Background & Hi there Japan

There was a number of noise round Berkshire’s 10 bn participation within the Alphabet capital enhance. Nevertheless, on the Berkshire AGM, Greg Ready principally singled out the funding of Berkshire into Japanese Insurer Tokio Marine as an incredible funding.

He additionally talked about explicitly that this was Ajit Jain’s concept. Many Berkshire Aficionados know in fact that Ajit is behind the rise and success of Berkshires Insurance coverage enterprise.

So when Ajit is brokering a cope with Tokio Marine, I made a decision to have a primary look into this firm regardless of having by no means checked out a Japanese firm extra severely.

Subsequently “Hi there Japan” for the primary time on the weblog.

Apparently, I used to be not capable of finding any actual write-ups on Substack, just some very “mild” ones mentioning the Berkshire partnership. The “Buffetologists” have ignored that one to this point.

The Berkshire deal

The Berkshire Cope with Tokio Marine covers the next “legs” in keeping with Tokio Marine’s webpage:

Strategic Funding: NICO acquired a 2.49% stake in Tokio Marine Holdings for roughly $1.8 billion, with choices to extend its holding as much as 9.9%. To my understanding, Tokio Marine bought Treasury shares to Berkshire.

Reinsurance Settlement: Berkshire entered a whole-account quota-share reinsurance association, absorbing a portion of Tokio Marine’s globally diversified portfolio to assist the Japanese insurer mitigate pure disaster and underwriting volatility.

M&A Collaboration: Each firms plan to collaborate on world M&A and strategic funding alternatives.

Technically, the funding is finished by NICO (Nationwide Indemnity), not Berkshire. The third half is admittedly attention-grabbing and distinctive. It is going to be attention-grabbing to see how this could look in apply.

Tokio Marine overview

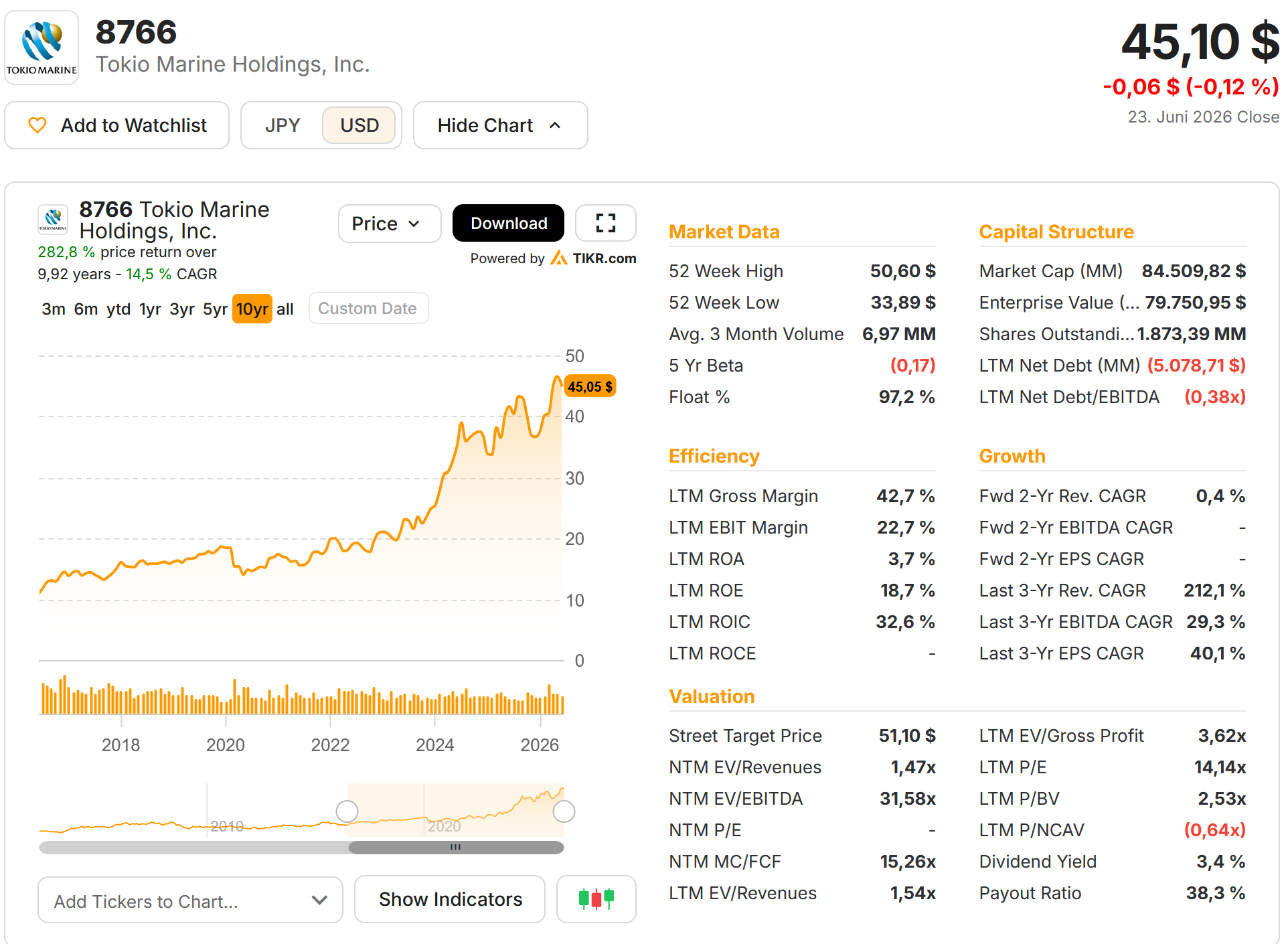

Trying on the TIKR overview, we are able to see that Tokio Marine has a market cap of round 85 bn USD, is kind of worthwhile and trades at 14x LTM P/E. The three% dividend yield is kind of excessive for Japanese requirements.

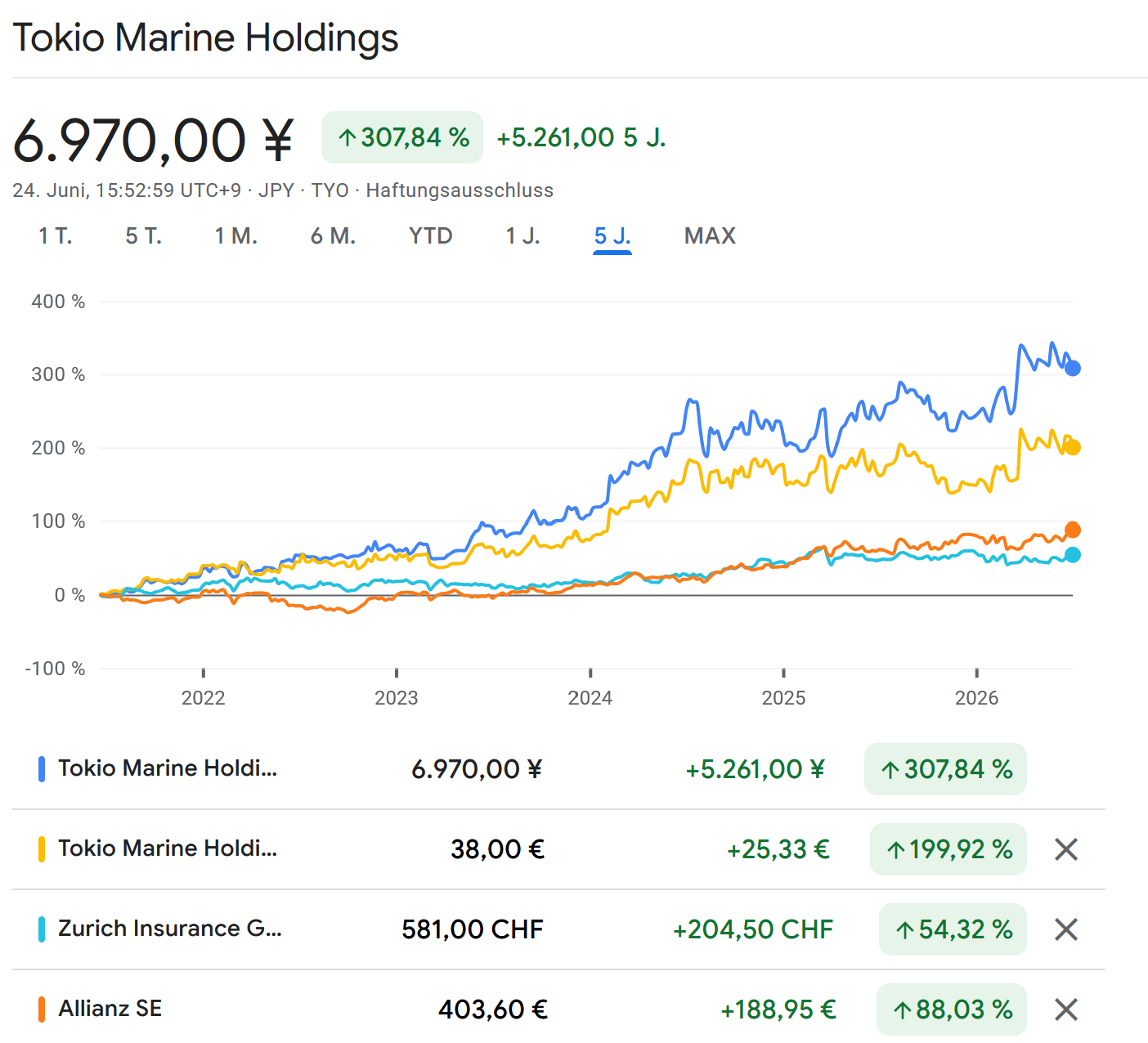

The share value has performed very effectively in Yen. Though as this chart exhibits, a part of the newer efficiency can also be as a result of very weak yen. However the firm nonetheless simply outperformed the European friends Zurich and Allianz by a large margin over the previous 5 years:

One attention-grabbing facet is that Tokio Marine is extensively owned. It was linked to the Mitsubishi Group (Kereitsu in Japanese) however they bought their remaining Mitsubishi shares in 2025.

In addition they said a objective to promote all remaining listed fairness investments by 2029.

The enterprise

Tokio Marine has a surprisingly complete Investor Presentation on its web site.

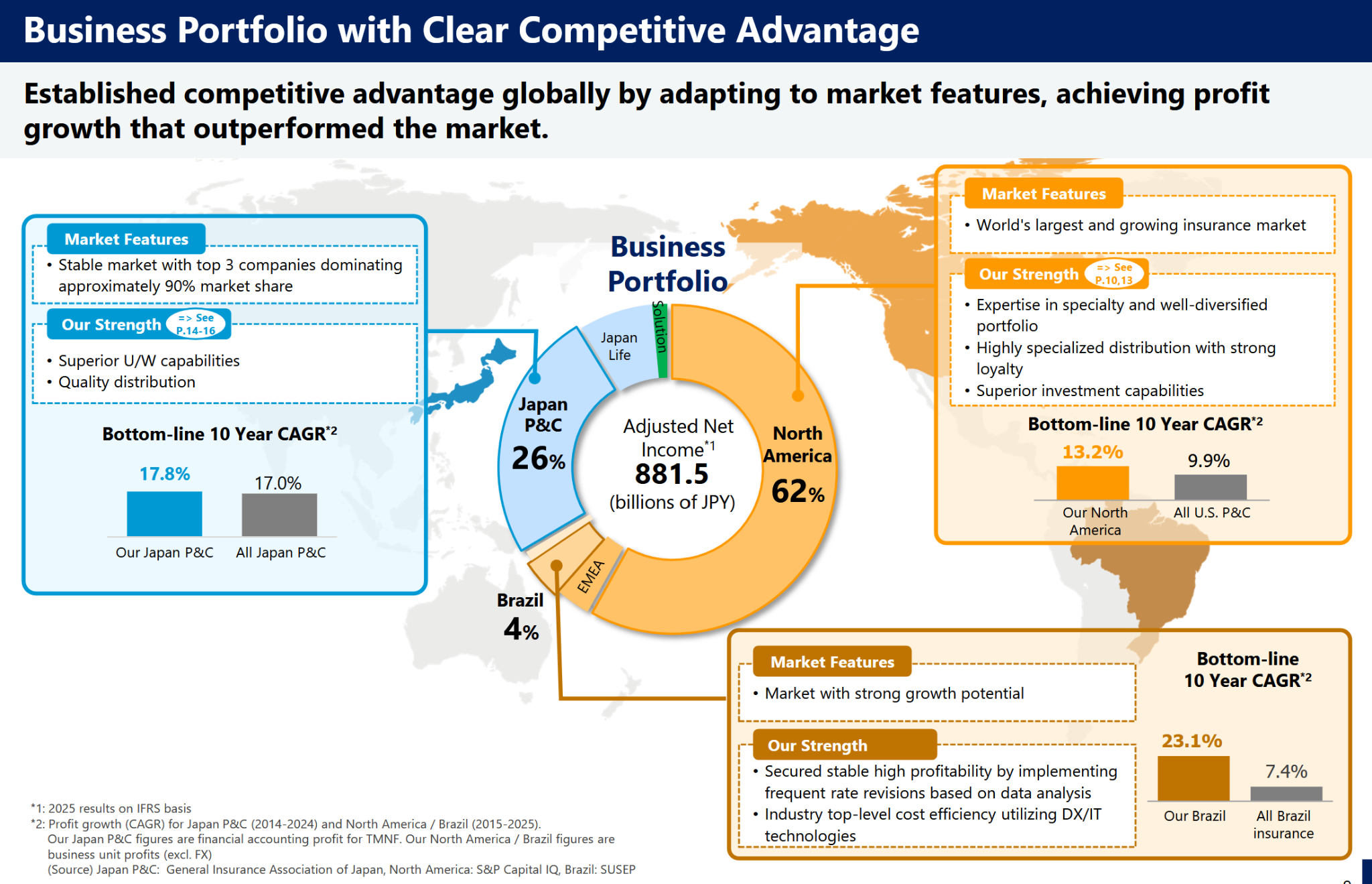

One facet that actually stunned me is that their enterprise appears to be by majority within the US (measured by “adjusted web revenue”) as this chart exhibits:

So primarily, Tokio MArine is a US Specialty Insurer with a Japanese enterprise. Trying on the combined observe report of Japanese acquisitions within the US, this appears fairly good as compared.

Marketing strategy:

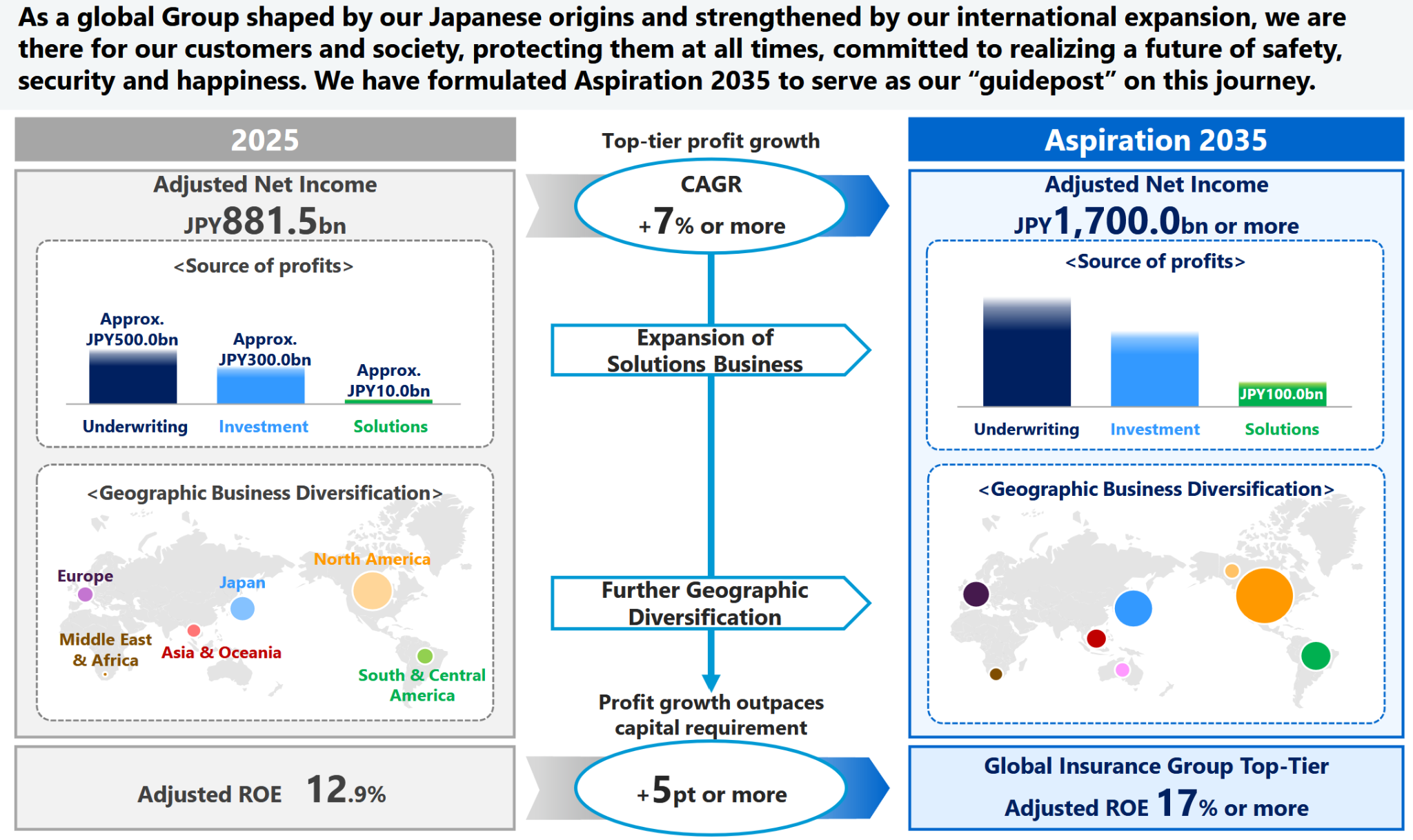

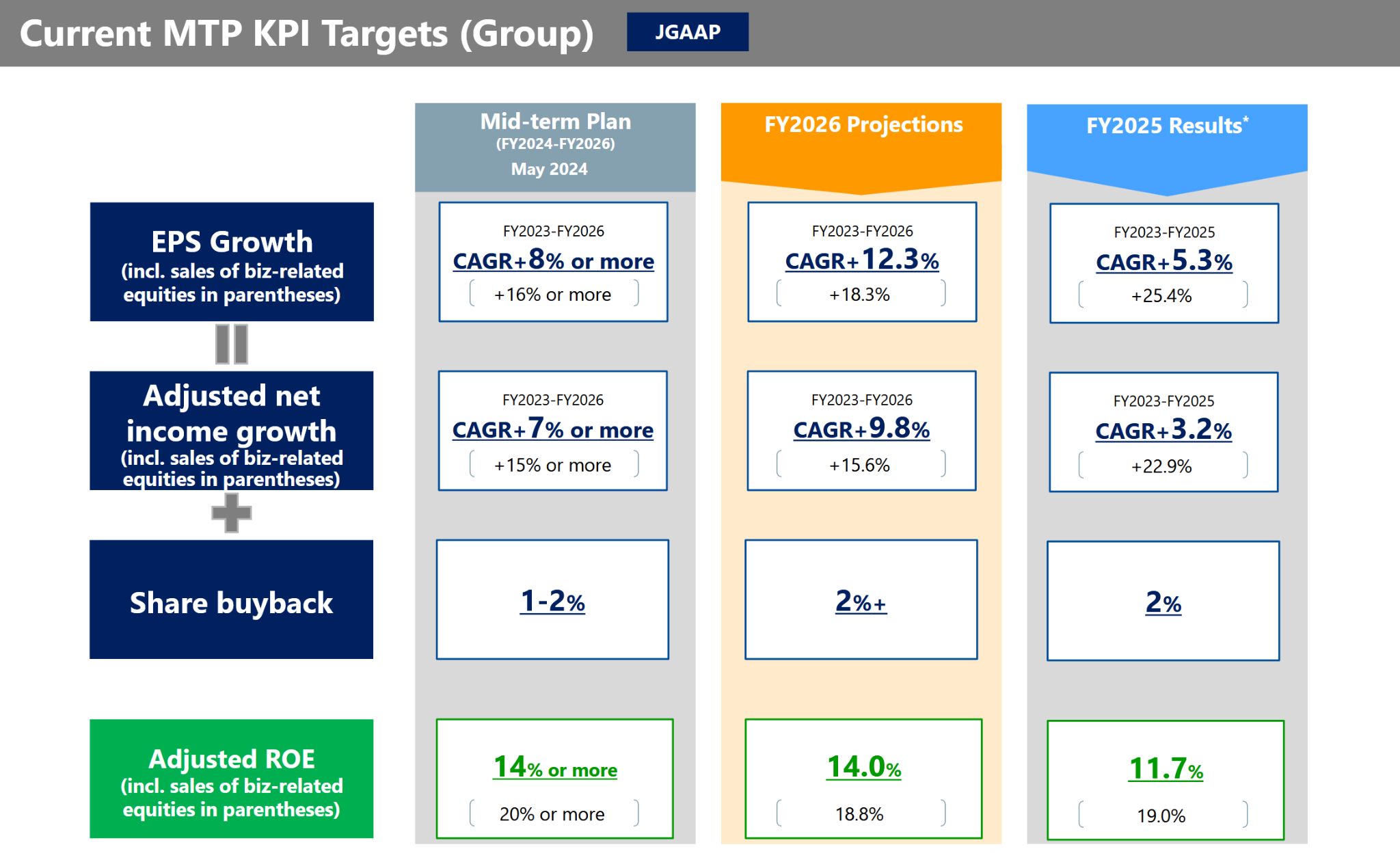

Their plan is to double Web revenue by 2035:

That is some extra element:

After all, as insurance coverage isn’t all the time predictable, this needs to be taken with a grain of salt, however placing out a ten 12 months plan is however a really optimistic facet.

Change from Japanese GAAP to IFRS

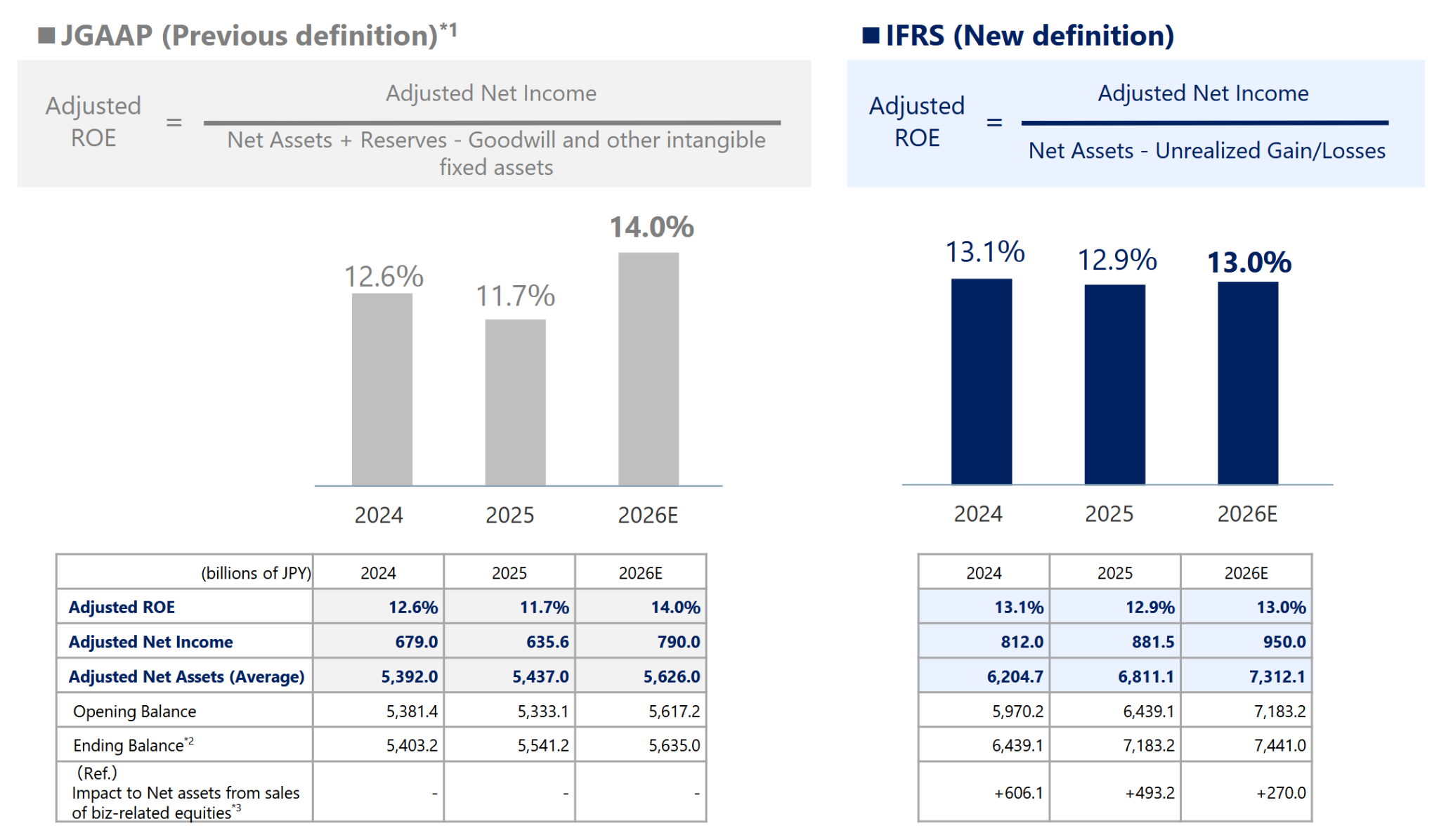

What makes issues somewhat bit extra difficult to research is the very fact, that in keeping with the presentation, Tokio Marine is switching from Japanese GAAP to IFRS in 2026.

They’ve this desk which appears to point that IFRS earnings are increased, however ROE decrease, as web belongings (Fairness) is leaping after the change:

General; Tokio Marine estimates that earnings on an adjusted foundation shall be increased and fewer risky in comparison with JGAAP.

Shopping for an Engineering design firm

One fairly distinctive transaction was their buy of an Engineering design firm in 2025. That’s fairly distinctive amongst insurers.

I’m actually curious if and the way this may really develop within the subsequent 2-3 years.

Capital optimisation

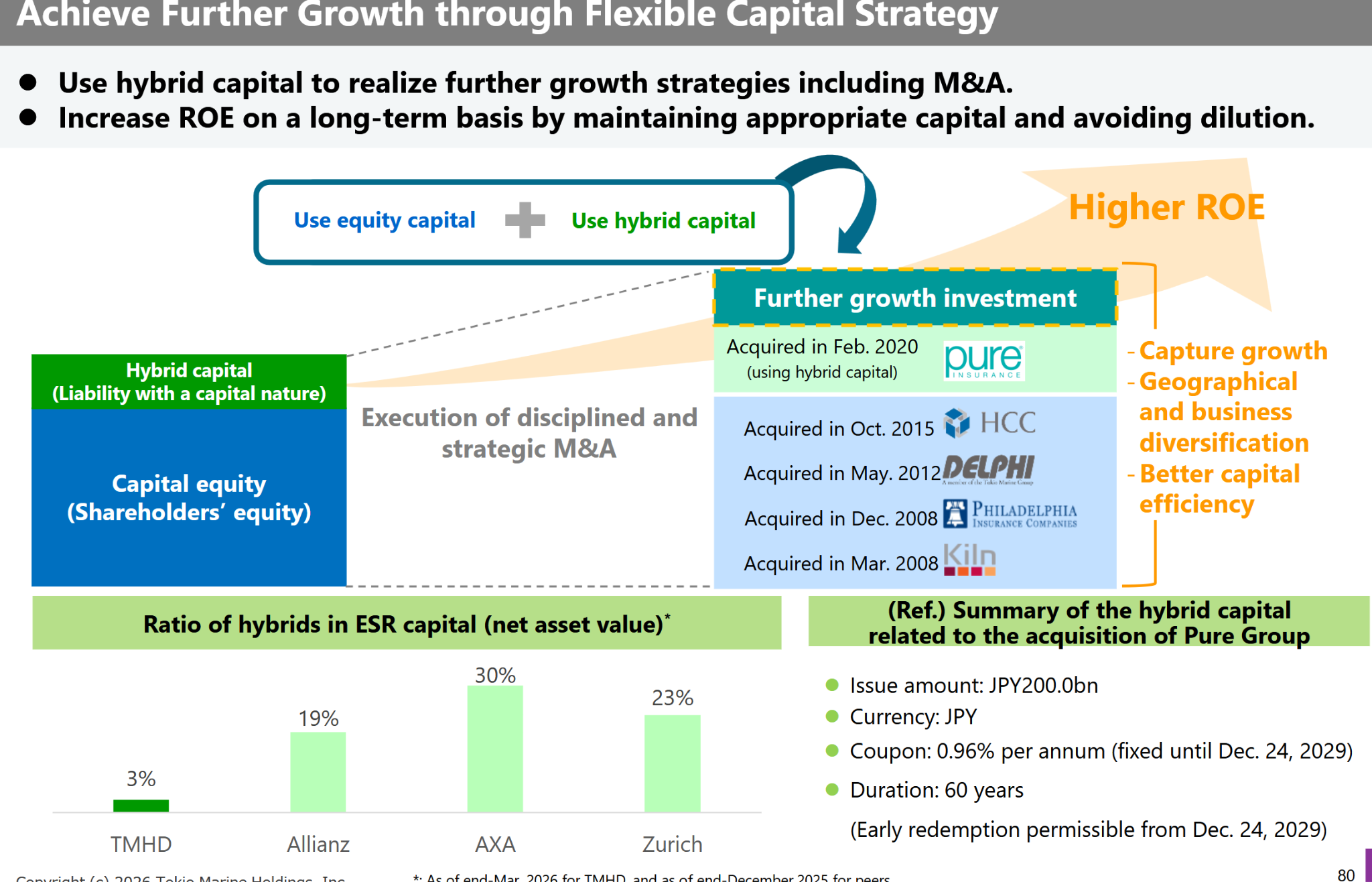

One of many “soiled secrets and techniques” of Insurance coverage shares is {that a} vital a part of the Massive Insurer’s capital base consists of bonds, so referred to as “hybrid bonds”. These are considerably cheaper than fairness. That is Tokio Marine’s slide that exhibits that they’ve made little use of that to this point:

Simply attending to their competitor’s ranges offers them a number of flexibility with regard to M&A and/or share buybacks.

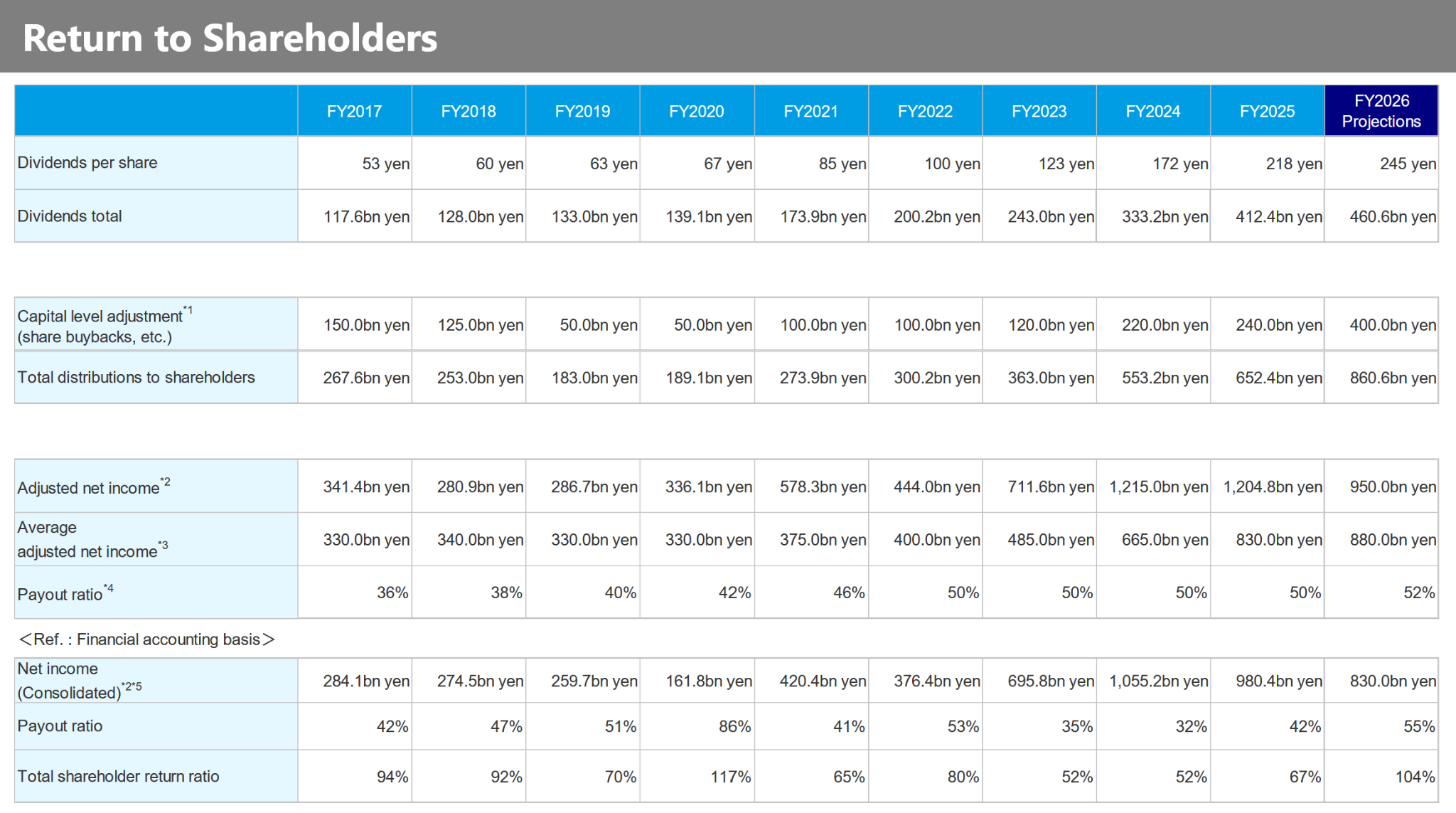

What’s attention-grabbing is clearly additionally how Tokio Marine has elevated dividends and share buybacks over the previous 10 years which might be seen on this desk:

Return expectation:

A simplified return expectation for Tokio MArine would seem like this:

Dividend yield + Buyback yield + development price

Taking Tokio Marine’s numbers this could lead to:

3,1% + 1,5-2% + 7% = 11,6-12,1% p.a. with out assuming any a number of enlargement

This isn’t unhealthy, however to be sincere, additionally not tremendous nice.

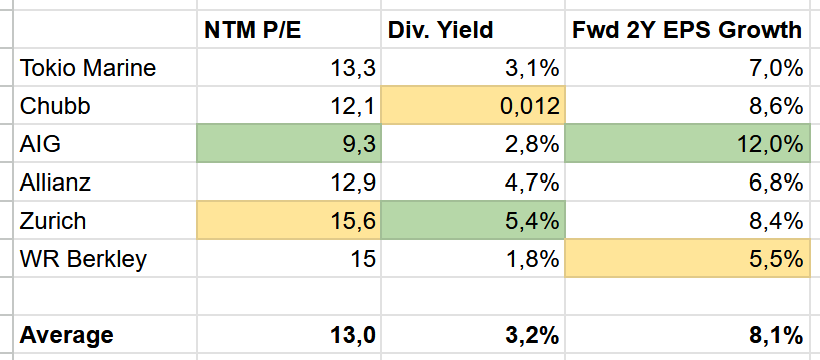

Here’s a fast Peer Group desk which exhibits that Tokio Marine enjoys an absolute common valuation in my subjective Peer Group:

The query or upside can be if Tokio Marine is admittedly an “above common” participant, then perhaps they’d deserve an above common a number of. Based mostly on their very conservative capital construction, they need to (in idea) have the ability to develop greater than rivals.

To be sincere, based mostly on this fast examine, I’m not but prepared to offer them an “above common” score regardless of Ajit’s endorsement.

Professional’s/Con’s

As all the time, a fast abstract of Professional’s and Con’s

- Ajit usually is aware of what he’s doing & Berkshire Cooperation

- Excessive capital flexibility

- Good enterprise combine

- Shareholder pleasant distribution/buyback technique

- Good share value /earnings momentum

- Superb historic development

+/- not tremendous low cost, anticipated return under my hurdle price

+/- Japan GAAP to IFRS transition

+/- complicated enterprise

+/- USD/JPY danger (as EUR investor)

- Common Nat Cat publicity (well-known Japanese Earthquake)

Abstract:

Tokio Marine appears form of attention-grabbing. Particularly the truth that the vast majority of its revenue comes kind the US is a giant shock to me.

Nevertheless, after the Berkshire announcement, the inventory isn’t so low cost anymore.

So in the interim I’ll put it onto my “focus watch checklist” however not make investments. I feel will probably be attention-grabbing to see how IFRS outcomes will seem like in 2026.

In any case, this shift from JGAAP to IFRS appears to be a really attention-grabbing merchandise for Japanese insurers.