to decide on between the 2.

A 529 plan will help pay for school, whereas a Trump Account will help fund retirement a long time later.

Collectively, they create a balanced technique that prepares your baby for each main milestones.

Trump Account vs. UGMA and UTMA Accounts

A UGMA or UTMA account is one other widespread manner dad and mom and grandparents make investments for youngsters.

Not like a Trump Account or a 529 plan, these are custodial accounts, that means an grownup manages the cash till the kid reaches the age of majority of their state.

The largest benefit of a UGMA or UTMA account is flexibility.

The cash can typically be used for nearly any function that advantages the kid.

That might embody training bills, shopping for a automotive, beginning a enterprise, or making a down cost on a primary dwelling.

The tradeoff is that there are fewer tax benefits than with retirement-focused accounts.

One other vital distinction is possession.

As soon as your baby reaches the age specified beneath your state’s legal guidelines, the cash legally turns into theirs.

They will typically spend it nevertheless they select—even should you had one thing else in thoughts.

With a Trump Account, the cash stays targeted on long-term monetary targets beneath this system’s guidelines.

| Characteristic | Trump Account | UGMA/UTMA |

|---|---|---|

| Main Goal | Lengthy-term investing | Common financial savings and investing |

| Authorities Contribution | Sure, for eligible kids | No |

| Tax Benefits | Tax-deferred progress with potential Roth conversion technique | Restricted tax benefits |

| Funding Flexibility | Restricted by program guidelines | Broad funding decisions |

| Use of Funds | Topic to program guidelines | Almost any expense that advantages the kid |

| Who Controls the Cash? | Account proprietor beneath program guidelines | Youngster positive aspects full management on the age of majority |

Which Account Is Higher?

If flexibility is your prime precedence, a UGMA or UTMA account could also be a greater match.

In case your objective helps your baby construct long-term wealth and doubtlessly retire with a considerable nest egg, a Trump Account could provide better benefits due to its tax therapy and the potential of a Roth IRA conversion at age 18.

One factor many dad and mom overlook is that flexibility isn’t at all times a bonus.

Some households really want having restrictions in place if it encourages their baby to go away the cash invested quite than spending it shortly after changing into an grownup.

Which Account Ought to You Select?

There isn’t a single “greatest” account for each household.

As an alternative, select the account that greatest matches your objective.

| In case your objective is… | Think about… |

|---|---|

| Paying for school | 529 Plan |

| Serving to a baby construct retirement financial savings from delivery | Trump Account |

| Investing for a kid who already has earned earnings | Roth IRA |

| Most flexibility for future bills | UGMA/UTMA |

| Constructing the strongest long-term plan | A mix of a number of accounts |

For a lot of households, the reply isn’t selecting one account over one other—it’s utilizing every account for what it does greatest.

For instance, grandparents may contribute to a Trump Account to assist construct long-term wealth, dad and mom may save in a 529 plan for future training prices, and as soon as the kid will get their first job, they might start contributing to a Roth IRA.

That mixture offers the kid a powerful monetary basis for school, retirement, and every part in between.

5 Widespread Trump Account Errors Dad and mom Ought to Keep away from

A Trump Account has the potential to grow to be a helpful monetary instrument, however merely opening one isn’t sufficient.

The choices you make over the subsequent 18 years can have a a lot greater affect than the preliminary $1,000 authorities contribution.

Listed below are 5 frequent errors to keep away from.

1. Considering the $1,000 Authorities Contribution Is Sufficient

Receiving $1,000 from the federal government is a good begin, however it’s unlikely to develop into life-changing wealth by itself.

The actual energy of a Trump Account comes from making further contributions every time potential.

Even small quantities, akin to $25 or $50 a month, can add up considerably because of compound progress.

If grandparents ask what your baby needs for birthdays or holidays, contemplate suggesting a contribution to their Trump Account as an alternative of one other toy they’ll outgrow in a number of months.

2. Ready Too Lengthy to Begin Contributing

Time is among the largest benefits this account affords.

Yearly you delay making contributions is one much less 12 months your cash has to develop.

Consider compound progress like planting a tree. One of the best time to plant it was years in the past. The second-best time is right this moment.

Even should you can’t afford giant contributions, beginning small is usually higher than ready till you may make investments extra.

3. Forgetting In regards to the Age 18 Roth Conversion Alternative

Many articles focus nearly totally on the federal government’s preliminary contribution.

In actuality, one of the helpful options of the account could come 18 years later.

Relying on the tax legal guidelines in impact and your baby’s earnings, changing the account to a Roth IRA whereas they’re in a low tax bracket might permit a long time of future funding progress to be withdrawn tax free.

That doesn’t imply changing all the stability directly is at all times the suitable transfer, however it’s a method value evaluating quite than overlooking.

4. Ignoring the Tax Affect of a Conversion

Whereas changing to a Roth IRA could be a highly effective technique, it’s vital to keep in mind that Roth conversions are typically taxable.

Changing a really giant stability in a single 12 months might enhance your baby’s taxable earnings and doubtlessly push them into a better tax bracket.

In some conditions, it could make extra sense to transform the account over a number of years as an alternative of unexpectedly.

The correct strategy depends upon the account stability, your baby’s earnings, and the tax guidelines in place on the time.

5. Assuming This Ought to Be Your Solely Financial savings Account

A Trump Account might be a wonderful addition to your loved ones’s monetary plan, however it doesn’t have to interchange each different financial savings account.

Every account serves a distinct function.

- A 529 plan is designed primarily for training bills.

- A Roth IRA is good as soon as your baby has earned earnings.

- A UGMA or UTMA account affords flexibility for a variety of future bills.

- A Trump Account is designed to offer kids a long-term investing head begin.

Many households could profit from utilizing a couple of account as an alternative of looking for a single resolution that does every part.

Steadily Requested Questions About Trump Accounts

What’s a Trump Account?

A Trump Account is a long-term funding account created for eligible kids beneath laws signed into legislation in 2026.

The federal authorities contributes $1,000 to qualifying accounts, and oldsters, grandparents, and others could make further contributions every year.

The cash is invested with the objective of rising over time and serving to construct long-term monetary safety.

Who qualifies for a Trump Account?

Typically, kids born after this system’s efficient date who meet the eligibility necessities established by legislation can obtain a Trump Account.

As a result of eligibility guidelines can change, it’s vital to evaluation essentially the most present IRS steerage or communicate along with your monetary establishment earlier than opening an account.

How a lot cash are you able to contribute to a Trump Account?

Along with the federal government’s preliminary contribution, members of the family and others could contribute as much as the annual restrict established beneath the legislation.

These limits could change over time, so test the present IRS guidelines earlier than making contributions.

Can grandparents contribute to a Trump Account?

Sure. Grandparents, kinfolk, and even household mates could possibly contribute to a baby’s Trump Account, topic to this system’s annual contribution limits.

This makes birthdays, holidays, and different particular events an important alternative to offer a present that would proceed rising for many years.

How is the cash invested?

Trump Accounts are designed to put money into a diversified inventory market index fund quite than maintaining the cash in money.

Whereas investments can lose worth within the brief time period, historical past has proven that long-term investing has typically produced greater returns than conventional financial savings accounts.

What occurs when my baby turns 18?

One of the vital vital options of a Trump Account happens at age 18.

At that time, the account is mostly handled very similar to a standard IRA. Relying in your baby’s earnings, tax state of affairs, and the legal guidelines in impact on the time, they could have the chance to transform some or the entire account to a Roth IRA.

Whereas the conversion is mostly taxable, future certified withdrawals from the Roth IRA may very well be utterly tax free.

Ought to my baby convert all the account to a Roth IRA at age 18?

Not essentially.

Changing all the stability instantly will be the proper technique for some households, however not for others.

As a result of Roth conversions are typically taxable, a big conversion might transfer your baby into a better tax bracket.

Some households could profit from changing all the account whereas the kid has little or no earnings, whereas others could want spreading the conversion over a number of years.

One of the best strategy depends upon the account stability, your baby’s earnings, and the tax legal guidelines in impact on the time.

Is a Trump Account higher than a 529 plan?

It depends upon your targets.

In case your main goal is paying for school, a 529 plan typically affords the best tax advantages for certified training bills.

In case your objective is giving your baby a long-term funding that would doubtlessly develop for retirement, a Trump Account will be the better option.

Many households could resolve to make use of each accounts as a part of a broader monetary plan.

Is a Trump Account higher than a Roth IRA?

These accounts are designed for various conditions.

A Roth IRA requires earned earnings, so most younger kids aren’t eligible to contribute.

A Trump Account permits investing to start a lot earlier in life.

As soon as the kid has earned earnings, they could additionally start contributing to a Roth IRA, and at age 18 they could even have the chance to transform the Trump Account to a Roth IRA.

For a lot of households, the perfect technique isn’t selecting one over the opposite.

It’s utilizing each when acceptable.

Can a Trump Account lose cash?

Sure.

As a result of the account is invested within the inventory market, its worth can rise and fall over time.

Brief-term losses are potential, particularly throughout market downturns.

Nonetheless, the account is designed for long-term investing.

Traditionally, broad inventory market index funds have typically rewarded buyers who remained invested for a few years.

What occurs if my baby doesn’t go to school?

Not like a 529 plan, a Trump Account isn’t primarily designed for training financial savings.

Whether or not your baby attends faculty, enters the workforce, begins a enterprise, or joins the navy, the account continues to exist beneath this system’s guidelines.

Many households are most excited about utilizing it as a long-term retirement and wealth-building instrument quite than a school financial savings account.

Are Trump Accounts value it?

For a lot of households, the reply could also be sure.

The $1,000 authorities contribution offers an instantaneous head begin, however the largest benefit is the chance to start investing from delivery.

Mixed with common contributions, a long time of compound progress, and a fastidiously deliberate Roth IRA conversion technique at age 18, a Trump Account has the potential to grow to be a significant a part of your baby’s long-term monetary future.

The important thing isn’t the scale of the preliminary deposit.

It’s giving your baby’s cash as a lot time as potential to develop.

Last Ideas

Whether or not you like the identify or hate it, the truth is {that a} Trump Account is solely one other monetary instrument. And like every monetary instrument, its worth depends upon how you employ it.

The $1,000 authorities contribution is a pleasant head begin, however it isn’t what has the potential to alter your baby’s monetary future.

The actual alternative comes from beginning early, contributing persistently, permitting compound progress to work for many years, and punctiliously planning what occurs when your baby turns 18.

For a lot of households, the age-18 Roth IRA conversion technique could show to be essentially the most helpful characteristic of all the program.

In case your baby can convert the account whereas they’re in a low tax bracket, a long time of future funding progress might doubtlessly be withdrawn tax free, a profit that may very well be value excess of the federal government’s preliminary contribution.

After all, a Trump Account isn’t a substitute for each different financial savings account.

Relying on your loved ones’s targets, it could work greatest alongside a 529 plan, a Roth IRA, or different funding accounts.

The secret is understanding what every account is designed to do and utilizing the suitable instrument for the suitable job.

On the finish of the day, the most important lesson has nothing to do with politics and even this particular account.

The sooner you begin investing, the extra time your cash has to develop.

Whether or not it’s $25 a month, birthday presents from grandparents, or bigger annual contributions, each greenback invested right this moment has the potential to grow to be many extra {dollars} a long time from now.

Your baby received’t keep in mind each toy they acquired rising up. However sooner or later, they could be extremely grateful that you simply gave them one thing much more helpful…a monetary head begin that lasts a lifetime.