DISCLAIMER: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!

Abstract

On this replace put up, I take a look at two of my French inventory positions, STEF SA and Gerard Perrier. For STEF, I diminished my place by 1% of the portfolio due to issues with the mixing of newly acquired corporations. In distinction, I elevated my Gerard Perrier place by 1,5% of the Portfolio as enterprise is accelerating they usually appear to have made some excellent acquisitions within the Protection/Aerospace and Digital area.

STEF SA

Stef is an organization that I analyzed and wrote about 2 years in the past. In essence, I thought of it an affordable however dependable infrastructure-like cold-storage firm with an incredible monitor file that’s consolidating a number of European markets. For such a “compounder”, the worth regarded very low cost at round 8xP/E.

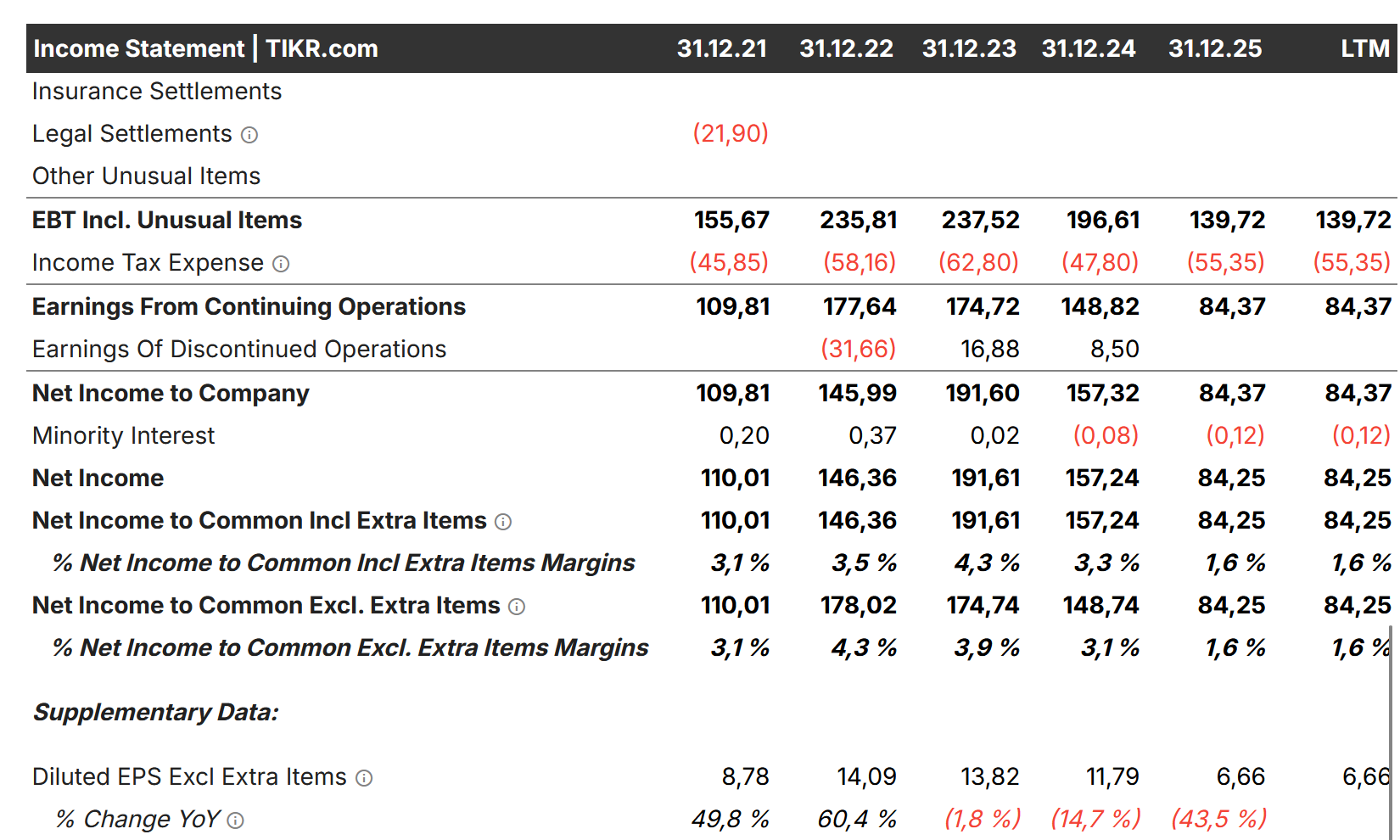

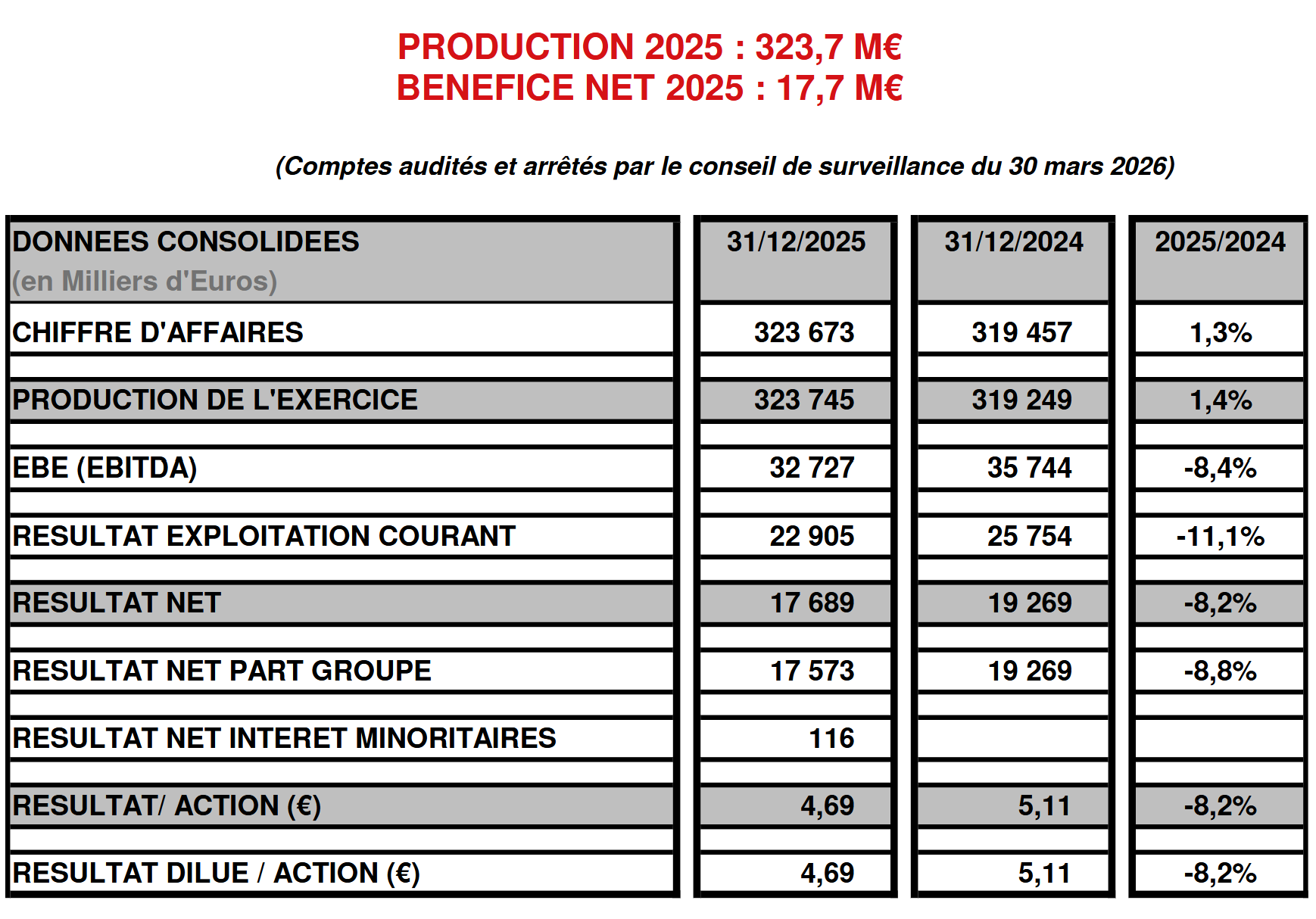

Nevertheless, issues turned out just a little in another way than I assumed. Whereas 2024 was just a little bit weaker than 2024, 2025 noticed a big decline in EPS to a degree of lower than 50% of the 2023 earnings.

In accordance with the 2025 investor presentation, this was a mix of one-time results (Tax France, VAT Italy) and slower than anticipated integration success in its latest acquisitions.

To my very own discredit, I didn’t observe up on the 6M gross sales launch from STEF which nonetheless regarded good. I ought to have regarded on the full half yr report as an alternative.

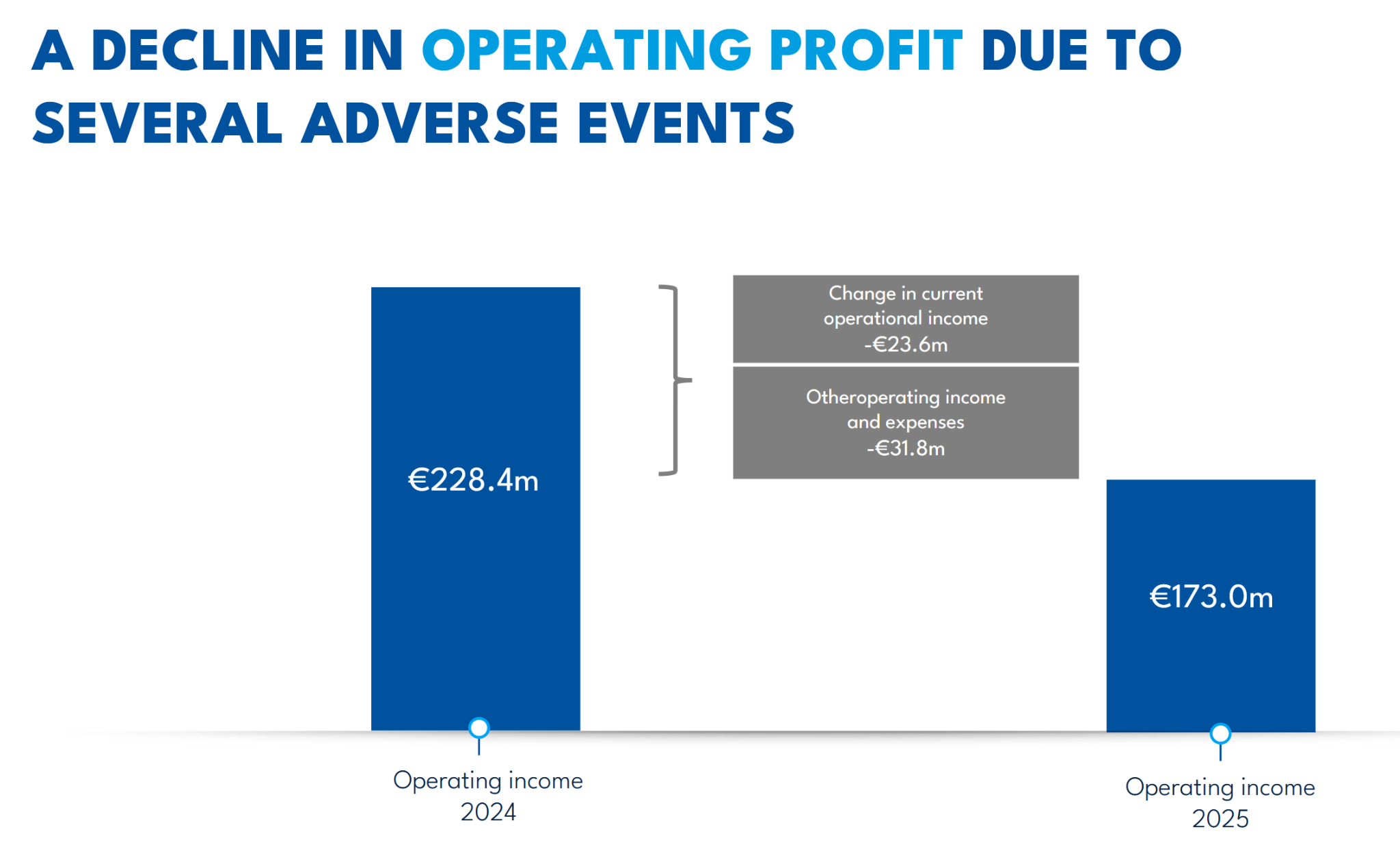

That is how the clarify the declin:

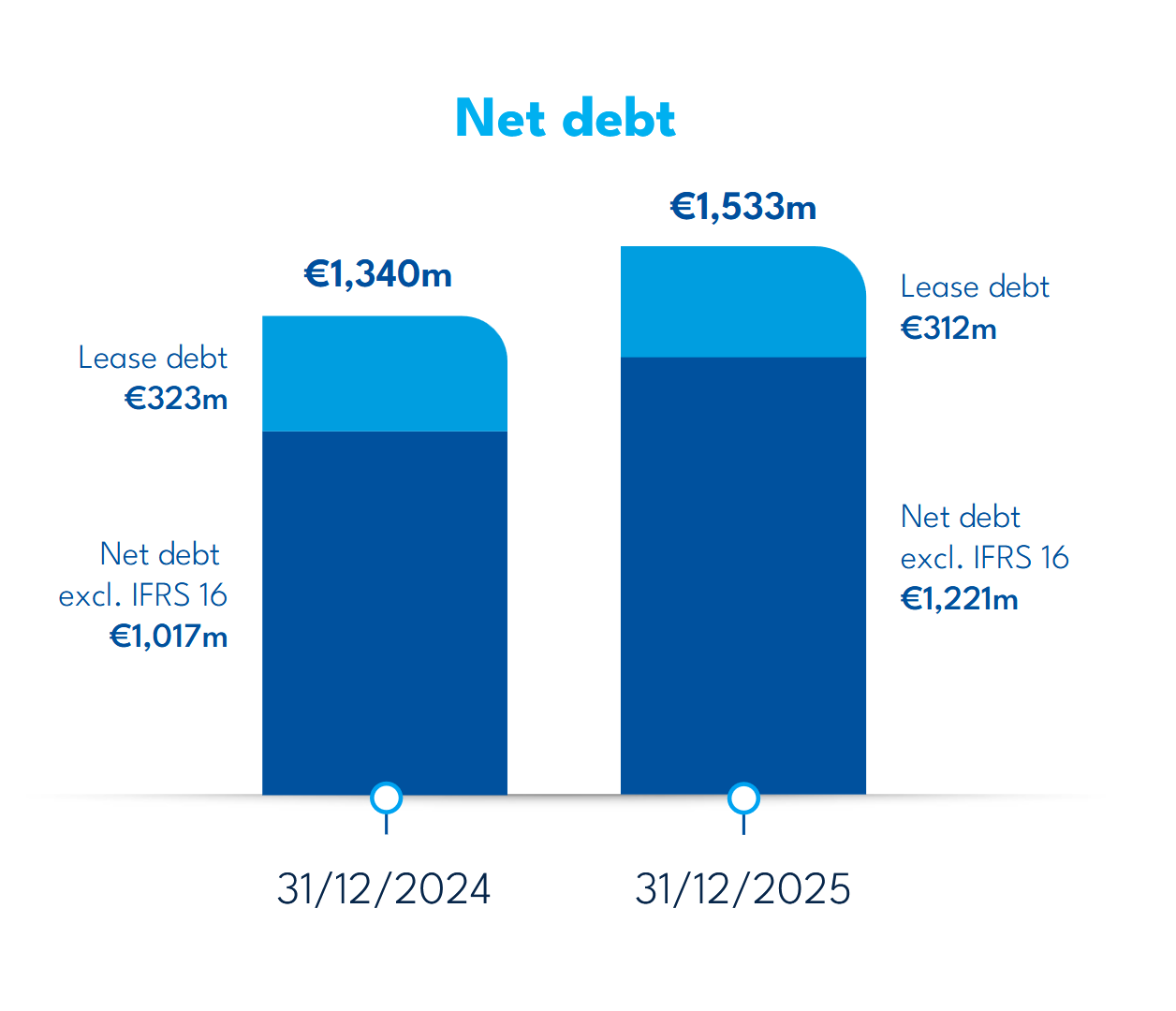

Additionally, web debt elevated by 200 mn.

The dividend was lower to 2,70 EUR from 4,15 EUR the yr earlier than (and 5,10 EUR in 2023). That is comprehensible from an organization perspective however considerably unlucky for buyers.

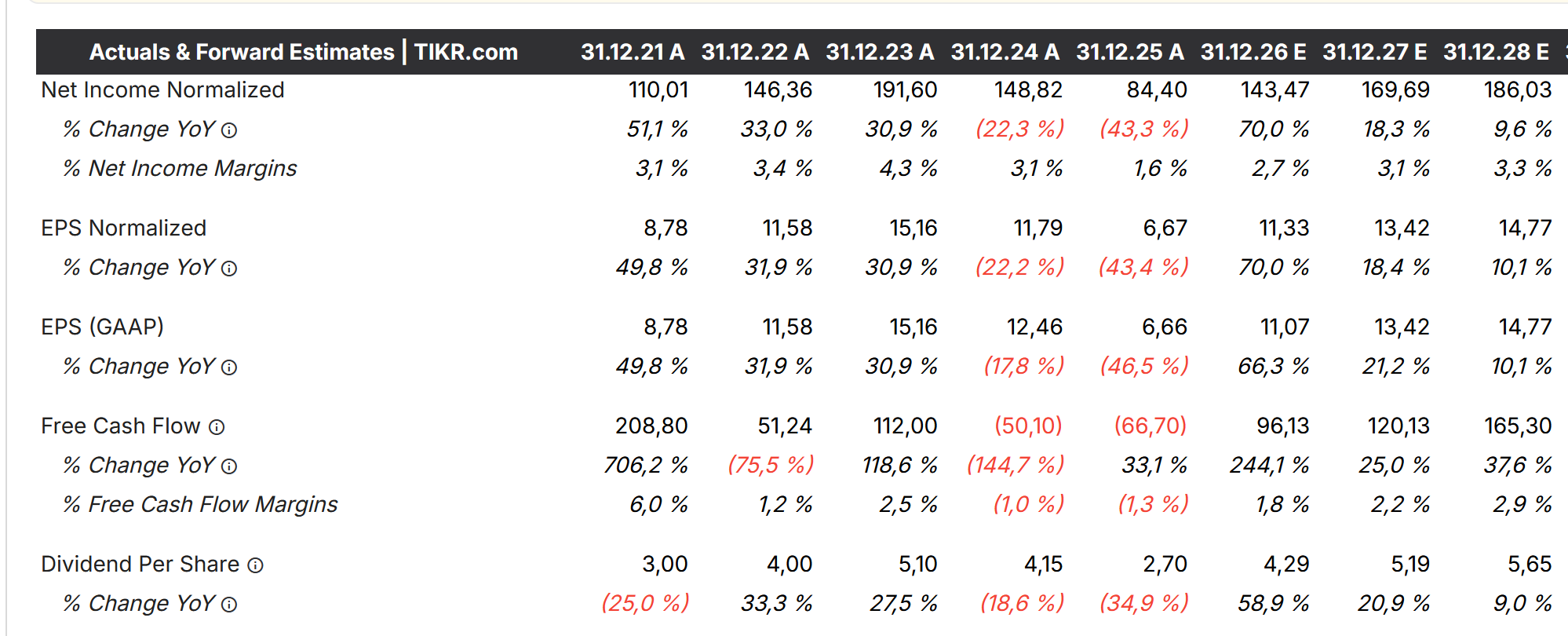

Analyst estimates appear to count on a restoration in 2026 and the next years based on TIKR:

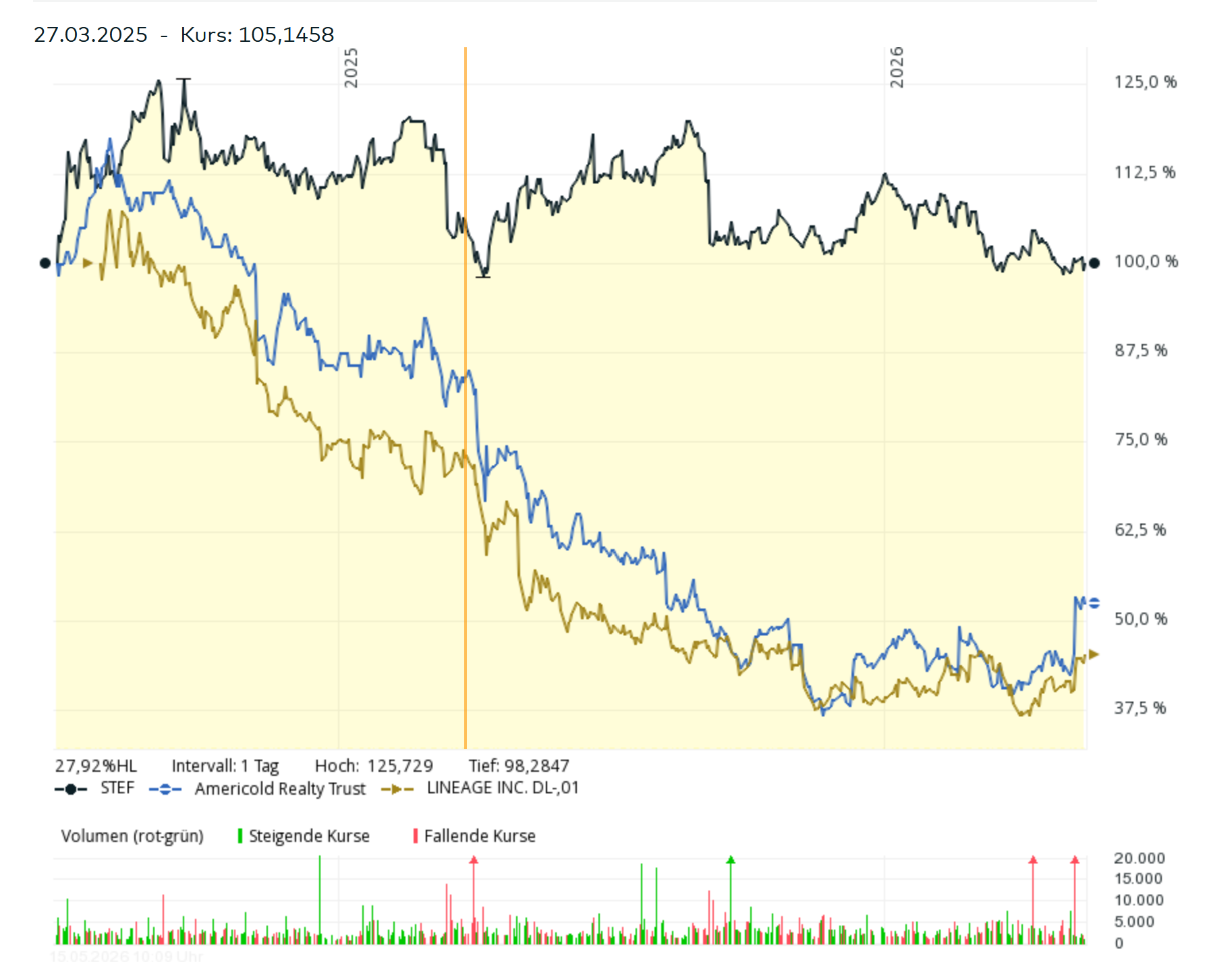

Share worth smart, the inventory is nearly precisely the place it was once I wrote up STEF. Apparently the US friends did a lot worse:

A fast look into Americold’s 2025 press launch exhibits decliningorganic gross sales and point out of “speculative developments” within the chilly storage business.

Additionally Lineage reported declining gross sales in 2025.

Each US friends are extraordinarily extremely leveraged (8x EV/EBITDA) and due to this fact very susceptible to adverse financial developments. Nevertheless, additionally STEF’s web debt to EBITDA ratio elevated from 2,5x in 2023 to three,5x in 2025. Nonetheless manageable but when rates of interest improve, it will signify one other headwind for them.

My conclusion at this stage is that Stef clearly has over-extended itself with its acquisitions within the neighbouring nations and has not been capable of combine them efficiently to date.

Administration mentions that issues ought to “normalize” in 2026 and Q1 income regarded okay, however expertise exhibits that the complete integration of the newly acquired firm can take far more time.

Though I’m not able to throw within the towel but, I do suppose that my preliminary 5% allocation (at present 4,5%) was too excessive and diminished the place by 1% of the portfolio to ~3,5%.

The constructive side of this story is clearly that I purchased low cost sufficient which protected me in opposition to a big lack of invested capital.

Gerard Perrier

On the floor, Gerard Perrier is just a little bit just like Stef insofar as 2025 was a yr when earnings went down barely:

Regardless of nonetheless rising gross sales, EPS was -8% decrease than in 2024. 2024 once more was kind of unchanged from 2023.

In Gerard Perrier’s case nevertheless, the reason shouldn’t be that they didn’t combine new acquisition however a temporal weak spot of their Vitality section which includes largely the servicing of the French nuclear fleet.

That is the interpretation (from Gemini) from G. Perriers report:

“The exercise of the Vitality division (ARDATEM, TECHNISONIC), which incorporates companies for the nuclear sector, noticed its manufacturing lower by 8.2%, falling from €89.8 million to €82.4 million. This slowdown is especially defined by the transitional impact of the discount in reactor outages and upkeep actions at energy crops this yr, in addition to by a rationalization coverage of nuclear operations in France, though the sector stays on a constructive dynamic within the medium time period.”

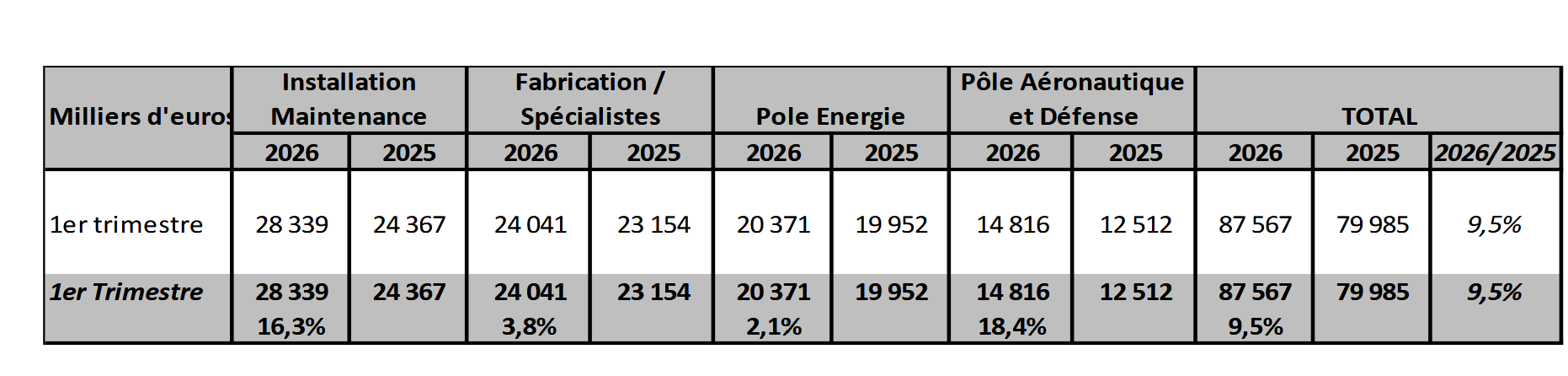

As well as, even with out a lot development within the Vitality section to date, G. Perrier had an incredible begin into 2026 with gross sales up by +10% yoy:

As we are able to see, particularly the “Set up Upkeep” and the Aerospace/Protection segments are doing effectively.

What I discovered attention-grabbing is that there was nearly no response to this information within the share worth:

What I do like is that their latest acquisitions look very attention-grabbing. With N-Cyp they acquired a small specialist firm for industrial cyber protection, with OFATEC they get entry to the Information Heart market and with the acquisition of the three corporations AQLE, SOMALEC et SOMALEC SUPPLY they strengthened their protection/aerospace section, together with parts for the Ariane Area missile program.

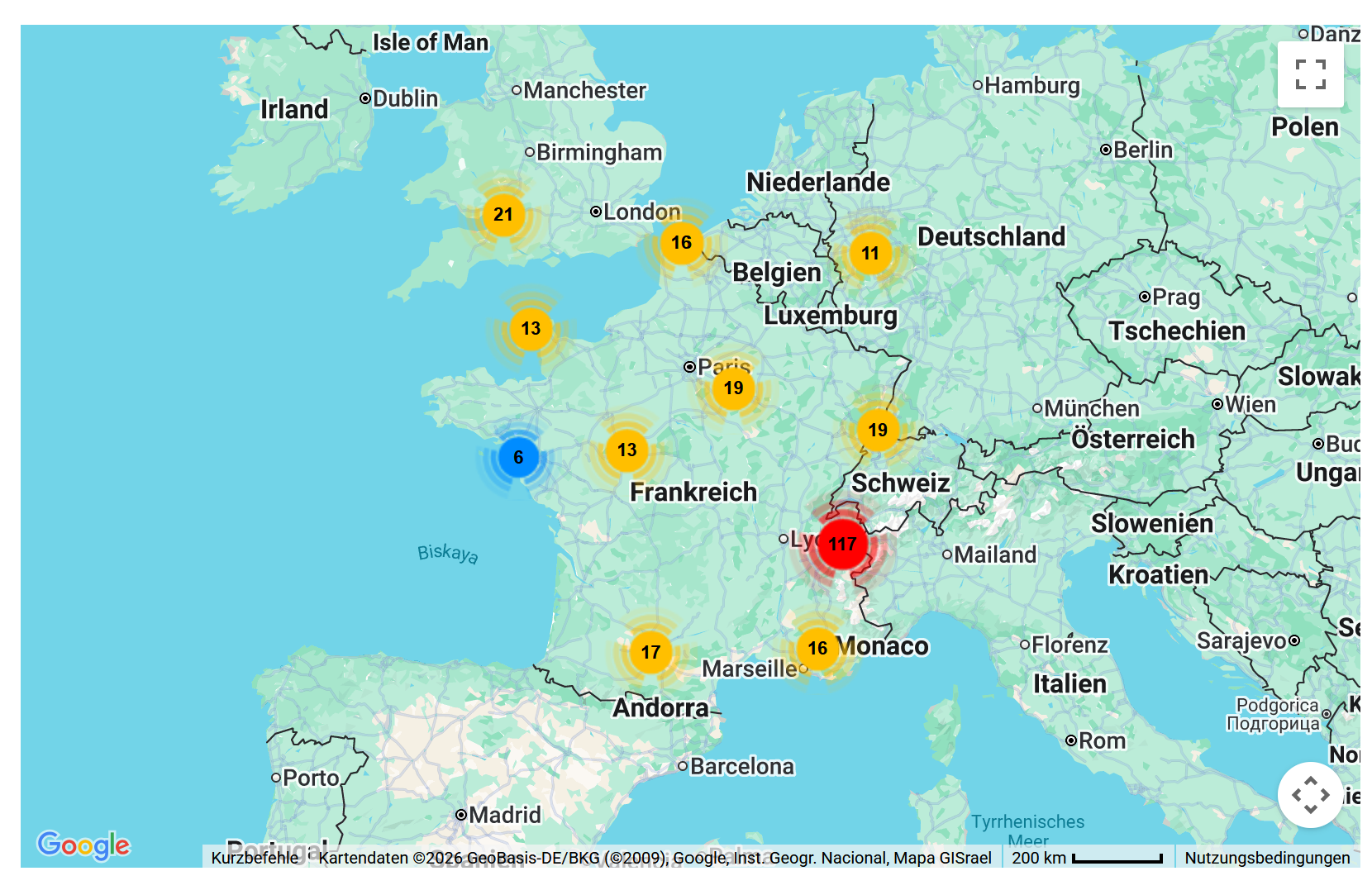

One other knowledge level that I discovered attention-grabbing is that G. Perrier has nonetheless round 230 open positions as per their website:

Many of the jobs are open at Ardatem (137), the Nuclear service firm, which appears to suggest that they count on much more work going ahead.

General, I do suppose that Gerard Perrier provides a really enticing return/threat profile particularly on the premise of the at present accelerating enterprise numbers, due to this fact I elevated my place from a earlier 3,5% weight to five% of the portfolio. The extra 1,5% have been purchased at a mean worth of round 83 EUR per share.